{kind=link}

In response to the Federal Reserve Board’s April 2023 Senior Mortgage Officer Opinion Survey (SLOOS)—carried out for financial institution lending exercise over the primary quarter of 2023—banks reported that lending requirements tightened for many residential actual property (RRE) and industrial actual property (CRE) mortgage classes. Demand for RRE and CRE loans weakened throughout all classes over the quarter. No banks anticipated their lending requirements for many loans to ease over the rest of 2023 and one-third anticipated extra tightening.

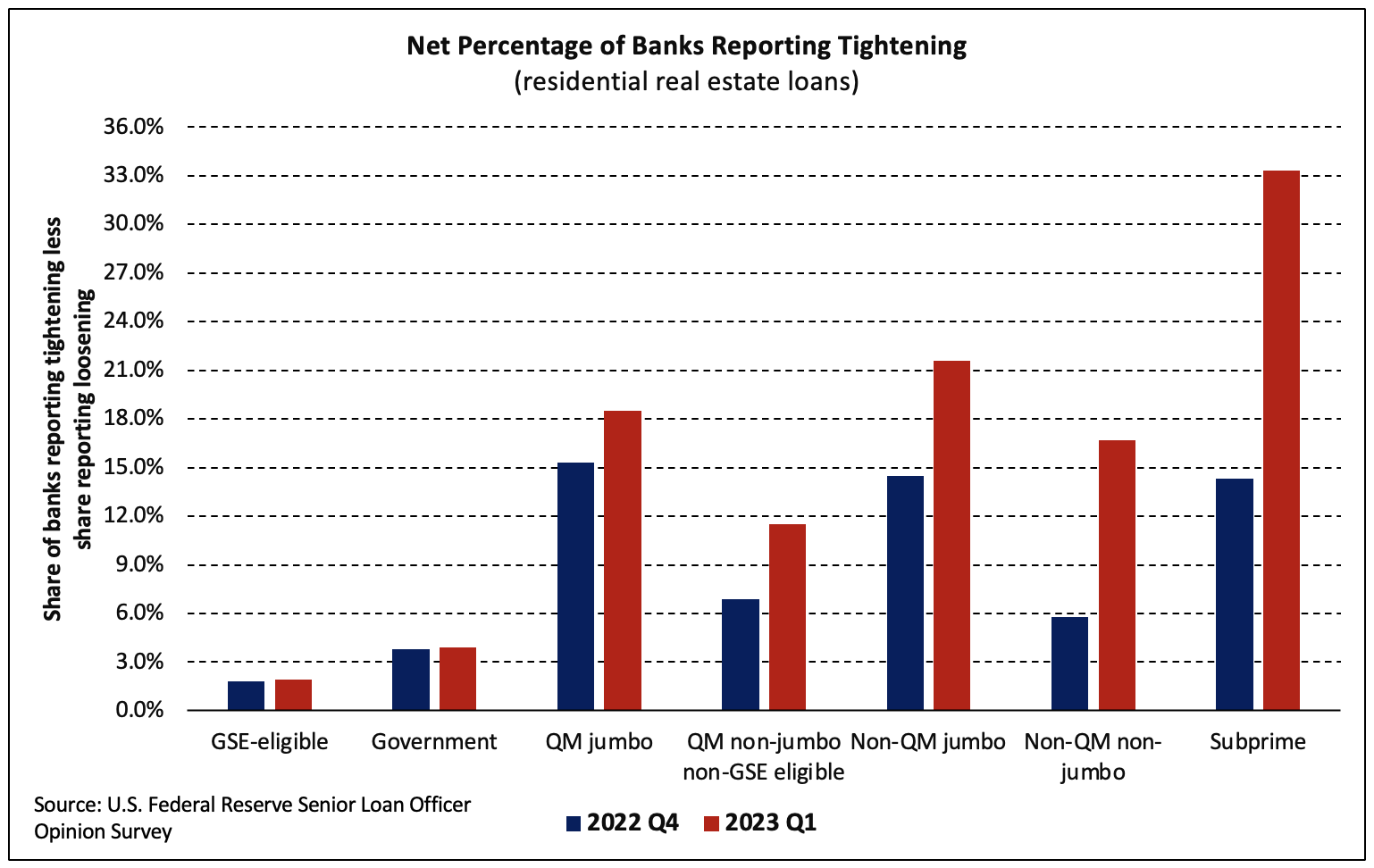

Residential mortgage lending requirements tightened essentially the most for subprime loans as the web share of banks reporting tighter requirements for these loans climbed from 14.3% to 33.3%. Banks additionally reported substantial tightening for non-QM non-jumbo, non-QM jumbo, QM jumbo, and QM non-jumbo non-GSE eligible RRE loans. In distinction, GSE-eligible (+0.1 ppt) and authorities (+0.1 ppt) loans every noticed a small enhance within the web % of banks reporting tighter requirements in Q1 2023 than This autumn 2022.

Demand weakened for all RRE mortgage classes and residential fairness traces of credit score (HELOCs). The web share of banks reporting weaker demand averaged 50.8% throughout mortgage classes. Whereas excessive, it was a big enchancment from the 87.4% common in This autumn 2022.

Banks tightened requirements for all sorts of business actual property loans, on web, although tightening was extra extensively reported by mid-sized banks than the biggest corporations. Banks additionally reported weaker demand for development and land improvement loans, loans secured by multifamily properties, and loans secured by nonfarm nonresidential properties.

Banks reported having tightened all of the phrases surveyed on all classes of CRE loans over the previous yr. For multifamily and development and land improvement loans, a considerable web share of banks widened the unfold on mortgage charges, lowered the loan-to-value ratio, elevated debt service protection, and decreased most mortgage measurement.

Associated