{kind=link}

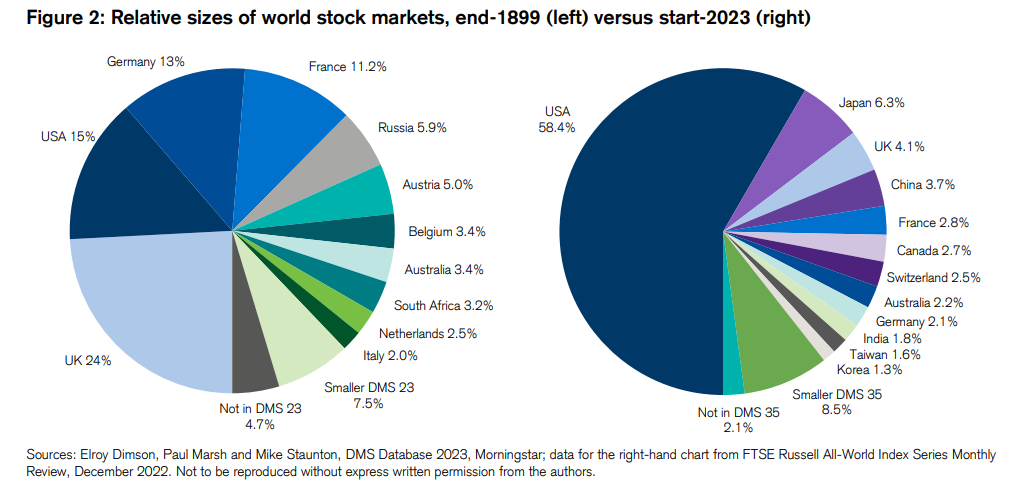

The USA makes up almost 60% of the worldwide inventory market by market capitalization:

The dominance of American shares over the remainder of the world wasn’t only a Twentieth-century phenomenon both.

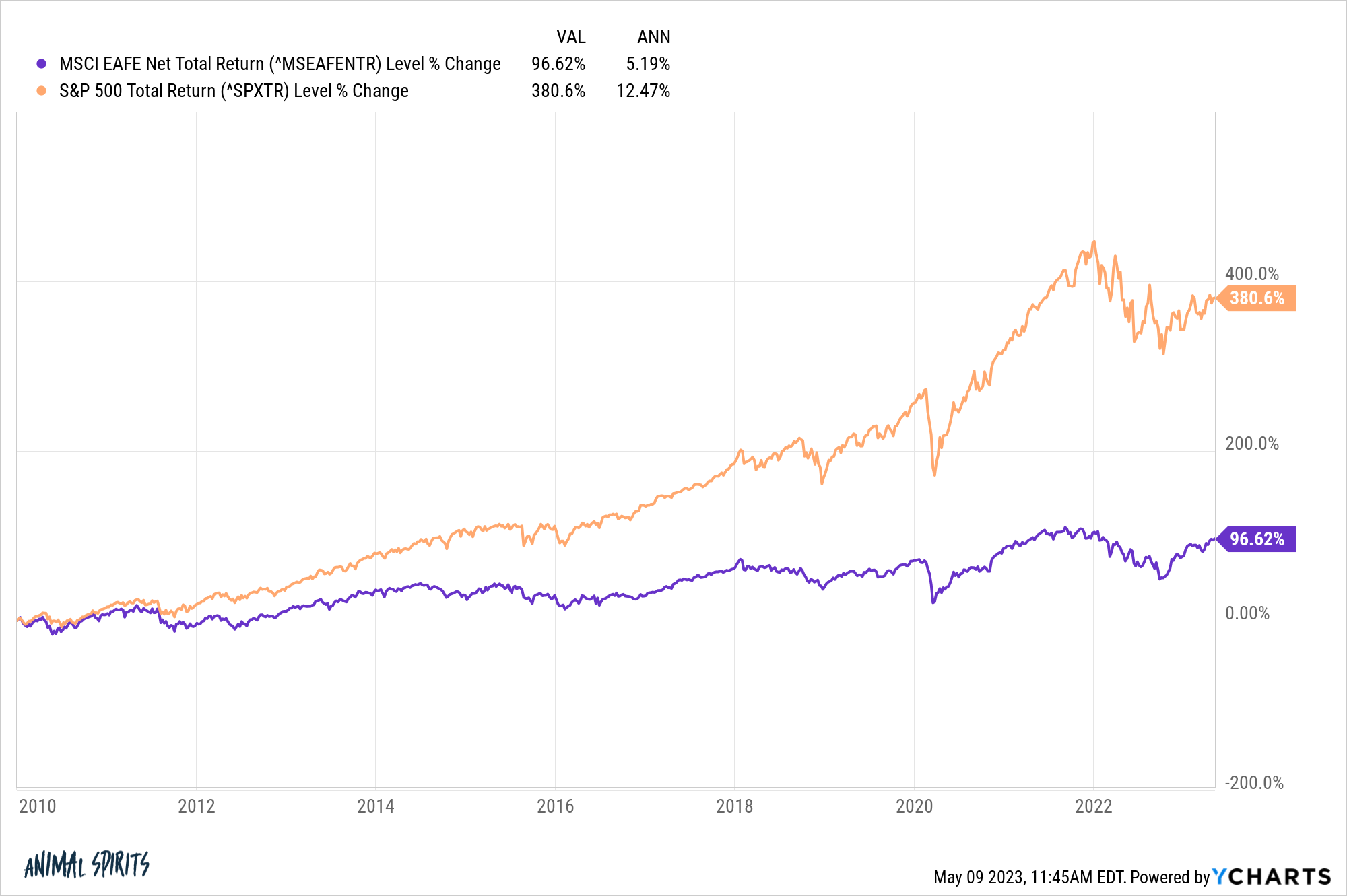

The efficiency over the previous decade and alter reveals U.S. shares profitable fingers down over our international counterparts:

Many traders have a look at these numbers and surprise: What’s the purpose of proudly owning worldwide shares if the U.S. is clearly the one recreation on the town?

I perceive the sentiment. The USA has the vast majority of the largest and finest corporations on the earth. A lot of these companies are multi-national and get an honest share of their income from abroad.

Having mentioned that, it’s nonetheless worthwhile to think about worldwide diversification over the long-run.

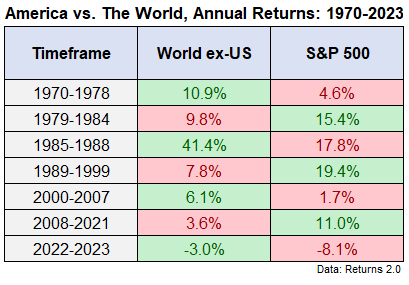

We now have MSCI knowledge for worldwide shares going again to 1970. Listed here are the annual returns for the S&P 500 and MSCI World ex-U.S. by means of April 2023:

- U.S. shares +10.5%

- Worldwide shares +9.1%

That’s a win for the stars-and-stripes however not a blowout by any means.

The win share isn’t that a lot better both. Over the previous 53 years from 1970-2022, worldwide shares had larger returns than U.S. shares 25 occasions. The U.S. inventory market had higher efficiency in 28 out of 53 years.

It looks as if U.S. shares at all times outperform however that’s recency bias at work. The efficiency is cyclical identical to every thing else within the markets.

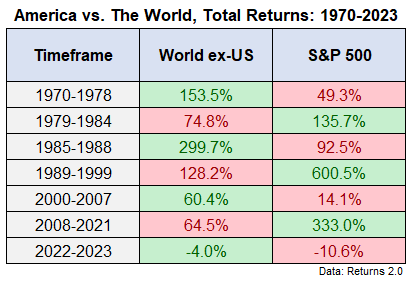

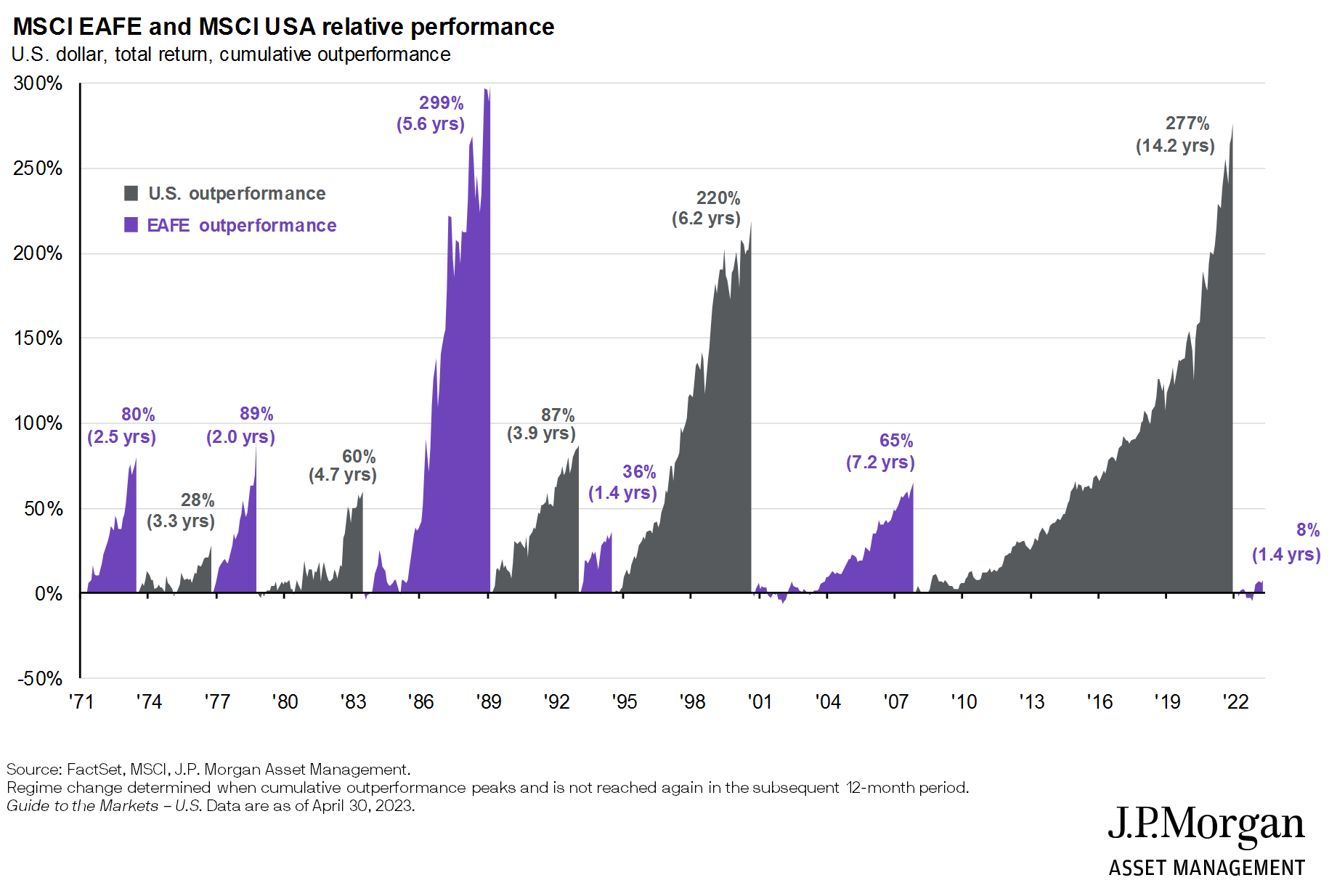

Listed here are whole returns by varied durations of over- or underperformance for every going again to 1970:

Some traders have a neater time wrapping their heads round annualized returns so listed here are these figures as effectively:

U.S. inventory had an unbelievable run popping out of the Nice Monetary Disaster however worldwide shares did much better at occasions within the Seventies, Nineteen Eighties and early-2000s.

It’s additionally true that a lot of the outperformance has taken place through the newest cycle. From 1970-2012, the annual returns had been mainly useless even:

- U.S. shares +9.7%

- Worldwide shares +9.6%

All the outperformance has primarily come since 2013.

One factor that jumps out is the magnitude and size of outperformance by U.S. shares since 1990 or so.

This JP Morgan chart does a pleasant job of visualizing the size of relative efficiency over time:

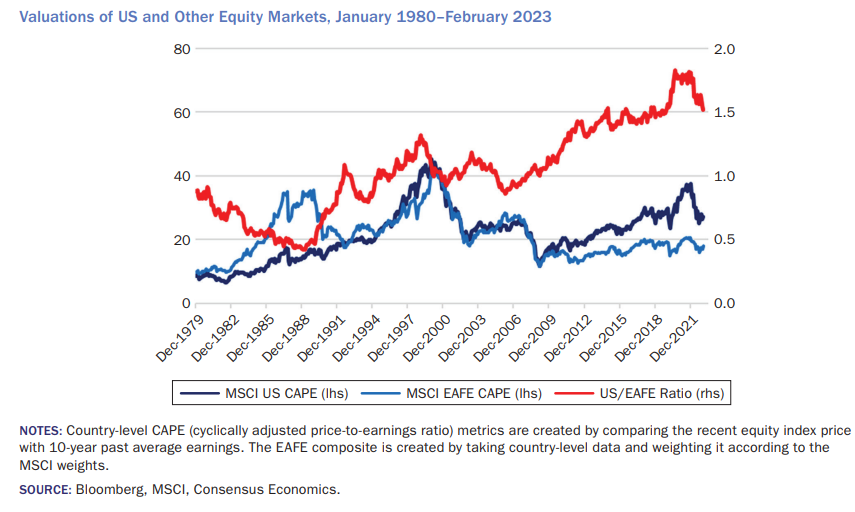

AQR simply put out a brand new analysis piece that appears on the reasoning behind the relative power of U.S. shares over the previous 30+ years:

Since 1990, the overwhelming majority of the US’s outperformance versus the MSCI EAFE Index (forex hedged) of a whopping +4.6% per 12 months, was because of modifications in valuations. The wrongdoer: In 1990, US fairness valuations (utilizing Shiller CAPE14) had been about half that of EAFE; on the finish of 2022, they had been 1.5 occasions EAFE. When you management for this tripling of relative valuations, the 4.6% return benefit falls to a statistically insignificant 1.2%.

Right here is the visible illustration of those phrases:

Principally, worldwide shares went from comparatively costly (hi there Japan) to comparatively low cost and U.S. shares went from comparatively low cost to comparatively costly.

May this proceed? Possibly.

Would I wager my life (or portfolio) on it? In all probability not.

I like AQR’s conclusion on whether or not or not worldwide diversification remains to be price it regardless of the underperformance in latest many years:

Worldwide diversification remains to be price it, even when it hasn’t delivered for US-based traders in 30 years. A lot of the US fairness outperformance throughout this era displays richening relative valuations, hardly a cause for elevating and even retaining US overweights at the moment. If something, traditionally large relative valuations level the opposite manner. At this time is an unusually unhealthy time to take the mistaken classes from the previous. Sadly, not often has doing the correct factor been so arduous (and it’s by no means simple).

Diversification is tough since you simply know there may be at all times going to be one thing in your portfolio that’s going to underperform. You simply don’t know what that asset class or technique it will likely be at any given time.

That’s a characteristic, not a bug of spreading your bets on the subject of portfolio administration.

It’s definitely potential your portfolio could be superb over the long-haul investing solely in U.S. shares from present ranges.

But it surely’s additionally extremely possible U.S. shares will underperform worldwide shares, presumably for an prolonged time period.

Should you may predict the long run there could be no cause to diversify however nobody has the flexibility to know what comes subsequent within the markets or world financial system.

All investing entails trade-offs.

Diversification is about giving up on the flexibility to hit a grand slam so that you don’t strike out on the plate.

World diversification is about accepting adequate returns to keep away from the potential for horrible returns at an inopportune time.

Additional Studying:

Diversification Isn’t Undefeated But it surely By no means Will get Blown Out