{kind=link}

Should you’re paying off a mortgage (say a house or automobile mortgage) and out of the blue end up with some additional money, you is perhaps questioning whether or not to place it in the direction of paying off the mortgage or investing.

It’s a difficult selection, however we’ve bought some insights that will help you make the best determination.

There are principally two lenses that you need to use to unravel the dilemma:

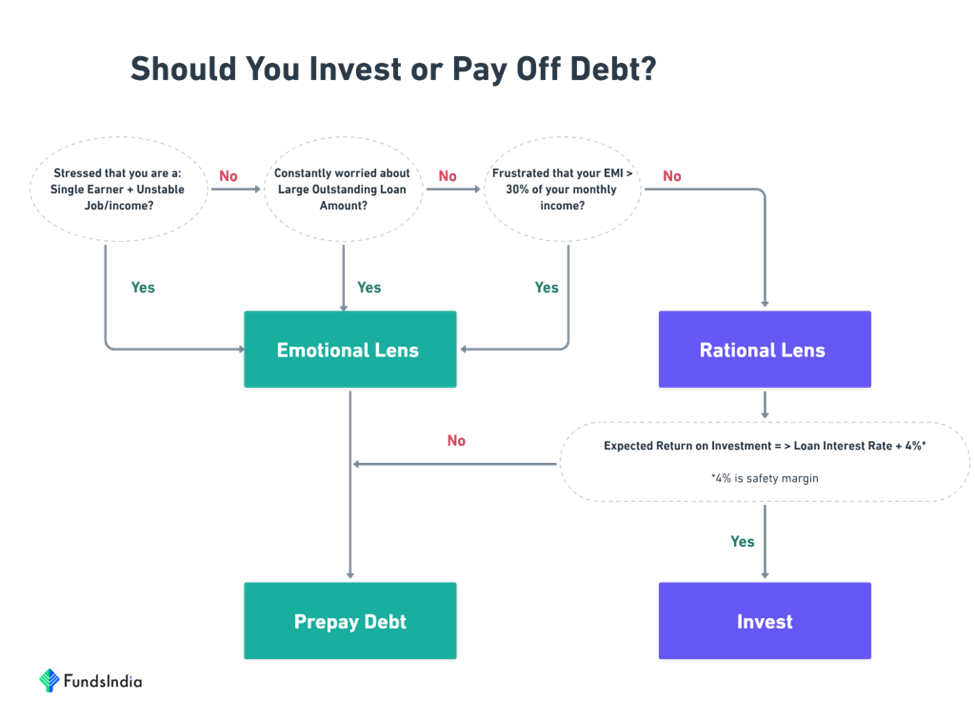

LENS 1: RATIONAL LENS

The logical place to begin is to check the anticipated future return out of your funding vs your present mortgage’s rate of interest.

If,

Anticipated Return from Funding >= Mortgage Curiosity Price + Security Margin (4%) = Make investments

Anticipated Return from Funding < Mortgage Curiosity Price + Security Margin (4%) = Prepay Debt

Why do now we have a security margin?

- Buffer for rising rates of interest – In the previous couple of months the mortgage rates of interest have elevated from 6% to nearly 8-9%. To offer for such rising charges a further buffer is required.

- Buffer for surprising Funding returns – There will be instances when the Funding returns don’t end up as anticipated, for such decrease than anticipated return outcomes a buffer is required.

Right here is an instance of how this works.

Assume you intend to put money into Fairness Mutual Funds and your return expectation is round 12%.

Your present dwelling mortgage fee is at 9%.

So,

Anticipated Return from Funding at 12% < 13% (i.e. Mortgage Curiosity Price of 9% + Security Margin of 4%)

This implies from a rational standpoint, it’s higher to ‘Prepay Debt’

LENS 2: EMOTIONAL LENS

Positive, the rational perspective makes logical sense. However let’s be actual, in relation to making selections, feelings can play an enormous function too. In actual fact, typically our feelings are simply as vital because the rational aspect of issues, if no more.

So, allow us to additionally put on the emotional lens and verify how you are feeling concerning the excellent mortgage and month-to-month EMIs?

Query 1: Are you confused that you’re a single earner and have an unstable job/earnings?

- If sure, it’s higher to prepay debt.

Query 2: Do you continuously fear about your massive excellent mortgage quantity?

- If sure, it’s higher to prepay debt which helps cut back the stress and burden.

Query 3: Are you pissed off that your month-to-month EMIs take away a big half (>30%) of your month-to-month earnings?

- If sure, it’s higher to prepay debt.

So, how do we all know when to use which lens?

The choice flowchart under will assist perceive when to make use of which lens.

Summing it up

- There are two lenses to guage this dilemma of prepaying debt vs investing.

- The Rational lens is the place you evaluate the anticipated funding returns and the mortgage rate of interest. The Emotional lens is the place you make selections based mostly on how you are feeling.

- Whereas each lenses are equally vital, you need to use the above framework to prioritize.

Different articles you might like

Submit Views:

4,846