{kind=link}

In Dec 2022, Mr Alam shared his monetary journey: From a internet price of Rs. 6000 to auto-pilot goal-based investing. He has shared particular particulars of investments on this follow-up.

About this sequence: I’m grateful to readers for sharing intimate particulars about their monetary lives for the advantage of readers. Among the earlier editions are linked on the backside of this text. You can even entry the total reader story archive.

Opinions printed in reader tales needn’t symbolize the views of freefincal or its editors. We should respect a number of options to the cash administration puzzle and empathise with numerous views. Articles are usually not checked for grammar except essential to convey the proper which means to protect the tone and feelings of the writers.

If you want to contribute to the DIY neighborhood on this method, ship your audits to freefincal AT Gmail dot com. They are often printed anonymously when you so need.

Please word: We welcome such articles from younger earners who’ve simply began investing. See, for instance, this piece by a 29-year-old: How I observe monetary targets with out worrying about returns. Now we have additionally began a brand new “mutual fund success tales” sequence. That is the primary version: How mutual funds helped me attain monetary independence.

First, some excerpts from Mr Alam’s first article. For full particulars pl see the hyperlink within the first paragraph. By 2021, I assumed that my funding was too messy, and I’m completely confused about what to do and the best way to do it. So I made a decision to satisfy a CFP and glued a gathering with him in my city. I discovered quite a lot of issues throughout the 3 hours of dialog. However he didn’t entertain me a lot as he was into dealing with monetary choices on his personal on behalf of his clients, and he would earn a fee by promoting common mutual funds. And I used to be not prepared for that. I felt it absurd to let others management my cash and funding technique.

So, I made a decision to do issues on my own. Sure, it won’t be simple. Sure, I’ll make errors. Sure, I will likely be confused. However I made myself mentally prepared for that. I began tagging my belongings to my targets.

When my different targets had been sorted effectively, I assumed primarily about “Little one Training Planning”. As a result of I used to be caught on this. If I can type this out, I also can type out retirement & marriage planning. I knew it. However I didn’t really feel comfy. So many questions got here to my thoughts.

So, I bought the “Objective Primarily based investing” course hoping to get extra solutions. I watched all of the movies and I acquired nearly all of the solutions about private finance that had been bothering me.

Then I felt that it was attainable to get into auto mode. I would like to purchase the “Robo Advisory Software“. I purchased it and nearly sorted all of the targets.

Then I felt that the MF objective tracker and inventory portfolio Tracker can be useful gizmo to visualise issues. I purchased it and began utilizing it.

I nearly sorted all the pieces now. I used to be a bit confused about some little issues. I wished to make use of my NSC quantity for my Little one’s Training and Retirement Planning. However I used to be confused about the best way to do it and use it within the calculator. So I wished to have a fruitful dialogue with a fee-only advisor.

I joined the AIFW Fb group after getting the knowledge from freefincal. I began to comply with, and it’s an amazing platform; members are so useful, trustworthy and educated. There I discovered Chandan Singh Padiyar Sir (you will get particulars from the fee-only advisor submit of Pattu sir) to be one of the energetic and trustworthy guys.

I attempted to rearrange a gathering with him, I didn’t need a strong monetary plan however to debate my thought course of about what I’m doing, if I’m committing a critical mistake. I don’t hassle about small errors, I’ll be taught from it and can rectify issues as per my capabilities. So, fortunately I acquired an opportunity to repair a gathering with him and he was so beneficiant to hearken to me, my drawback, my confusion and guided me in a easy approach which was extra vital. I used to be assured about what I’m doing, however after speaking to him I’m extra assured now.

Now I’m within the driver’s seat and I do know the place to go, when to go, and as I’ve a highway map I understand how to go. So, my funding journey is in auto-pilot mode now.

Emergency Fund:

- Financial savings Account

- Insta Redemption Liquid Fund (ICICI)

Time period Insurance coverage :

- 10X of annual revenue once I took

- HDFC Life – 5X

- TATA AIA – 5X

Well being Insurance coverage:

- HDFC ERGO – 10L

- Employer Advantages

Brief Time period Objective (upto 5 years):

For brief time period targets I take advantage of

- Liquid funds

- Cash Market funds

- FDs

- Extremely Brief Time period Fund (for >3 years)

CAR Objective (5 years away – versatile):

I thought of investing in Canara Robeco Fairness Hybrid fund with Canara Robeco Conservative Hybrid Fund as debt part. However I’ve to satisfy some quick time period targets. So, I received’t be capable to make investments for 15-16 months for this objective. So, I tagged a few of my beforehand invested funds and left it as it’s.

Fairness – weight 42% – XIRR 12%

- Parag Parikh Tax Saver fund – Weight 58% – XIRR 26%

- Axis Lengthy Time period fairness (tax) – Weight 33% – XIRR 11%

- Nippon alpha low volatility index fund – Weight 9% – XIRR (-8)%

Debt – weight 58% – XIRR 5%

- Canara Robeco Conservative Hybrid Fund

5 years to go (can stretch it to six to 7 years)

- Current Price – 8L

- Inflation – 6%

- PTRE (Publish tax return expectations) from fairness – 9%

- PTRE from Debt – 5%

- Plan – Depart it as it’s until I meet my quick time period objective, then I’ll give it some thought.

Little one Training (15 years away):

Fairness:Debt = 65:35

This was the hardest job for me. I used to be caught at this. However all due to the Objective Primarily based Portfolio Administration course and the Robo Advisory Software, all the pieces is in autopilot mode now.

In NOV 2022 the ratio was 100% fairness. I used to be Investing solely in fairness. I had a RD and I put 85% of the matured quantity in fairness funds. Later I spotted that regardless of how far a objective is, one can’t simply merely spend money on fairness and depart the funding on luck. If something like corona occurs throughout the objective completion yr, what’s going to occur to my fund? My hard-earned cash deserves higher therapy than that. I would like an asset allocation technique. So, I shifted some funds from fairness to debt and added some portion of my NSC (which is able to mature on NOV 2023) to make the ratio proper. It took me about 3 months to get all the pieces on observe as per my plan.

For Fairness I ended contemporary funding on energetic funds and selected UTI Low Volatility index fund and ICICI SENSEX index fund to speculate from now (60:40).

- Why not a easy Nifty 50 index fund? Effectively, I just like the idea of this issue based mostly index as it’s the easiest of all and the main focus is to have low volatility in my portfolio and that’s why I make investments 60% of the quantity on this index fund.

- The Remaining 40% I spend money on ICICI SENSEX fund.

- Mirae asset tax saver fund is kind of like a sensex index fund with a bit draw back efficiency. And in addition it has lock-in, so I’ve to maintain it and deal with it as an index hugger. ● Removed the opposite 2 energetic funds (Parag flexi + Axis small) and invested in index funds ● Sure, I’ve made some errors and that’s why I invested in so many funds for a objective, however it was my studying interval. However I’ve no regrets, a minimum of I attempted one thing.

For Debt, I used to be so confused. First, I selected a gilt fund (ICICI) to spend money on. Then I thought of having a conservative hybrid fund additionally. Then I felt that I’ve 15 years + . So, I can go along with PPF. ● Eventually I opened PPF for my spouse. I may also open a minor PPF and spend money on it. And I selected an Arbitrage fund for Rebalancing functions.

- PPF + Arbitrage – seems easy

- The gilt fund shouldn’t be wanted now, later at any time when I get probability I’ll take into consideration that ● When the NSC will mature, will make investments the quantity in PPF

Fairness Mutual Fund: (Weight – 65%)

- UTI Low Volatility Index – weight 60%

- ICICI SENSEX index – weight 7%

- Mirae tax saver – weight 33%

- These are latest investments, so XIRR doesn’t matter

Debt Devices : (Weight – 35%)

- PPF – weight 15%

- NSC – Weight 65%

- Arbitrage (Nippon) – Weight 20% – XIRR 5%

15 years to go

- Current Price – 30L

- Inflation – 11%

- PTRE from fairness – 9%

- PTRE from Debt – 6%

- Step up – 10%

- Plan – Cut back the fairness AA systematically from sixth yr onwards

- Remarks – I’m comfy however I don’t know whether or not I will pull it off or not as issues will hold altering alongside the journey as my daughter is simply <2years outdated. However I’ll strive my greatest.

Milestones

- To take a position greater than the Robo Advisory Software —— I’m already Investing about 30% extra recurrently than the quantity of Robo Advisory Software in order that’s factor.

- The present value of an undergraduate training matches the present worth of your youngster training portfolio ——- Complete Portfolio worth is sufficient for Personal Engineering School in Kolkata (I’ve finished engineering in a personal faculty).

- Complete Debt Portfolio worth is sufficient for Normal Programs in Kolkata

Daughter Marriage/House (22 years away):

Fairness:Debt = 67:33

Fairness – weight 67%

Debt – weight 33%

These are latest investments, so XIRR doesn’t matter

22 years to go

- Current Price – 12L

- Inflation – 8%

- PTRE from fairness – 10%

- PTRE from Debt – 6%

- Step up – 10%

- Plan – I’m investing at 67:33 (E:D). Investing just about lower than required because it’s the least vital objective as of now, simply to get it going. In a while I’ll make investments as per Robo Advisory Software when I’ll have cash to speculate, after completion of my CAR objective possibly.

Retirement (29 years away):

Fairness Mutual Fund: (Weight – 6%)

- UTI Nifty – weight 66%

- UTI Midcap 150 High quality 50 – weight 34%

- At the moment I’m investing – N50 : MC150Q50 = 2:1

- These are latest investments, so XIRR doesn’t matter

NPS: (Weight – 87.5 % & XIRR – 11%)

- I’ve opted Average Auto selection (HDFC PFM) in June 2022

- Upto 35 yrs of age – max fairness allocation 50% – Rebalancing occurs yearly (Delivery Date)

- From thirty sixth yrs of age, fairness will cut back by 2% annually until 55 years of age and it’ll come right down to 10% at 55 years of age

- Why Average auto selection? I’ve round 29 years for this objective. So, I’ve time. Being a central authorities worker, NPS is obligatory and is my most disciplined instrument with an amazing Investing CAGR of greater than 10% on a mean since mid 2016. Additionally I received’t should do something, no human intervention, additionally the fairness will systematically cut back with yearly Rebalancing. The one threat is that HDFC (Fairness) fund could or could not be capable to beat an index fund. However it doesn’t matter to me. For now, my total NPS is sort of a balanced hybrid fund and will likely be a conservative hybrid fund with a gilt majority at later phases. So, I’m okay with it.

Mounted Devices (Weight – 6.5 %)

- Time period deposit – weight 3 %

- My PPF – weight 3.5 %

General Portfolio Fairness: Debt = 50:50

29 years to go

- Inflation – 7% earlier than & 6% after

- PTRE from fairness – 10%

- PTRE from NPS – 8%

- Step up – 10%

- Plan – Improve the fairness Mutual Fund allocation as per my capabilities.

Milestones

- Your Retirement Planning could be set on auto-pilot —— Now it’s on autopilot mode as per calculation in Robo Advisory Software

- You possibly can reside off Your Internet Price for a sure variety of years

○ If I had been to retire right now, the present corpus will final for (years) – 3 years ○ If I had been to retire as supposed, I will likely be financially impartial for (years) – 5 years.

Reader tales printed earlier:

As common readers could know, we publish a private monetary audit every December – that is the 2020 version: How my retirement portfolio carried out in 2020. We requested common readers to share how they evaluate their investments and observe monetary targets.

These printed audits have had a compounding impact on readers. If you want to contribute to the DIY neighborhood on this method, ship your audits to freefincal AT Gmail. They may very well be printed anonymously when you so need.

Do share this text with your folks utilizing the buttons under.

🔥Get pleasure from large reductions on our programs and robo-advisory device! 🔥

Use our Robo-advisory Excel Software for a start-to-finish monetary plan! ⇐ Greater than 1000 buyers and advisors use this!

New Software! => Observe your mutual funds and shares investments with this Google Sheet!

- Observe us on Google Information.

- Do you’ve a remark in regards to the above article? Attain out to us on Twitter: @freefincal or @pattufreefincal

- Be a part of our YouTube Neighborhood and discover greater than 1000 movies!

- Have a query? Subscribe to our e-newsletter with this kind.

- Hit ‘reply’ to any e mail from us! We don’t provide personalised funding recommendation. We will write an in depth article with out mentioning your title when you have a generic query.

Get free cash administration options delivered to your mailbox! Subscribe to get posts through e mail!

Discover the positioning! Search amongst our 2000+ articles for data and perception!

About The Creator

Dr M. Pattabiraman(PhD) is the founder, managing editor and first creator of freefincal. He’s an affiliate professor on the Indian Institute of Expertise, Madras. He has over 9 years of expertise publishing information evaluation, analysis and monetary product growth. Join with him through Twitter or Linkedin, or YouTube. Pattabiraman has co-authored three print books: (1) You could be wealthy too with goal-based investing (CNBC TV18) for DIY buyers. (2) Gamechanger for younger earners. (3) Chinchu Will get a Superpower! for teenagers. He has additionally written seven different free e-books on varied cash administration matters. He’s a patron and co-founder of “Price-only India,” an organisation selling unbiased, commission-free funding recommendation.

Dr M. Pattabiraman(PhD) is the founder, managing editor and first creator of freefincal. He’s an affiliate professor on the Indian Institute of Expertise, Madras. He has over 9 years of expertise publishing information evaluation, analysis and monetary product growth. Join with him through Twitter or Linkedin, or YouTube. Pattabiraman has co-authored three print books: (1) You could be wealthy too with goal-based investing (CNBC TV18) for DIY buyers. (2) Gamechanger for younger earners. (3) Chinchu Will get a Superpower! for teenagers. He has additionally written seven different free e-books on varied cash administration matters. He’s a patron and co-founder of “Price-only India,” an organisation selling unbiased, commission-free funding recommendation.

Our flagship course! Be taught to handle your portfolio like a professional to attain your targets no matter market circumstances! ⇐ Greater than 3000 buyers and advisors are a part of our unique neighborhood! Get readability on the best way to plan on your targets and obtain the required corpus it doesn’t matter what the market situation is!! Watch the primary lecture totally free! One-time cost! No recurring charges! Life-long entry to movies! Cut back concern, uncertainty and doubt whereas investing! Learn to plan on your targets earlier than and after retirement with confidence.

Our new course! Improve your revenue by getting folks to pay on your abilities! ⇐ Greater than 700 salaried workers, entrepreneurs and monetary advisors are a part of our unique neighborhood! Learn to get folks to pay on your abilities! Whether or not you’re a skilled or small enterprise proprietor who needs extra purchasers through on-line visibility or a salaried particular person wanting a aspect revenue or passive revenue, we’ll present you the best way to obtain this by showcasing your abilities and constructing a neighborhood that trusts you and pays you! (watch 1st lecture totally free). One-time cost! No recurring charges! Life-long entry to movies!

Our new guide for teenagers: “Chinchu will get a superpower!” is now accessible!

Most investor issues could be traced to a scarcity of knowledgeable decision-making. We have all made dangerous choices and cash errors after we began incomes and spent years undoing these errors. Why ought to our kids undergo the identical ache? What is that this guide about? As mother and father, what would it not be if we needed to groom one capacity in our kids that’s key not solely to cash administration and investing however to any facet of life? My reply: Sound Choice Making. So on this guide, we meet Chinchu, who’s about to show 10. What he needs for his birthday and the way his mother and father plan for it and train him a number of key concepts of choice making and cash administration is the narrative. What readers say!

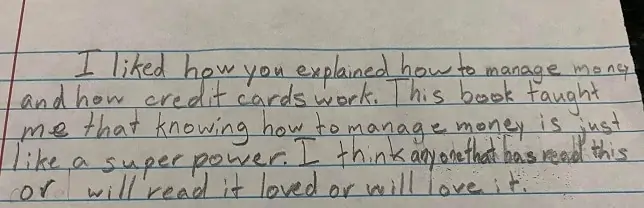

Should-read guide even for adults! That is one thing that each guardian ought to train their youngsters proper from their younger age. The significance of cash administration and choice making based mostly on their needs and desires. Very properly written in easy phrases. – Arun.

Purchase the guide: Chinchu will get a superpower on your youngster!

Tips on how to revenue from content material writing: Our new book for these enthusiastic about getting aspect revenue through content material writing. It’s accessible at a 50% low cost for Rs. 500 solely!

Need to test if the market is overvalued or undervalued? Use our market valuation device (it would work with any index!), otherwise you purchase the brand new Tactical Purchase/Promote timing device!

We publish month-to-month mutual fund screeners and momentum, low volatility inventory screeners.

About freefincal & its content material coverage Freefincal is a Information Media Group devoted to offering unique evaluation, experiences, evaluations and insights on mutual funds, shares, investing, retirement and private finance developments. We accomplish that with out battle of curiosity and bias. Observe us on Google Information. Freefincal serves greater than three million readers a yr (5 million web page views) with articles based mostly solely on factual data and detailed evaluation by its authors. All statements made will likely be verified from credible and educated sources earlier than publication. Freefincal doesn’t publish any paid articles, promotions, PR, satire or opinions with out knowledge. All opinions introduced will solely be inferences backed by verifiable, reproducible proof/knowledge. Contact data: letters {at} freefincal {dot} com (sponsored posts or paid collaborations won’t be entertained)

Join with us on social media

Our publications

You Can Be Wealthy Too with Objective-Primarily based Investing

Printed by CNBC TV18, this guide is supposed that can assist you ask the proper questions and search the proper solutions, and because it comes with 9 on-line calculators, you too can create customized options on your way of life! Get it now.

Printed by CNBC TV18, this guide is supposed that can assist you ask the proper questions and search the proper solutions, and because it comes with 9 on-line calculators, you too can create customized options on your way of life! Get it now.

Gamechanger: Overlook Startups, Be a part of Company & Nonetheless Stay the Wealthy Life You Need

This guide is supposed for younger earners to get their fundamentals proper from day one! It should additionally assist you journey to unique locations at a low value! Get it or present it to a younger earner.

This guide is supposed for younger earners to get their fundamentals proper from day one! It should additionally assist you journey to unique locations at a low value! Get it or present it to a younger earner.

Your Final Information to Journey

That is an in-depth dive evaluation into trip planning, discovering low cost flights, finances lodging, what to do when travelling, and the way travelling slowly is healthier financially and psychologically with hyperlinks to the net pages and hand-holding at each step. Get the pdf for Rs 300 (prompt obtain)

That is an in-depth dive evaluation into trip planning, discovering low cost flights, finances lodging, what to do when travelling, and the way travelling slowly is healthier financially and psychologically with hyperlinks to the net pages and hand-holding at each step. Get the pdf for Rs 300 (prompt obtain)