Just a few days in the past I gave a brief speak on the topic. I used to be partly impressed by just a little remark made at a seminar, roughly “in fact everyone knows that if costs are sticky, greater nominal charges increase greater actual charges, that lowers combination demand and lowers inflation.” Possibly we “know” that, however it’s not as readily current in our fashions as we expect. This additionally crystallizes some work within the ongoing “Expectations and the neutrality of rates of interest” venture.

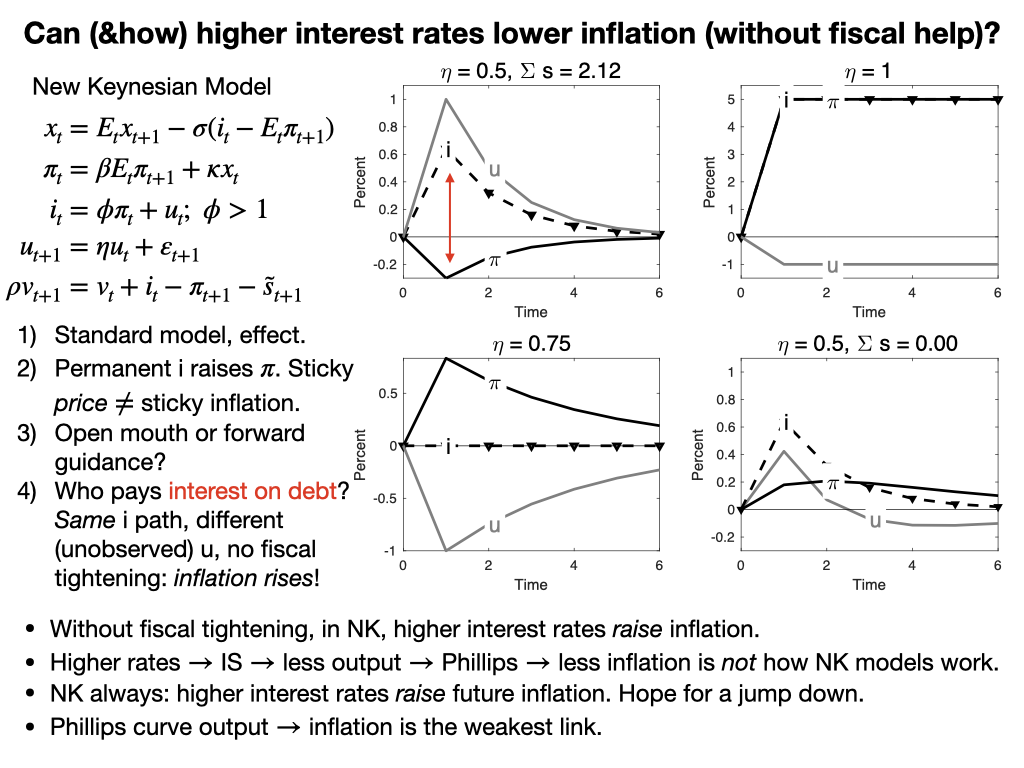

The equations are the completely commonplace new-Keynesian mannequin. The final equation tracks the evolution of the actual worth of the debt, which is often within the footnotes of that mannequin.

OK, prime proper, the usual outcome. There’s a optimistic however short-term shock to the financial coverage rule, u. Rates of interest go up after which slowly revert. Inflation goes down. Hooray. (Output additionally goes down, because the Phillips Curve insists.)

The subsequent graph ought to provide you with pause on simply the way you interpreted the primary one. What if the rate of interest goes up persistently? Inflation rises, all of the sudden and fully matching the rise in rate of interest! But costs are fairly sticky — ok = 0.1 right here. Right here I drove the persistence all the best way to 1, however that is not essential. With any persistence above 0.75, greater rates of interest give rise to greater inflation.

What is going on on? Costs are sticky, however inflation will not be sticky. Within the Calvo mannequin only some companies can change worth in any prompt, however they modify by a big quantity, so the speed of inflation can bounce up immediately simply because it does. I believe loads of instinct needs inflation to be sticky, in order that inflation can slowly choose up after a shock. That is the way it appears to work on the planet, however sticky costs don’t ship that outcome. Therefore, the actual rate of interest would not change in any respect in response to this persistent rise in nominal rates of interest. Now perhaps inflation is sticky, prices apply to the spinoff not the extent, however completely not one of the immense literature on worth stickiness considers that risk or how on the planet it is perhaps true, at the very least so far as I do know. Let me know if I am flawed. At a minimal, I hope I’ve began to undermine your religion that all of us have straightforward textbook fashions through which greater rates of interest reliably decrease inflation.

(Sure, the shock is unfavorable. Take a look at the Taylor rule. This occurs rather a lot in these fashions, another excuse you would possibly fear. The shock can go in a distinct path from observed rates of interest.)

Panel 3 lowers the persistence of the shock to a cleverly chosen 0.75. Now (with sigma=1, kappa=0.1, phi= 1.2), inflation now strikes with no change in rate of interest in any respect. The Fed merely publicizes the shock and inflation jumps all by itself. I name this “equilibrium choice coverage” or “open mouth coverage.” You possibly can regard this as a function or a bug. If you happen to imagine this mannequin, the Fed can transfer inflation simply by making speeches! You possibly can regard this as highly effective “ahead steering.” Or you may regard it as nuts. In any case, when you thought that the Fed’s mechanism for reducing inflation is to lift nominal rates of interest, inflation is sticky, actual charges rise, output falls and inflation falls, effectively right here is one other case through which the usual mannequin says one thing else totally.

Panel 4 is in fact my principal pastime horse nowadays. I tee up the query in Panel 1 with the crimson line. In that panel, the nominal curiosity are is greater than the anticipated inflation price. The actual rate of interest is optimistic. The prices of servicing the debt have risen. That is a critical impact these days. With 100% debt/GDP every 1% greater actual price is 1% of GDP extra deficit, $250 billion {dollars} per yr. Any person has to pay that ultimately. This “financial coverage” comes with a fiscal tightening. You may see that within the footnotes of fine new-Keynesian fashions: lump sum taxes come alongside to pay greater curiosity prices on the debt.

Now think about Jay Powell comes knocking to Congress in the course of a knock-down drag-out struggle over spending and the debt restrict, and says “oh, we’ll increase charges 4 share factors. We want you to lift taxes or lower spending by $1 trillion to pay these further curiosity prices on the debt.” Fun is perhaps the well mannered reply.

So, within the final graph, I ask, what occurs if the Fed raises rates of interest and financial coverage refuses to lift taxes or lower spending? Within the new-Keynesian mannequin there’s not a 1-1 mapping between the shock (u) course of and rates of interest. Many alternative u produce the identical i. So, I ask the mannequin, “select a u course of that produces precisely the identical rate of interest as within the prime left panel, however wants no extra fiscal surpluses.” Declines in curiosity prices of the debt (inflation above rates of interest) and devaluation of debt by interval 1 inflation should match rises in curiosity prices on the debt (inflation under rates of interest). The underside proper panel provides the reply to this query.

Overview: Identical rate of interest, no fiscal assist? Inflation rises. On this very commonplace new-Keynesian mannequin, greater rates of interest with out a concurrent fiscal tightening increase inflation, instantly and persistently.

Followers will know of the long-term debt extension that solves this downside, and I’ve plugged that answer earlier than (see the “Expectations” paper above).

The purpose right this moment: The assertion that we’ve straightforward easy effectively understood textbook fashions, that seize the usual instinct — greater nominal charges with sticky costs imply greater actual charges, these decrease output and decrease inflation — is solely not true. The usual mannequin behaves very in another way than you suppose it does. It is wonderful how after 30 years of enjoying with these easy equations, verbal instinct and the equations stay to date aside.

The final two bullet factors emphasize two different features of the instinct vs mannequin separation. Discover that even within the prime left graph, greater rates of interest (and decrease output) include rising inflation. At greatest the upper price causes a sudden bounce down in inflation — costs, not inflation, are sticky even within the prime left graph — however then inflation steadily rises. Not even within the prime left graph do greater charges ship future inflation decrease than present inflation. Widespread instinct goes the opposite means.

In all this theorizing, the Phillips Curve strikes me because the weak hyperlink. The Fed and customary instinct make the Phillips Curve causal: greater charges trigger decrease output trigger decrease inflation. The unique Phillips Curve was only a correlation, and Lucas 1972 considered causality the opposite means: greater inflation fools individuals briefly to producing extra.

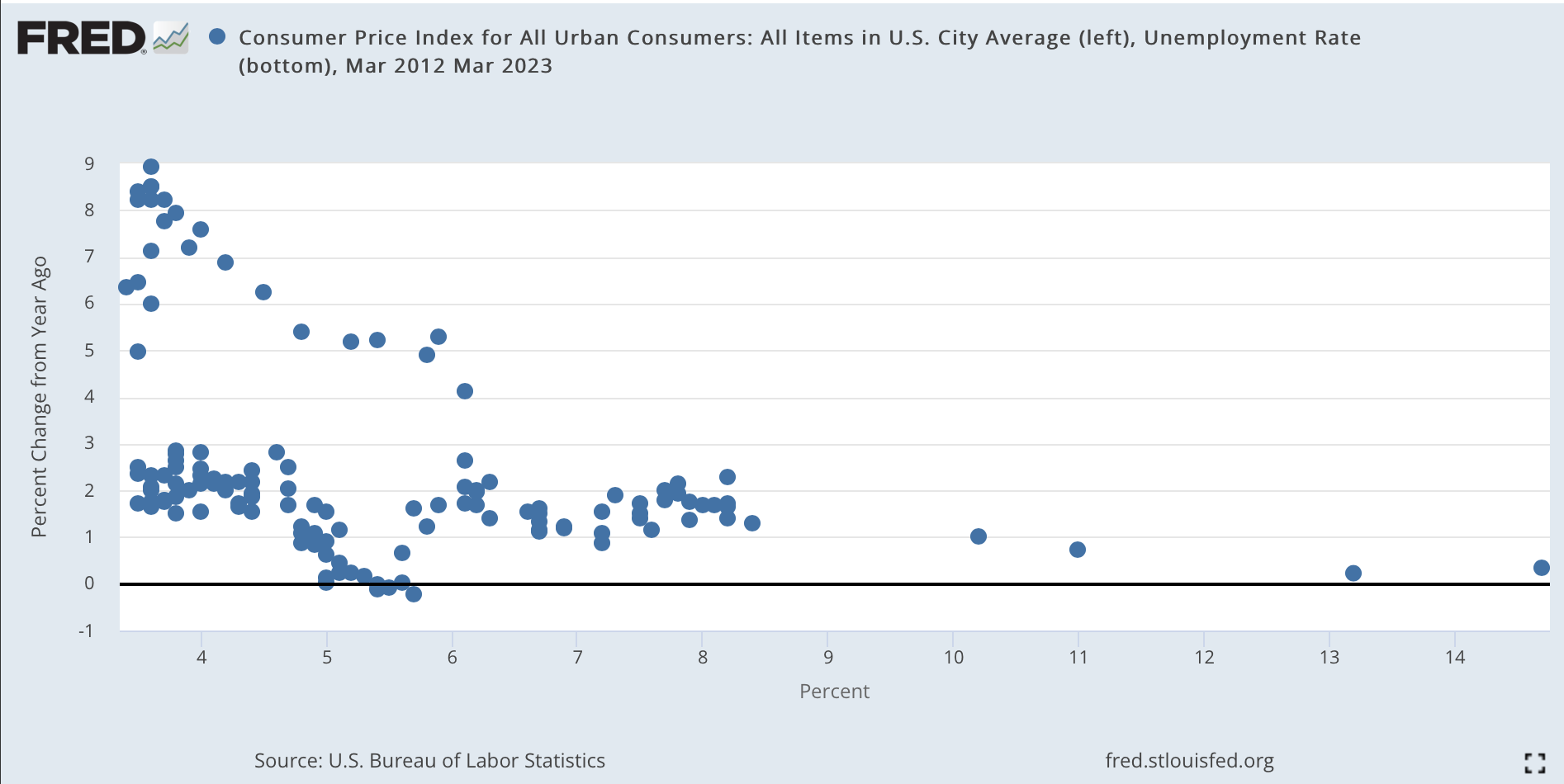

Right here is the Phillips curve (unemployment x axis, inflation y axis) from 2012 via final month. The dots on the decrease department are the pre-covid curve, “flat” as frequent knowledge proclaimed. Inflation was nonetheless 2% with unemployment 3.5% on the eve of the pandemic. The higher department is the newer expertise.

I believe this plot makes some sense of the Fed’s colossal failure to see inflation coming, or to understand it as soon as the dragon was contained in the outer wall and respiratory fireplace on the interior gate. If you happen to imagine in a Phillips Curve, causal from unemployment (or “labor market situations”) to inflation, and also you final noticed 3.5% unemployment with 2% inflation in February 2021, the 6% unemployment of March 2021 goes to make you completely ignore any inflation blips that come alongside. Certainly, till we get effectively previous 3.5% unemployment once more, there’s nothing to fret about. Effectively, that was flawed. The curve “shifted” if there’s a curve in any respect.

However what to place as a substitute? Good query.

Replace:

Numerous commenters and correspondents need different Phillips Curves. I have been influenced by quite a lot of papers, particularly “New Pricing Fashions, Identical Previous Phillips Curves?” by Adrien Auclert, Rodolfo Rigato, Matthew Rognlie, and Ludwig Straub, and “Value Rigidity: Microeconomic Proof and Macroeconomic Implications” by Emi Nakamura and Jón Steinsson, that numerous completely different micro foundations all find yourself wanting about the identical. Each are nice papers. Including lags appears straightforward, however it’s not that straightforward except you overturn the ahead wanting eigenvalues of the system; “Expectations and the neutrality of rates of interest” goes on in that means. Including a lag with out altering the system eigenvalue would not work.