{kind=link}

Why You Must Plan for Early Retirement Years in Advance

Early retirement is an thrilling prospect to stay up for, however must be deliberate for years earlier than once you would possibly need to retire early. Most of our month-to-month spending past housing, meals and transportation is discretionary. That means, we are able to spend extra or spend much less and nonetheless get by. Listed below are the standard bills you’d must have financial savings put aside for in early retirement:

- Mortgage or rental prices

- Meals at dwelling and eating out

- Transportation and clothes

- Communication companies, together with cellphones and residential web

- Conveniences, like streaming companies and membership memberships

- Larger journey price range whereas retired

- Healthcare bills and insurance coverage premiums

These bills add up. The problem is having funds put aside you could draw from as you have to. Bear in mind, you’ll be able to’t begin pulling cash out of your IRAs and 401(okay)s till you’re no less than Age 59-½. So somebody retiring of their early to mid-50s faces the problem of protecting dwelling bills from financial savings or an funding brokerage account.

Subsequently, understanding the price of medical health insurance is essential. It’s more likely to be considered one of your largest bills in early retirement, one thing you’re not paying for when you’re working and lined by an employer insurance coverage plan.

Excessive Price of Well being Insurance coverage in Early Retirement

Most early retirees are totally answerable for the price of their healthcare bills and insurance coverage. Understanding how a lot this price is crucial to any early retirement plan.

The very best and best method to acquire a quick understanding of the potential price of healthcare in early retirement is to take a look at authorities market plans, also called Obamacare. These are available and essentially the most logical choice for a lot of.

For the sake of this train, we’ll have a look at the full price of a mean healthcare plan utilizing these assumptions:

- State of Illinois

- Married couple in mid-50s

- Most popular Supplier Group (PPO)

- Most cost-effective Silver Plan on Authorities Market

- Assume no Premium Tax Credit that decrease the month-to-month price

Let’s add up all of the direct prices and potential prices to getting healthcare protection on this plan.

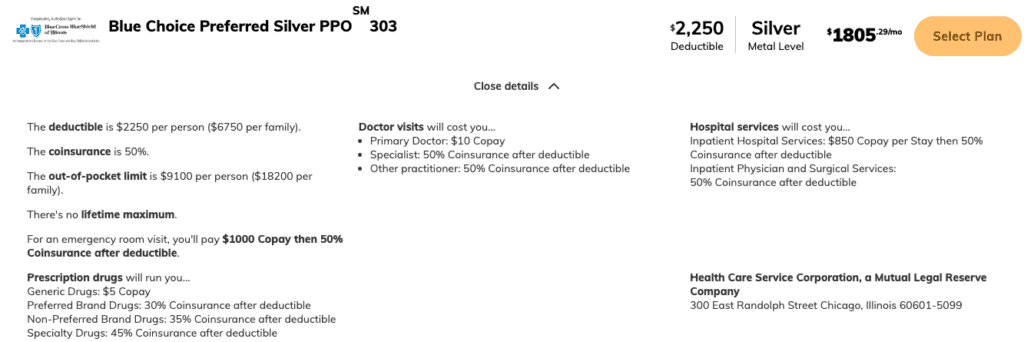

First, you’ve got the month-to-month premiums. For this plan, you’d must pay $1,805/month for an annual whole of $21,660. That price proper there’ll instantly be considered one of your largest month-to-month bills, behind your mortgage cost or lease. Most individuals which have medical health insurance by an employer don’t perceive the total price of that protection; it’s not low cost!

Second, there are insurance coverage deductibles. This plan has a $2,500 deductible per particular person, for a complete of $5,000. That signifies that many of the first healthcare bills you incur every year are your accountability to pay, earlier than insurance coverage actually kicks in.

Third, each plan has an out-of-pocket most that you just’re answerable for. They promote this to individuals as a “good factor” in that there’s a cap on how a lot you need to pay for healthcare every year. However these out-of-pocket maximums might be giant, as within the case right here the place it’s $9,100 per particular person, or $18,200 for the couple.

The worst-case, all-in price of healthcare for a pair that totally makes use of protection beneath this plan is gigantic.

Compound this price for every year in early retirement till you’re eligible for Medicare and it’s an enormous difficulty to think about earlier than you retire!

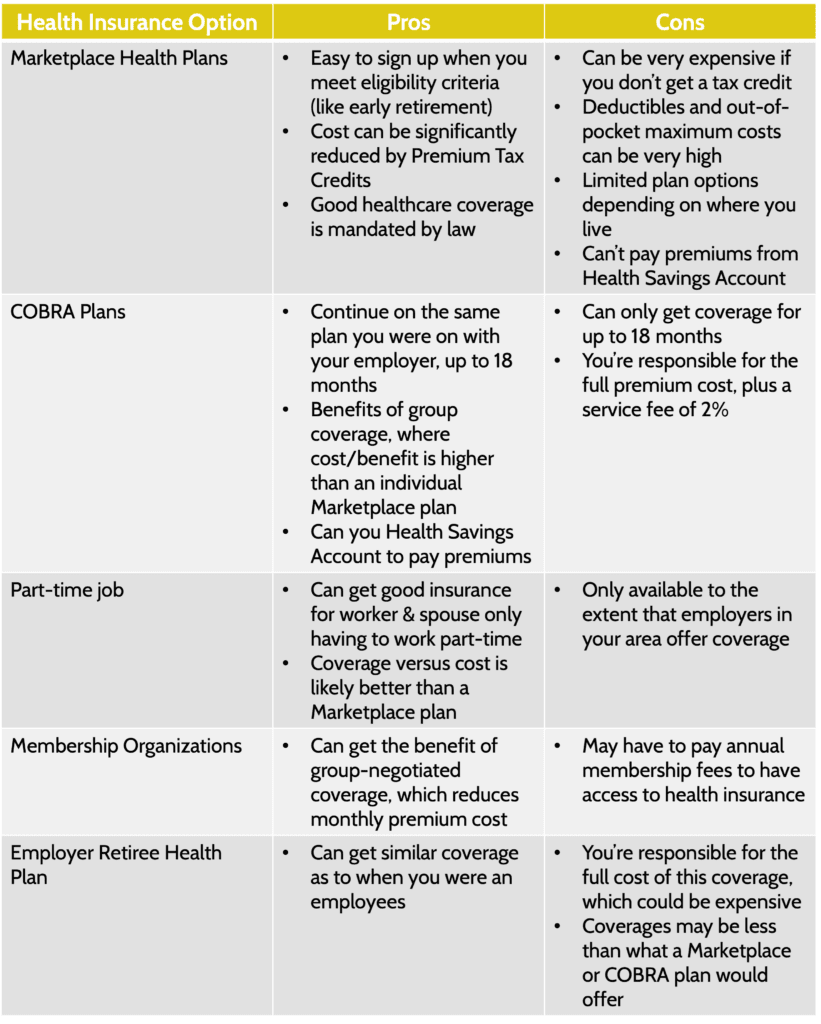

Choice #1: Market Well being Insurance coverage Plan

We’ve simply seen how costly these plans might be. However they’re the best and more than likely manner early retirees can acquire medical health insurance protection.

Nevertheless, there’s a method to considerably cut back the price of these plans: the Premium Tax Credit score. This tax credit score is a subsidy the federal government will present to you to cowl the price of insurance coverage premiums. The dimensions of the subsidy relies in your annual earnings, which for an early retiree, could also be fairly low.

For instance, a pair making $50,000 per 12 months would get a Premium Tax Credit score of $1,300/month, bringing the full month-to-month price from $1,800/month to “simply” $500/month. That provides as much as $15,600 per 12 months of medical health insurance premium financial savings.

The issue with relying on Premium Tax Credit to scale back medical health insurance premiums is that the credit score goes down as your earnings goes up. One of many extra highly effective monetary planning methods for early retirees is making the most of Roth Conversions throughout these low earnings years. The potential tax financial savings from this technique might be huge.

Nevertheless, for those who’re doing a Roth Conversion technique, you create earnings as you exchange Conventional IRA cash to a Roth. Bear in mind, the upper your earnings, the decrease Premium Tax Credit score you get.

Market plans, whereas one of the crucial logical choices, should be chosen and deliberate for with different points of your retirement plan.

Choice #2: COBRA Plans

Corporations with over 20 staff are required by Federal legislation to supply persevering with healthcare protection for 18 months after a employee quits or retires. This legislation known as COBRA.

When most employees hear of COBRA protection, they robotically assume it’s costly. It often is. You’d must cowl the total, month-to-month, price of the insurance coverage your organization gives. This might simply high $2,000/month.

Nevertheless, as a result of your organization is on a bunch insurance coverage plan, they’re often in a position to negotiate a lot better plans for the value paid. Deductibles and out-of-pocket maximums are additionally often decrease.

There may be one HUGE profit to selecting a COBRA plan for those who’ve been saving right into a Well being Financial savings Account (“HSA”). You’re in a position to pay COBRA insurance coverage premiums out of your HSA. The choice to pay medical health insurance premiums out of your HSA is NOT accessible for Market plans. So for those who’re planning for early retirement, stashing some cash into an HSA might be a good way to pay COBRA premiums.

Choice #3: Getting a Half-time Job That Offers Well being Insurance coverage

It might appear odd to say “get a part-time job” when the aim of early retirement is to cease working! However time and time once more, we see purchasers who early retire from a high-stress job however aren’t able to lie round on the seashore but. They nonetheless need to be lively and preserve their thoughts sharp.

Due to the labor shortages we have now in the USA, extra massive corporations are providing greater pay and advantages to part-time employees. For instance, you may get a job at Costco working simply 24 hours every week and get glorious healthcare protection for your self and your loved ones.

Getting a low-stress, part-time job can have many advantages:

- You possibly can have considered one of your largest early retirement bills (healthcare) lined by employer insurance coverage.

- Earned earnings, even modest ranges, reduces the necessity so that you can pull cash out of financial savings to cowl dwelling bills.

- Some individuals simply get pleasure from working in order that they really feel productive.

The important thing right here is doing the analysis on which corporations supply advantages to part-time employees. And this would possibly depend upon which corporations are across the city you reside in.

Choice #4: Group Well being By way of Membership Organizations

In case you’re a licensed skilled in your line of labor, be sure you take a look at medical health insurance choices these skilled organizations would possibly supply. As a result of these organizations can get group protection, the insurance coverage might be cheaper and canopy greater than a typical Market plan.

Choice #5: Employer Retiree Well being Plans

Some employers will supply the choice for a retiring worker to proceed protection beneath a Retiree Well being Plan. The commonest is retiree well being plans that have been negotiated as a part of a union contract. Academics and different authorities employees would doubtless have this selection accessible to them.

The difficulty with retiree well being plans is that they’re generally scaled-down variations of the medical health insurance provided to full-time staff. Within the instances we’ve seen at FDS, it wasn’t a viable choice for early retirees. However these plans are on the market and could be an choice.

Summarizing Your Well being Insurance coverage Choices for Early Retirement

Highly effective Early Retirement Financial savings Plan: Well being Financial savings Accounts

In case you’re pondering of early retirement, be sure you take a look at Well being Financial savings Accounts (“HSAs”) when you’re nonetheless working. Many individuals which have HSAs contribute cash to them every year, however then use those self same funds to pay present medical bills.

HSA could be a highly effective financial savings software, each for retirement and early retirement. You possibly can make investments cash that’s contributed to an HSA for the longer term, very similar to your 401(okay) or IRA. Then, when you’ve got qualifying medical bills, you’ll be able to pull cash out of your HSA tax-free to cowl these prices. Successfully, HSAs are a pool of cash that you just put apart to deal solely with healthcare prices.

How does having an HSA assist in early retirement?

First, you’ll be able to pay premiums for COBRA protection out of your HSA. This can be a distinctive profit that solely applies to COBRA; you can not use HSA financial savings to pay Market or different medical health insurance premiums. Regardless of the (doubtless) excessive price of COBRA protection, for those who’ve completed your work to economize for that into an HSA, you’ve acquired that price lined.

Second, you’ll be able to pay for qualifying medical bills out of your HSA, tax-free. Physician visits and copays, together with many different regular bills qualify. An HSA account turns into a considerable supply to cowl these out-of-pocket bills that will be paid beneath a Market plan, for instance. Given the excessive deductibles and out-of-pocket maximums for a lot of Market plans, having a completely stocked HSA can restrict the quantity you need to take out of day-to-day financial savings to cowl these prices.

HSAs present you quite a lot of tax advantages and suppleness to cowl medical prices in early retirement.

Subsequent Steps for Planning an Early Retirement

When we have now purchasers categorical an curiosity in retiring early, we do quite a lot of work to ensure they’re ready for it. The very last thing somebody needs to do is retire from the rat race, solely to must get a job once more as a result of the price of early retirement was greater than they anticipated.

We mannequin a variety of healthcare situations for our purchasers, assessing the tradeoff between doing Roth Conversions and getting a Premium Tax Credit score on a Market plan, for instance. And if the shopper is a number of years away from retiring, we have a look at accessible HSA choices at their employer to assist construct a “warchest” of devoted healthcare funds for early retirement.

Medical insurance is only one vital consideration for early retirement.