Magenta Therapeutics (MGTA) ($39MM market cap) is a member of my damaged biotech basket, I am bringing it ahead once more to focus on the chance for shareholders to vote down the proposed reverse merger with privately held Dianthus Therapeutics. In MGTA’s S-4, the corporate strongly hints that if the deal isn’t authorized, a dissolution and liquidation is on the desk:

If the merger isn’t consummated, Magenta’s board of administrators might resolve to pursue a dissolution and liquidation. In such an occasion, the amount of money out there for distribution to its stockholders will rely closely on the timing of such liquidation in addition to the amount of money that may must be reserved for commitments and contingent liabilities.

There may be no assurance that the merger can be accomplished. If the merger isn’t accomplished, Magenta’s board of administrators might resolve to pursue a dissolution and liquidation. In such an occasion, the amount of money out there for distribution to its stockholders will rely closely on the timing of such choice and, with the passage of time the amount of money out there for distribution can be lowered as Magenta continues to fund its operations. As well as, if Magenta’s board of administrators have been to approve and suggest, and its stockholders have been to approve, a dissolution and liquidation, Magenta can be required underneath Delaware company legislation to pay its excellent obligations, in addition to to make affordable provision for contingent and unknown obligations, prior to creating any distributions in liquidation to its stockholders. On account of this requirement, a portion of its belongings might must be reserved pending the decision of such obligations and the timing of any such decision is unsure. As well as, Magenta could also be topic to litigation or different claims associated to a dissolution and liquidation. If a dissolution and liquidation have been pursued, Magenta’s board of administrators, in session with its advisors, would want to judge these issues and make a dedication a couple of affordable quantity to order. Accordingly, holders of its widespread inventory may lose all or a good portion of their funding within the occasion of liquidation, dissolution or winding up.

Included within the S-4 can also be a administration ready liquidation evaluation (the distribution estimate right here assumes a Could or June 2023 distribution, clearly that is not a sensible timeline, further liquidation prices can be incurred if MGTA does find yourself down that street):

In mild of the foregoing components and the uncertainties inherent in estimated money balances, stockholders are cautioned to not place undue reliance, if any, on the Liquidation Evaluation.

The beneath abstract of the Liquidation Evaluation is topic to the statements above, and it represents Magenta administration’s estimates of Magenta’s money which can be distributed to stockholders as permitted underneath relevant legislation pursuant to a plan of dissolution.

Key assumptions underlying the Liquidation Evaluation included (i) that all the distribution of Magenta’s web money can be made in both Could 2023 or June 2023, (ii) that Magenta would have roughly $65.2 million and $63.9 million of web money as of Could 2023 and June 2023, respectively, after deducting prices and bills, together with authorized charges, the charges payable to Magenta’s strategic monetary advisor, accounting charges, worker retention bonuses, severance and advantages, insurance coverage bills and different transaction-related prices, with no changes for taxes; (iii) that these prices and bills have been forecasted to whole roughly $11.8 million assuming the closing of a liquidation in every of Could 2023 and June 2023; and (iv) roughly 60.7 million whole shares excellent as of April 27, 2023. The evaluation resulted in an estimated money distribution per share in Could 2023 and June 2023 of $1.07 per share and $1.05 per share, respectively.

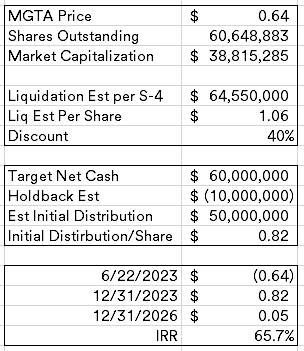

At this time, shares commerce for $0.64 per share, effectively beneath administration’s liquidation estimate. There is a affordable presumption a liquidation would certainly observe a “no” vote to the merger, per the merger settlement, MGTA can be required to pay a termination charge of $13.3MM (large compared to their money balances or market cap) if MGTA enters into one other merger inside 12 months.

Termination Charges Payable by Magenta

Magenta should pay Dianthus a termination charge of $13.3 million if (i) the Merger Settlement is terminated by Magenta or Dianthus pursuant to clause (e) above or by Dianthus pursuant to clause (f) above, (ii) at any time after the date of the Merger Settlement and previous to the Magenta particular assembly, an Acquisition Proposal with respect to Magenta could have been publicly introduced, disclosed or in any other case communicated to the Magenta board of administrators (and won’t have been withdrawn), and (iii) within the occasion the Merger Settlement is terminated pursuant to clause (e) above, inside 12 months after the date of such termination, Magenta enters right into a definitive settlement with respect to a subsequent transaction or consummates a subsequent transaction.

A liquidation can be their solely practical possibility, 12 months is a very long time to attend it out for a money burning biotech with no pipeline (they offered all their belongings in April). In an effort to shut the deal, MGTA wants a majority of the votes forged to vote in favor of the merger (edit: they want a majority of the shares excellent), the help settlement solely has 6.9% of the shares, leaving fairly a little bit of floor to cowl. Tang Capital Administration owns just below 10% and presumably is the Investor named within the background part of the S-4 who proposed a money tender provide:

Between March 1, 2023 and March 28, 2023, a stockholder of Magenta (the “Investor”) made a number of unsolicited inquiries to Stephen Mahoney, the President, Chief Monetary and Working Workplace of Magenta, to inquire whether or not Magenta would have an curiosity within the Investor proposing a money tender provide for Magenta at a reduction to its present money place. No particular proposal, phrases or valuation have been mentioned throughout this dialog, or any subsequent dialog between the Investor and representatives of Magenta.

It’s unlikely that Tang would vote in favor of the reverse merger at this level, given the present low cost to money. I am guessing it will likely be difficult for administration to get the 50% of the vote essential, however as we have seen in different microcaps, getting buyers to vote in any respect could possibly be a difficulty. A non-vote right here would not affect the vote a technique or one other, possible benefitting administration.

MGTA’s goal web money place on the time of closing (Q3) per the merger settlement is $60MM, if we assume that the vote fails and MGTA pursues a liquidation, let’s guess that they holdback $10MM for added winddown bills or contingencies.

Above is my potential IRR math, I am assuming an preliminary distribution by yr finish after which a small one ($3MM of the $10MM holdback) in 3 years. As well as, the corporate did promote their pre-merger belongings in April, $20MM in mixed milestone funds are in play too, however I am assuming these are nugatory. The merger vote hasn’t been set but, however I’d anticipate it in early-mid Q3. I purchased extra lately.

Disclosure: I personal shares of MGTA