{kind=link}

A comparatively minor bureaucratic change proposed by the Federal Housing Finance Company stirred up a viral storm in right-leaning information media not too long ago, with retailers just like the Washington Occasions, New York Put up, Nationwide Overview and Fox Information all reporting some variant of the sentiment expressed within the Occasions headline: “Biden to hike funds for good-credit homebuyers to subsidize high-risk mortgages.”

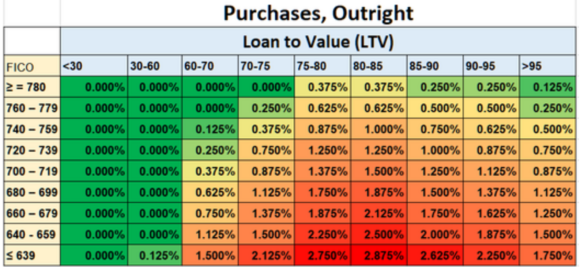

The underlying challenge issues the FHFA’s current determination—as conservator of the government-sponsored enterprises (GSEs)—to revise the loan-level worth changes (LLPAs) charged by Fannie Mae and Freddie Mac, which collectively account for roughly 60% of U.S. residential mortgage loans. The LLPAs that the GSEs cost are decided primarily by mortgage kind, loan-to-value ratio and a borrower’s credit score rating.

What’s broadly true within the protection is that the adjustments—which have been first introduced in January, have an effect on loans delivered to the GSEs on or after Might 1 and due to this fact have already been applied by lenders for months—do on steadiness have a tendency to cut back prices for these with decrease credit score scores and improve prices for these with larger credit score scores. In reality, as a part of a broader repricing change introduced final 12 months, the FHFA eradicated charges altogether for typical loans for about 20% of dwelling patrons, financed by elevated upfront charges for second houses, high-balance loans, and cash-out refinancings.

Sadly, the way in which this story has been spun within the wake of the adjustments would depart many information shoppers with the impression that debtors with larger credit score scores can be paying extra outright in charges than debtors with decrease credit score scores. That is definitely not the case. Evaluating apples to apples, at each stage of the grid, a borrower with a better credit score rating would proceed to have decrease LLPAs (or, in lots of LTV classes, none).

Writing in his Substack e-newsletter Kevin Erdmann of the Mercatus Heart responded to a Fox Information graphic that declared, below the brand new guidelines, a “620 FICO rating will get a 1.75% charge low cost” whereas a “740 FICO rating pays a 1% charge”:

I’m fairly certain what they’ve executed right here is cherry decide the low credit score rating that had the most important charge lower. Then, they reported the overall charge of a better credit score rating. So, a low down cost 620 rating has a charge that went from about 6.75% to five% (when mortgage insurance coverage is included). And, additionally, the charge for a 740 rating went from 0.25% to 1%. (plus a 0.25% mortgage insurance coverage charge). Why didn’t they simply say that charges for 740 scores went up 0.75%? It could nonetheless get their partisan level throughout. It could nonetheless be bizarre, as a result of it will be describing mortgages with two completely different down funds. And it will cover the truth that the 620 rating nonetheless has a charge that’s greater than 3% larger than the 740 rating. However, at the very least it wouldn’t be mixing ranges with adjustments.

Finally, whether or not these explicit adjustments are good or dangerous for the GSEs is an actuarial query. As Erdmann goes on to notice, there are good causes to imagine that the charges on lower-credit debtors have been too excessive for an prolonged interval.

However there are different causes to be involved about what the incident may imply for insurance coverage markets. Right here, the concern is that state regulators—or, within the worst-case situation, Congress—may suppose charging these with excessive credit score scores extra to subsidize these with low credit score scores may really be an thought worthy of emulation.

Clearly, insurers’ use of credit score data in underwriting and rate-setting has been a topic of public debate for occurring 4 many years. At this level, whereas a handful of states prohibit the follow outright, most have adopted laws that allows it, with some caveats.

The FHFA precedent—permitted as a result of Fannie and Freddie have been within the company’s conservatorship for shut to fifteen years—is especially regarding given current instances of state insurance coverage regulators transferring to restrict or ban using credit score data with none specific course from state legislators to take action. Whether or not courts select to uphold such unilateral choices will depend on the particularities of state legislation.

Final 12 months, Washington State Insurance coverage Commissioner Mike Kreidler moved to undertake a everlasting rule enacting a three-year ban on using credit-based insurance coverage scores, after a predecessor emergency rule to do the identical was declared invalid in September 2021 by Thurston County Superior Courtroom Choose Indu Thomas. An August 2022 remaining order from Thomas discovered that Kreidler exceeded his authority in adopting the rule when there was a particular state statute that allowed insurers to make use of credit score scoring.

Extra not too long ago, the Nevada Supreme Courtroom dominated in February to uphold a short lived ban on the use credit score data in insurance coverage rate-setting initially issued by the Nevada Division of Insurance coverage in December 2020. The rule, which is scheduled to run out Might 20, 2024, was unsuccessfully challenged by the Nationwide Affiliation of Mutual Insurance coverage Firms.

The rise of credit-based insurance coverage scoring has revolutionized the trade, permitting vastly larger segmentation and higher matching of danger to charge. The place state residual auto insurance coverage entities as soon as insured as a lot as half or extra of all private-passenger auto dangers, they now signify lower than 1% of the market nationwide. It could be unlucky if some deceptive headlines impressed ill-considered regulation to reverse that progress.

Crucial insurance coverage information,in your inbox each enterprise day.

Get the insurance coverage trade’s trusted e-newsletter