{kind=link}

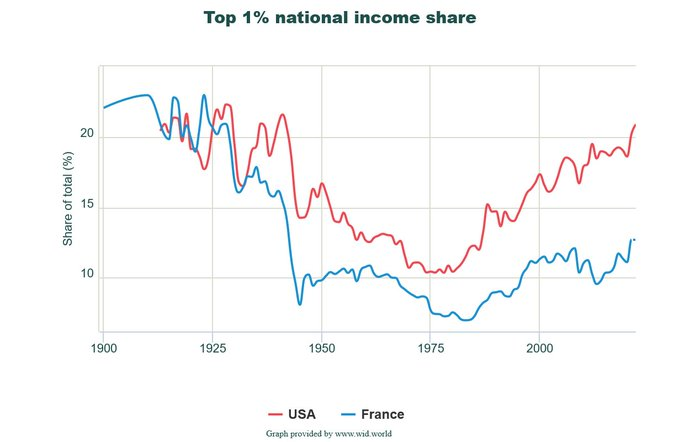

Thomas Piketty is well-known for his work on estimating revenue and wealth inequality. That work made him an “economics rockstar” within the eyes of the media, as he appeared to substantiate a preferred narrative about rising inequality. Piketty’s stats confirmed a constant pattern throughout the Twentieth-century United States. High revenue and wealth concentrations adopted a U-curve sample, the place the early 1900s had been marked by excessive “Gilded Age” ranges of inequality. These ranges fell quickly in the course of the Nineteen Forties, stayed low till the Nineteen Eighties, and quickly rebounded till the current day because the “high 1 %” pulled away from the remainder of the pack.

In reality, Piketty claims that US inequality right this moment is increased than it was in 1929 — the very best level on the primary half of the U-curve. The principle offender behind rising inequality, in line with his story, is a collection of tax cuts starting with the Reagan administration. Simply the identical, Piketty factors to the mid-Twentieth century’s tax system, the place high marginal charges peaked at over 90 %, as the explanation for the trough in his U-curve. The ensuing collection of educational articles — usually co-authored with Gabriel Zucman and Emmanuel Saez — are deemed as novel and necessary contributions to the scholarly literature on inequality.

The empirical work of Piketty and his coauthors has attained immense affect in American political life. The media usually touts the U-curve and its depictions of skyrocketing inequality because the Nineteen Eighties as a stylized truth. Politicians and pundits invoke his tutorial works to justify tax hikes and redistributive applications, all within the identify of combating inequality.

What if Piketty and his crew received the numbers mistaken although? What if inequality wasn’t rising as quick as he claimed, or what if the results of rising revenue concentrations had been already offset by current authorities applications? There would now not be an empirical case for mountaineering taxes or increasing authorities redistribution. That’s the implication of a bevy of latest analysis articles, displaying that Piketty’s statistics might (and may) be discarded in favor of extra rigorous work.

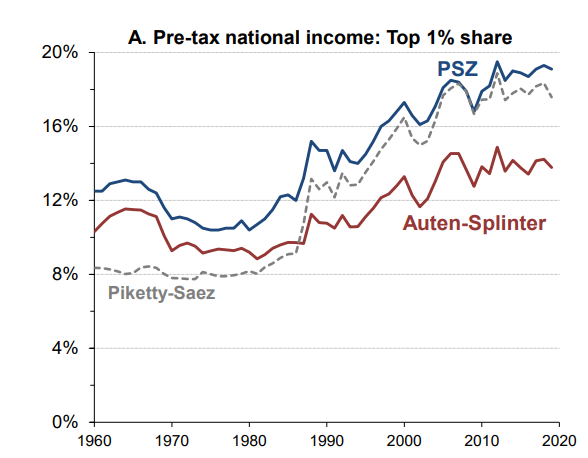

The latest of those is an article by David Splinter and Gerald Auten within the Journal of Political Financial system. Auten and Splinter revisited most of the knowledge building assumptions made by Piketty and his acolytes in coping with knowledge from 1960 to 2020. Most notably, they made certain that revenue definitions had been constant over time, that the right households had been thought of (as Piketty et al. used tax items that may be simply biased by demographic adjustments), and that higher knowledge had been used. They ended up discovering that Piketty’s mid-century trough was not as little as marketed. Additionally they confirmed that the rise in revenue concentrations after 1980 was way more average than Piketty claims.

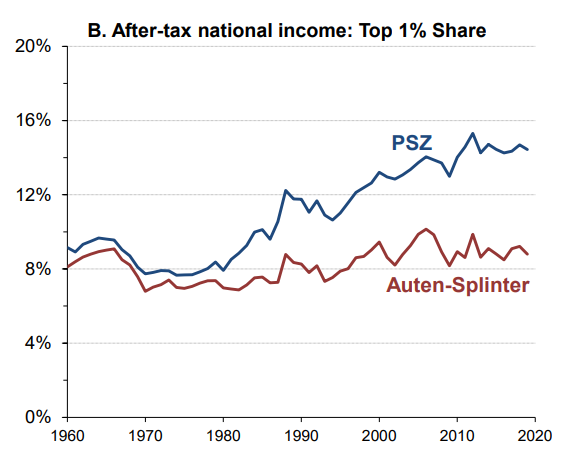

In the principle article by Piketty and Saez, the highest 1 % earned 9 % of all pre-tax incomes in 1980 versus 20 % in 2020. In Auten and Splinter’s enhancements, these proportions are 9 % and 14 %, respectively. After accounting for transfers and taxes (one thing that Piketty and Saez fail to do), Auten and Splinter discover just about no adjustments since 1960. Piketty and his defenders have so far attributed the variations to differing assumptions about methodology and the calculation of imputed parts of their collection. However Auten and Splinter’s work exhibits that these assumptions matter an important deal, that means Piketty’s model is now not an authoritative customary for evaluating ranges of inequality.

However what if we put aside the methodological disagreements about imputed knowledge and focus as an alternative on merely getting the underlying statistics proper? It seems that Piketty and Saez’s authentic collection had a number of accounting errors, knowledge discrepancies, and even historic errors in how they handled adjustments to the tax code.

In a latest working paper, we put aside the discretionary disagreements over imputation and solely regarded on the ways in which Piketty and his coauthors dealt with the underlying tax statistics. At a number of factors over their century-long collection, they change out their approaches for estimating the whole quantity of revenue earned in america every year. This determine permits them to calculate the share of these earnings that went to the richest 1 %, utilizing revenue tax information.

Oddly sufficient, Piketty’s most sweeping methodological adjustments occur at essential junctures of their depicted U-Curve, such because the sharp decline in revenue inequality that they depict throughout World Conflict II. It’s no coincidence that these identical years coincided with an overhaul of the tax code that standardized how the IRS collects and reviews revenue knowledge. On this occasion, we discovered that Piketty and his coauthors didn’t correctly appropriate for the accounting adjustments, and used an inaccurate estimate of complete private revenue earnings. Related errors pervade the complete Piketty-Saez collection.

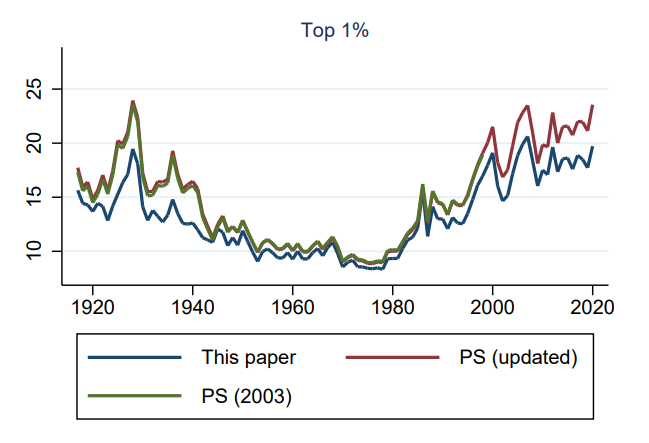

After correcting for these issues, we discovered that Piketty and his co-authors are likely to underestimate complete private revenue earnings, thereby artificially pumping up the revenue shares of the richest earners. They achieve this inconsistently although, as their largest underestimations are from the intervals between 1917-1943 and from 1986-present. These errors correspond exactly with the 2 highest intervals of inequality, the 2 tails of the U-shaped sample. Shifting to a constant methodology that does what Piketty and his co-authors aimed to do, however does so extra rigorously (we rigorously assembled year-by-year knowledge of nationwide accounts parts to create a constant definition moderately than use a “rule of thumb” as they did), exhibits that 40 % of the variations between Piketty and the work of Auten and Splinter is as a result of methodological inconsistencies of the previous.

In earlier works printed in The Financial Journal and Financial Inquiry, we additionally discovered different indicators of carelessness by Piketty and his acolytes with knowledge sources pre-1960. They used inconsistent definitions to hyperlink discontinuities in tax information. They omitted sure tax submitting information after misreading their knowledge sources. They made arbitrary choices about the right way to impute gaps of their knowledge, and used unreliable ratios to estimate the results of accounting adjustments by the IRS. Once we corrected all of those points, we discovered that inequality was far decrease within the Twenties than depicted. The decline didn’t begin within the Nineteen Forties — it began in 1929 and near two-thirds of it was accomplished by 1941. Once more, the mid-century trough was not as deep as depicted. The mixture of all work – the pre-1960 corrections and the century-long constant methodology may be seen within the graph under the place the U-curve is much much less pronounced and at a decrease stage.

Different works have confirmed these factors in another way. A small record of those suffices to indicate this. Miller et al. in an article in Overview of Political Financial system confirmed that many of the enhance from 1986 onward is because of tax shifting conduct linked to the 1986 Tax Reform. Armour et al. in an article within the American Financial Overview confirmed that correctly measuring capital positive aspects eliminates all the rise since 1989. In subsequent work within the Journal of Political Financial system, Armour et al. confirmed this discovering. Lastly, a Nationwide Bureau of Financial Analysis by Smith et al. confirmed that each one of those findings additionally apply to wealth inequality. Furthermore, work by Sylvain Catherine et al. from the College of Pennsylvania exhibits that Piketty and his crew failed to correctly think about the function of social safety which – when included – basically ranges the evolution of wealth inequality.

Usually, these findings could be trigger to revisit the traditional knowledge round Piketty’s narrative. The issues along with his underlying statistics are actually well-documented, and newer and higher estimates can be found to take their place. These estimates present a weaker U-curve with completely different timing and magnitudes for its evolution. Many of the decline to the trough is now not tied to tax charge adjustments however moderately to the results of the Nice Melancholy. Many of the enhance post-1986 is an artifice of accounting and may be in all probability higher attributed to adjustments within the returns to schooling in the course of the Nineteen Seventies, Nineteen Eighties and Nineteen Nineties which have since stabilized. General, the causal hyperlink between excessive taxes and low inequality (or the inverse situation) is now not obvious within the corrected knowledge, which exhibits a way more nuanced evolution of high revenue ranges over time. Certainly, one in every of Auten and Splinter’s essential findings exhibits that if you happen to take a look at high revenue ranges after taxes are paid, the highest 1 % has hovered round a steady 8 % revenue share for the final 60 years.

Because the research and measurement of inequality progresses, Piketty’s (and his crew’s) essential estimates have develop into out of date and is likely to be correctly consigned to the sector of the historical past of financial thought. Nevertheless, Piketty is now calling anybody who refuses to simply accept his stats an “inequality denier” and saying it’s equal to local weather denial.

Critics don’t deny inequality. They merely wish to measure it appropriately. Piketty’s personal knowledge are deeply suspect and open to challenges that he merely doesn’t wish to reply. Labeling his critics as “deniers” is a method of sidestepping the numerous issues along with his personal work. That alone warrants not solely discarding his estimates but in addition discounting any future analysis due to unhealthy tutorial conduct.

Phillip W. Magness

Phillip W. Magness is Senior Analysis College and F.A. Hayek Chair in Economics and Financial Historical past on the American Institute for Financial Analysis. He’s additionally a Analysis Fellow on the Unbiased Institute. He holds a PhD and MPP from George Mason College’s College of Public Coverage, and a BA from the College of St. Thomas (Houston). Previous to becoming a member of AIER, Dr. Magness spent over a decade instructing public coverage, economics, and worldwide commerce at establishments together with American College, George Mason College, and Berry Faculty. Magness’s work encompasses the financial historical past of america and Atlantic world, with specializations within the financial dimensions of slavery and racial discrimination, the historical past of taxation, and measurements of financial inequality over time. He additionally maintains an lively analysis curiosity in increased schooling coverage and the historical past of financial thought. His work has appeared in scholarly retailers together with the Journal of Political Financial system, the Financial Journal, Financial Inquiry, and the Journal of Enterprise Ethics. Along with his scholarship, Magness’s well-liked writings have appeared in quite a few venues together with the Wall Avenue Journal, the New York Instances, Newsweek, Politico, Purpose, Nationwide Overview, and the Chronicle of Greater Training.

Vincent Geloso

Vincent Geloso, senior fellow at AIER, is an assistant professor of economics at George Mason College. He obtained a PhD in Financial Historical past from the London College of Economics.

Observe him on Twitter @VincentGeloso