{kind=link}

Kajaria Ceramics Ltd. – India’s No.1 Tile Firm

Kajaria Ceramics Restricted (KCL) was integrated in 1985 as a producer of flooring and wall tiles by Mr. Ashok Kajaria in technical collaboration with Todagres SA, Spain. At this time, Kajaria Ceramics is the biggest producer of ceramic/vitrified tiles in India. It has an annual combination capability of 84.45 mn. sq. meters, distributed throughout eight crops – Sikandrabad in Uttar Pradesh, Gailpur & Malootana in Rajasthan, Vijayawada & Srikalahasti in Andhra Pradesh, Balanagar in Telangana and two crops in Gujarat. Kajaria’s manufacturing models are outfitted with innovative fashionable expertise. Intense automation, robotic automobile software and a zero likelihood for human error are few causes for Kajaria to be the #1 within the business. Kajaria Ceramics has elevated its capability from 1 mn. sq. mtrs to 84.45 mn. sq. mtrs. in final 34 years and affords greater than 3000 choices in ceramic wall & flooring tiles, vitrified tiles, designer tiles and rather more.

Merchandise & Companies:

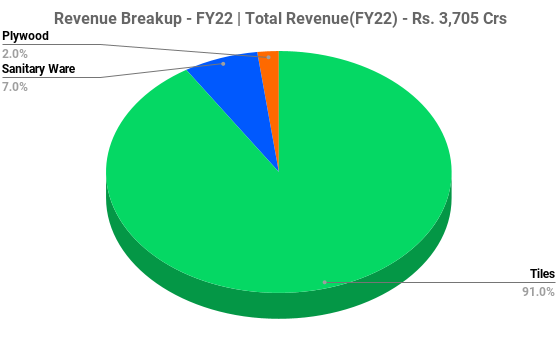

The corporate is producing numerous forms of tiles, sanitaryware and plywood below numerous segments specifically Ceramic Wall & Flooring Tiles, Polished Vitrified Tiles, Glazed Vitrified Tiles, Bathware and Plywood & Laminates.

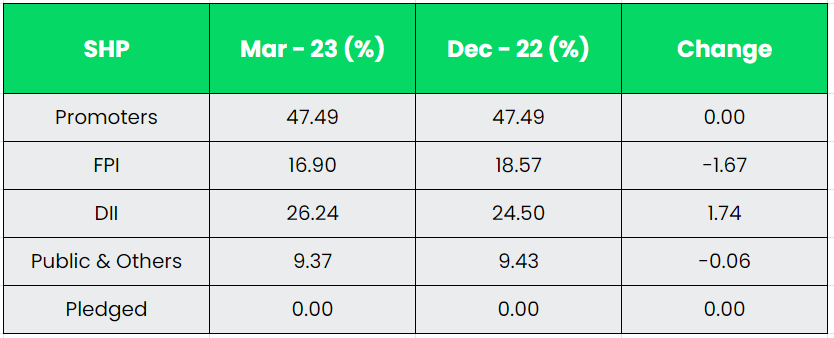

Subsidiaries: As on FY22, the corporate had 5 Subsidiaries and 1 Step down subsidiary.

Key Rationale:

- Largest Participant – Kajaria is the biggest participant within the home tiles business working greater than three a long time. The corporate has a robust model presence with a PAN-India Distribution community of 1825 operative sellers. The corporate had a base of 1700 sellers throughout India at FY22 finish. Later, it added 125 sellers throughout 9MFY23.

- Enlargement – Kajaria introduced an enlargement for big sized glazed vitrified tiles capability of 1.8 MSM/annum on the Sikandrabad plant lately, which is able to enhance the entire capability of the plant from 8.4 MSM/annum to 10.2 MSM/annum on the capex of Rs.70 crs. The enlargement is prone to be accomplished by September, 2023. Moreover, it’s enterprise modernization of its ceramic tile manufacturing capability at Gailpur (Rajasthan) for a capex of ~Rs.51 crs. The modernized capability will produce tiles of bigger measurement (and may have greater realization). Moreover, the corporate is anticipated to take a position Rs.70 crs to arrange a 6 lakh items/annum of sanitary ware manufacturing facility in Gujarat (income potential: ~Rs.150 crs at full capability utilization). The enlargement is anticipated to be accomplished by December, 2023. Additional, the corporate is including new capability of 6 lakh items/annum in its faucet plant at Gailpur, which is able to take the entire the capability to 16 lakh items/annum. Estimated value for this enlargement is ~Rs.5 crs and is anticipated to be accomplished by March, 2023.

- Q3FY23 – The corporate generated an general income of Rs.1091 crs, a rise of two.1% YoY & 1.2% QoQ. Kajaria’s gross sales quantity within the tiles section was muted YoY (down 0.7%) to 25.5 MSM (million Sq. Metres) primarily impacted by a subdued demand state of affairs. Three-year quantity CAGR was at 8%. Tiles income had been up 2.3% YoY at Rs.984 crs. Kajaria’s subsidiaries and allied companies reported muted progress throughout Q3FY23. Within the faucet and sanitary ware section, revenues had been down 2.7% YoY at Rs.79.5 crore. Within the plywood enterprise, revenues had been down 25% YoY and had been at Rs.18.8 crore whereas adhesive enterprise contributed Rs.9 crs to the general income.

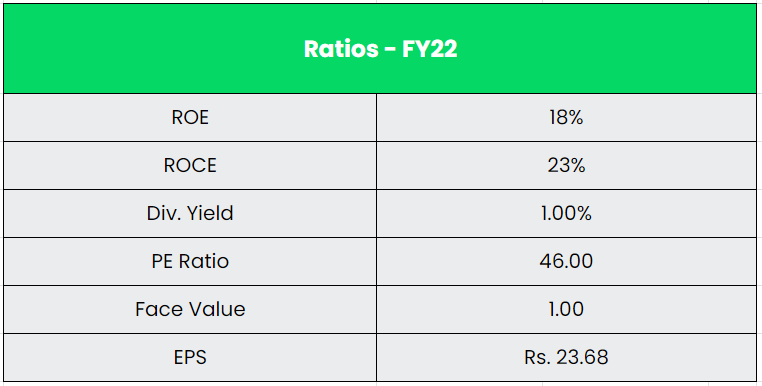

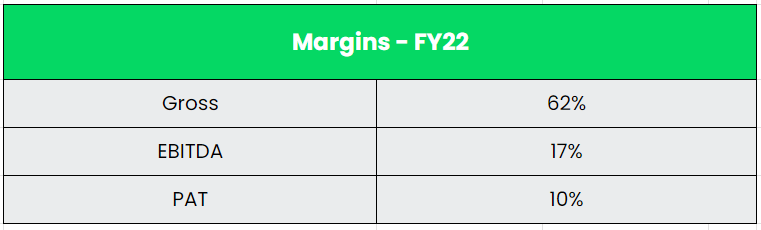

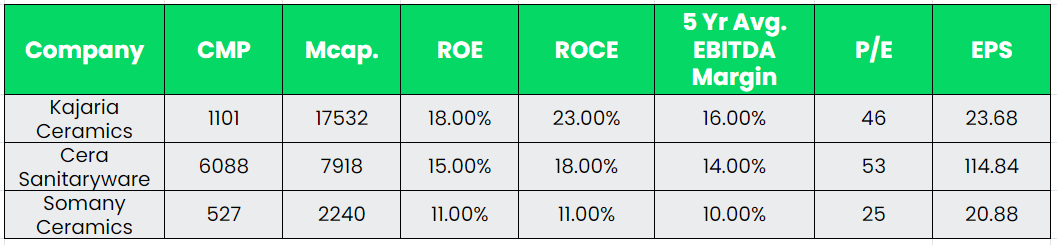

- Monetary Efficiency – Regardless of the corporate’s merchandise catering to actual property business, Common Gross margin has been solidly stood at 64% for FY18-22. The 5-year common Return on Fairness (ROE) and Return on Capital Employed (ROCE) of the corporate is round 16% and 22%, respectively. The steadiness sheet is powerful with money & money equivalents stood at Rs.424 crs (as on FY22) and a really low Debt-to-Fairness ratio of solely 0.08x as on the identical interval.

Business:

The Development business in India consists of the Actual property in addition to the City improvement section. The Actual property section covers residential, workplace, retail, motels and leisure parks, amongst others. Whereas City improvement section broadly consists of sub-segments comparable to Water provide, Sanitation, City transport, Faculties, and Healthcare. The development business market in India works throughout 250 sub-sectors with linkages throughout sectors. The development Business in India is anticipated to succeed in $1.4 Tn by 2025. The Actual Property Business in India is anticipated to succeed in $1 Tn by 2030 and can contribute 13% to India’s GDP. The federal government’s concentrate on constructing infrastructure of the long run has been evident given the slew of initiatives launched lately. The US$ 1.3 trillion nationwide grasp plan for infrastructure, Gati Shakti, has been a forerunner to result in systemic and efficient reforms within the sector, and has already proven a major headway. The Indian tile business measurement is estimated to be ~Rs. 52,700 crs as of FY22. Out of this, home consumption is ~Rs.40,000 crs and exports represent ~ Rs.12,700 crs.

Development Drivers:

- Underneath Funds 2023-24, capital funding outlay for infrastructure is being elevated by 33% to Rs.10 lakh crore (US$ 122 billion), which might be 3.3% of GDP and virtually thrice the outlay in 2019-20.

- City areas are anticipated to grow to be residence to 40% of India’s inhabitants and contribute to 75% of India’s GDP by 2030 with the rise in urbanization.

- The outlay for PM Awas Yojana is being enhanced by 66 % to over 79,000 crs. As of August 2022, 122.69 lakh homes have been sanctioned, 103.01 lakh homes have been grounded, and 62.21 lakh homes have been accomplished, below the Pradhan Mantri Awas Yojna scheme (PMAY-City).

Opponents: Cera sanitaryware, Somany Ceramics, and so forth.

Peer Evaluation:

KCL continues to take care of its margin management place amongst friends within the tiles enterprise. Within the final 5 years, KCL has seen common EBITDA margin of 16% whereas the identical for Somany Ceramics has been at solely 10%. Main causes for KCL’s higher margins are beneficial product combine, greater proportion of in-house produced tiles and technologically superior manufacturing course of.

Outlook:

The corporate has began utilizing Mustard husk, an alternate gasoline with safe provide preparations and can value round Rs.30/SCM (Value could decline if it’s a brand new crop). The Administration in its Q3FY23 con-call said that by February 2023, 65-70% of the gasoline combine can be pure fuel and the remaining can be alternate gasoline. So, if the operations have commenced as per the assertion, there may be large likelihood that the corporate’s common gasoline value will come all the way down to Rs.47-48/SCM in Q4FY23 (vs. Rs.53/SCM in Q3FY23). The Administration additionally guided for a 13-15% YoY enhance in Quantity progress within the tiles section throughout FY24. The components driving the expansion can be wholesome capability utilisation, Rise in Demand from Tier 2 and three cities, anticipated enhance within the manufacturing capability, enhanced seller community and a robust model recall. Aside from Quantity steering, the Administration additionally advised that they anticipate a minimal of 200 bps enchancment within the EBITDA Margin (12% to 14%) throughout Q4FY23 on account of gasoline combine and the relief within the fuel costs. The corporate anticipate capex of Rs.90 crs in FY23 (Rs.75 crs in 9MFY23) and ~Rs.300-350 crs in FY24.

Valuation:

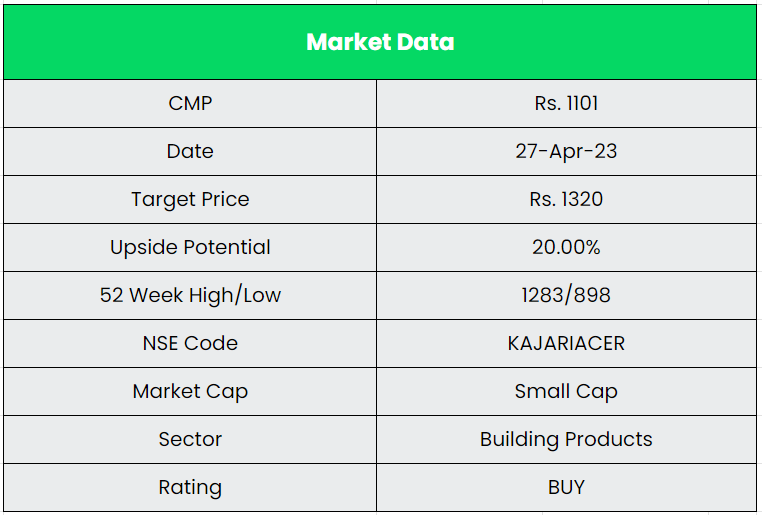

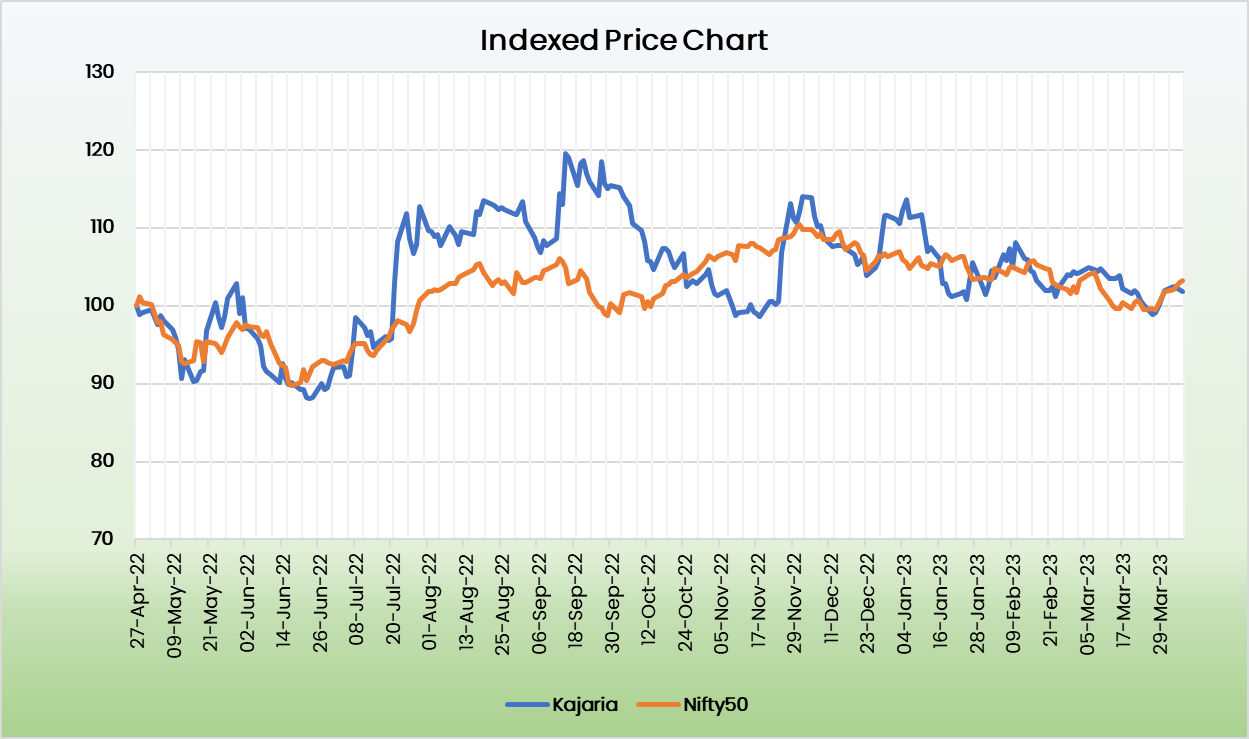

The model ‘Kajaria’ is a robust play within the Tiles section supported by a robust monetary efficiency and steadiness sheet. With the decline within the fuel costs, we consider the margin will begin to get well anytime quickly. We suggest a BUY ranking within the inventory with the goal value (TP) of Rs.1320, 35x FY25E EPS.

Dangers:

- Uncooked Materials Threat – KCL’s profitability stays weak to any enhance within the costs of uncooked supplies and pure fuel as these two elements kind a serious a part of the associated fee construction.

- Economical Threat – Constructing materials business derives its demand from the actual property business. Therefore, any slowdown in the actual property sector will have an effect on KCL. The corporate’s revenues and money flows stay weak to the cyclicality within the end-user business.

- Aggressive Threat – Tile business is extremely aggressive, which restricts gamers’ capacity to move on value inflation. Whereas KCL continues to achieve market share, it actually doesn’t affect costs.

Different articles chances are you’ll like

Publish Views:

849