Star Holdings (STHO) (~$225MM implied market cap) is the upcoming spinoff of the merger of iStar (STAR) and Safehold (SAFE) focused to be accomplished on 3/31/23. Just like different actual property spinoffs, STHO will likely be filled with legacy property with a said technique to monetize the portfolio over time and return sale proceeds to shareholders.

iStar was a industrial mREIT previous to the nice recession, throughout ’08-’09 lots of their industrial mortgage loans went unhealthy and the corporate ended up foreclosing on numerous property varieties throughout the nation. Within the years since, they’ve run off a lot of that legacy portfolio (I beforehand owned it for the legacy property) after which a number of years again launched a brand new floor lease technique beneath the Safehold (SAFE) banner, a REIT that’s externally managed by iStar. Because the SAFE technique succeeded within the low price surroundings (a floor lease is usually 99 years, in regards to the longest length asset you will discover) and iStar’s legacy portfolio ran off, there was no use to keep up two separate public corporations with associated occasion preparations. iStar with its administration contract and SAFE shares was principally an asset backed monitoring inventory of SAFE. Final August, iStar and SAFE introduced a merger transaction the place SAFE would internalize administration and iStar would spinoff its non-ground lease property into STHO. Just like different actual property spins (SMTA, RVI, and many others), the brand new mixed SAFE would be the exterior supervisor of STHO.

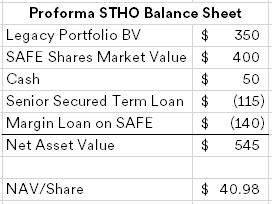

As standard in spinoffs now, iStar will likely be receiving a dividend again from STHO, the usage of funds is to pay down iStar’s debt and go away primarily simply SAFE shares to then swap for brand spanking new SAFE. So as to facilitate that dividend, STHO is receiving $400MM in SAFE shares that they are going to then take a $140MM margin mortgage out towards and ship that, plus a $115MM time period mortgage collateralized by all of STHO’s property again to iStar. The time period mortgage will amortize down shortly as all money above $50MM will sweep to pay down principal and the margin mortgage will likely be in place not less than 9 months per a lockup settlement on STHO’s SAFE shares. The proforma STHO appears to be like one thing like this (notice, the STHO share depend will likely be roughly 13.3 million, or 0.153 shares for each STAR share):

The legacy portfolio is a mixture of property, the 2 largest ones that account for roughly half of the e book worth are smaller grasp plan communities, one is Asbury Park Waterfront (a group of developed and pre-development combined use properties) on the Jersey Shore and Magnolia Inexperienced (a golf course centered 1900 acre single household residence neighborhood) simply outdoors of Richmond. STHO may even have some legacy industrial actual property loans and a parcel of land in Coney Island NY, they anticipate it is going to take 3-4 years to monetize a lot of the legacy property.

The trickier, and presumably scarier a part of STHO is the SAFE shares, as talked about, its principally a perpetual bond masquerading as an working firm. However with the speed curve considerably inverted, the market is pricing in fairly a couple of price cuts that will be useful to SAFE shares.

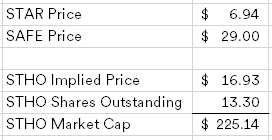

On March seventeenth, iStar put out a press launch estimating the consolidation ratio with SAFE (will probably be finalized instantly previous to the merger utilizing a VWAP calculation) at 0.15 shares of SAFE for every share of STAR. Utilizing that ratio we will again into the implied value of STHO:

At at the moment’s shut, until I made a dumb error (at all times doable), STHO shares are buying and selling at roughly 40% of e book worth. Shares might doubtlessly get even cheaper after the spinoff happens, STAR is a REIT and included in REIT indices, STHO will likely be a c-corp and can seemingly get bought by any REIT index funds (though the biggest ones like VNQ now embody non-REIT actual property corporations as nicely) and it will not pay a dividend. Proudly owning actual property proper now could be a bit scary, however STHO’s chunkier legacy property are tied extra to residential markets and we proceed to have a scarcity of housing on this nation.

The administration settlement can be value calling out right here, they’ve designed it to be a set charge versus a bps charge on property, with the fastened quantity happening annually to mirror the intention to liquidate over a 4ish yr interval. Many externally managed entities will commerce at a large low cost as a result of the property contained in the holdco won’t ever make it again to the shareholders, right here the low cost ought to slender additional time because the property are monetized and proceeds are used to both paydown debt or distribute again to shareholders.

Administration Charges and Expense Reimbursements

We don’t keep an workplace or make use of personnel. As an alternative, we depend on the amenities and assets of our supervisor to conduct our day-to-day operations.

We pays our supervisor an annual administration charge fastened at $25.0 million, $15.0 million, $10.0 million and $5.0 million in every of the primary 4 annual phrases of the settlement, and a pair of.0% of the gross e book worth of our property thereafter, excluding the Protected Shares, as of the top of every fiscal quarter as reported in our SEC filings. The administration charge is payable in money quarterly, in arrears. If we would not have adequate web money proceeds available from gross sales of our property or different obtainable sources to pay the administration charge in full by the unique due date of the administration charge, we pays the utmost quantity obtainable to us by the unique due date and the remaining shortfall will likely be carried ahead and be paid inside 10 days after adequate web proceeds have been generated by subsequent asset gross sales to cowl such shortfall in full; supplied that in no occasion could such shortfall in respect of any fiscal quarter stay unpaid by the 12 month anniversary of the unique due date.

I went synthetically lengthy STHO this week by shorting out 0.15 shares of SAFE for every share of STAR. You possibly can additionally go one step additional and quick out the SAFE shares that STHO will personal.

Disclosure: I personal shares of STAR and quick shares of SAFE (synthetically lengthy STHO)