{kind=link}

This submit is a part of a collection sponsored by CoreLogic.

Insurers affected by Hurricane Ian’s damaging path throughout Florida on the finish of September 2022 confronted operational, regulatory and statutory necessities for correct projections of the last word monetary value of the harm. Accustomed to utilizing disaster danger fashions to venture their final losses, the uncertainty bounds on their loss estimates have been significantly greater for this occasion. Whereas hurricane loss fashions are able to estimating damages and insured losses to buildings and belongings to some recognized diploma of certainty, there are different sources of loss that are much less sure.

These uncertainty components are known as post-loss amplification components. These embody a requirement surge issue, i.e., a short-term run-up in costs pushed by the extraordinary prices of importing outdoors employees and supplies, and cost-inflation components arising from regulatory points just like the task of advantages regulation (AOB) in Florida. These post-loss amplification components have plagued the Florida insurance coverage market for a few years and have been step by step getting worse, culminating in a seemingly endless upward spiral of claims prices for Hurricane Irma in 2019.

Latest ranges of traditionally excessive inflation fueled by provide shortages of supplies and excessive vitality prices have contributed to vital will increase in the price of on a regular basis items and providers, with shopper worth inflation peaking at just below 10% earlier this 12 months. Labor shortages additionally proceed to be a difficulty, with the Nationwide Federation of Unbiased Companies reporting hiring to be as exhausting as ever.[1]

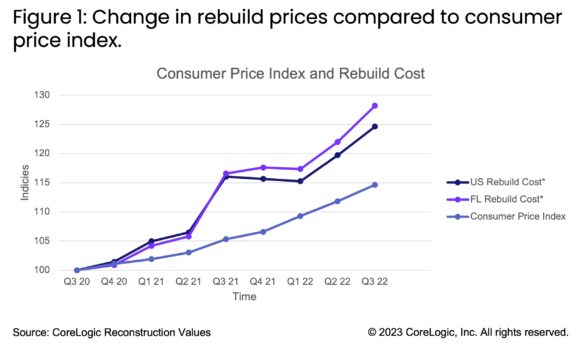

The prices of building supplies and labor used for rebuilding have been rising quicker than basic inflation, with ranges just below 15% in the beginning of 2022. We will see within the graph beneath that these prices have seen an excellent steeper rise in Florida.

Determine 1: Change in rebuild costs in comparison with shopper worth index.[2]

CoreLogic loss estimates have been calculated utilizing the newest values for rebuild prices. The issue is that insurers or brokers could also be schedules or values from twelve months or extra in the past which may very well be undervalued with little or no future inflation constructed into the schedule. Prices to insurers are incurred as soon as the restore is full. As of November 22, 2022, virtually 50% of the insurance coverage claims have been nonetheless open and 25% have been nonetheless open as of January 20, 2023.[3] The most expensive claims take the longest time to restore with inflation driving final prices greater. This lag is even longer for reinsurers.

In 2017, Florida had a major change to the constructing code for current buildings which required a complete roof part to get replaced the place 25% or extra of a roofing part is broken and the place there have been errors with the allowing, set up, or inspection.

Task of advantages is a longtime apply in Florida that allows a property proprietor the flexibility to rent a contractor to restore their property and to assign the advantages of their insurance coverage coverage to the contractor in lieu of a direct cost. Devised to ship agility and velocity to owners in search of repairs to their property, the addition of lawyer settlement charges to the declare have elevated prices to insurers for settlements and, finally, has elevated prices to owners.[4] In Could of 2022, Florida’s legislature applied reforms to the AOB legal guidelines and the effectiveness of those reforms is untested.

The revised 2017 laws on AOBs similar to lowered claims home windows, worth of cancellation, and contingent charges could have a major affect on reducing prices provided that insurers can cease doubtful actors from contacting their shoppers and proactively beginning to deal with settled claims early. Additional reforms enacted by emergency legislative session have now (going ahead at the very least) banned the flexibility of policyholders to assign the advantages of their coverage to threerd events and restricted the flexibility to get well authorized charges. Nonetheless, the laws is just not retroactive, so claims from Hurricane Ian may nonetheless be topic to AOB-inflated losses.

Hurricane Ian and Housing: By the Numbers

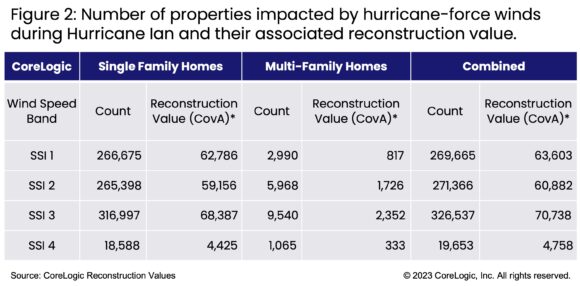

CoreLogic estimates that just about 900,000 houses have been topic to hurricane drive winds, and 600,000 of these have been topic to extreme Cat 2 or Cat 3 wind speeds. Per the Florida Workplace of Insurance coverage Regulation, roughly 475,000 residential claims have been on file as of January twentieth, 2023, up from 440,000 claims on file as in November 2022.

The continued stabilization of those declare numbers could also be proof of the enhancements made to home-strengthening constructing code laws within the years since Hurricane Andrew (1991). This high-volume of claims can be a take a look at of not solely the adequacy of the latest AOB reforms in decreasing general restore/insurance coverage prices for owners to restore/insure their houses but additionally a take a look at for insurers and reinsurers in managing the uncertainty of figuring out the last word value of Hurricane Ian.

To study extra concerning the impacts of Hurricane Ian 6 months after landfall, see a latest CoreLogic webinar exploring the findings of a harm survey in Southwest Florida together with an in depth breakdown of the modeled losses and what made this hurricane occasion so distinctive.

©2023 CoreLogic, Inc. The CoreLogic® statements and knowledge on this article will not be reproduced or utilized in any kind with out categorical written permission. Whereas all of the CoreLogic statements and knowledge are believed to be correct, CoreLogic makes no illustration or guarantee as to the completeness or accuracy of the statements and knowledge and assumes no duty in any way for the knowledge and statements or any reliance thereon.

[1] https://www.nfib.com/content material/press-release/economic system/nfib-jobs-report-nearly-half-of-small-business-owners-still-cant-fill-job-openings/

[2] U.S. Bureau of Labor Statistics, Client Value Index

[3] https://www.floir.com/house/ian

[4] https://floir.com/shoppers/assignment-of-benefits-resources

Subjects

Revenue Loss

Taken with Revenue Loss?

Get automated alerts for this subject.