{kind=link}

As life grows extra complicated and the advantages panorama will get even wider and in addition extra complicated, simplicity is now essential to workers and employers. Mockingly, a part of that simplicity will likely be offered by new and extra group and voluntary advantages. Simply as hospital indemnity helps to simplify the economics of an surprising hospital keep or pet insurance coverage serves to alleviate the stress of sick pets, up-and-coming advantages will simplify points of life that have an effect on work/life stability and monetary wellness.

BenefitBump is an instance of a brand new, revolutionary group profit that simplifies worker lives throughout the beginning and adoption course of, the household go away interval, and the start of daycare. Many employers have realized that there’s a substantial amount of complexity round these essential timeframes in a household. Busy workers don’t naturally know the best way to navigate all the ins and outs of their advantages. It can lead to a excessive price of those that don’t return to work.

BenefitBump educates workers on the particular person degree, assigning a navigator who provides steerage, well being instruments, and emotional help. Their preliminary survey statistics are spectacular, with “98% of program contributors efficiently returned to work.” Group insurer, Securian, now gives BenefitBump as a value-added service, paired with their hospital indemnity insurance coverage.[i]

Expertise + Shift in Possession

Everybody has been speaking in regards to the battle for expertise, the brand new technology of workers, and the expectations that immediately’s digital workers convey with them into the office. What they haven’t checked out as intently is the make-up of immediately’s enterprise homeowners and executives. At what level will their expectations and concepts on what is required for his or her companies and workers affect all the group & voluntary panorama?

Effectively, that time has arrived. GenZ and Millennials are proudly owning and working companies and they’re extremely perceptive about what advantages packages will inspire their worker friends. This leaves insurers looking for new gaps to fill. In Majesco’s newest thought-leadership report, Bridging the Buyer Expectation Hole: Group & Voluntary Advantages, we study SMB buyer opinions and the way they align in opposition to each worker expectations and insurer plans to satisfy these expectations.

Immediately’s buyer expectation hole

What’s the buyer expectation hole? The hole is the distinction between what clients anticipate, need, and want, as in comparison with what insurers are delivering. This hole must be as small as doable for insurers to create long-term buyer progress, worth, and loyalty. It calls for a customer-centric technique that understands the distinctive generational phase variations in behaviors, life, and extra, that drive insurers’ selections about merchandise, companies, and buyer experiences.

“Conventional” SMB clients – Gen X and Boomers – signify an unlimited portion of insurers’ income and revenue immediately. Many remained loyal to their insurer for years, even when they weren’t at all times 100% glad. Nonetheless, these “conventional” clients are altering. They’re more and more digitally adept and are in search of extra worth from insurers.

On the identical time, we’re seeing the rising dominance of SMB clients from the Gen Z and Millennial phase who seem like extra in tune with the altering wants and expectations of immediately’s workers – particularly the youthful technology – and the worth of providing newer and revolutionary profit choices to draw and maintain workers. They need new merchandise that can align with their wants, actions, and behaviors. And so they need it their method … customized to them. With the fluid state of employment that’s more and more widespread for the youthful technology, portability and suppleness of advantages have develop into crucial within the competitors for expertise.

The Gen Z and Millennial technology has the potential to reverse the rising safety hole for insurance coverage.

From a excessive within the mid-Nineteen Seventies, when 72% of adults and 90% of households with two-parent owned life insurance coverage,[ii] to a brand new 50-year low in 2010 when solely 44% of US households had particular person life insurance coverage, based mostly on LIMRA’s 2010 life insurance coverage research.[iii] A February 2017 LIMRA research famous that employment-based advantages (group and voluntary) life insurance coverage coated extra folks than particular person life insurance coverage as of 2016. Encouragingly, a current evaluation discovered 50% of North American employers which might be at the moment not providing voluntary advantages are contemplating including them. Plus, 40% who do provide them want to add extra advantages[iv] which might assist shut the safety hole.

This altering market dynamic highlights progress alternatives for insurers who can provide advantages that meet a extra numerous worker base. Insurers have a chance to supply the appropriate merchandise, value-added companies, and experiences to assist SMBs navigate these challenges and place their companies for progress.

Savvy, revolutionary corporations are redefining insurance coverage from an outside-in perspective to adapt to what clients – of any technology — need and anticipate, as a substitute of following the generations-long apply of an inside-out perspective that requires clients to adapt to the best way insurance coverage works. Consequently, these revolutionary corporations are reworking insurance coverage from a mysterious, complicated, and tough ordeal most would moderately keep away from, to a extra clear, easy, and fascinating expertise.

To know the client expectation hole, Majesco used the outcomes of our SMB, Client, and Insurer Strategic Priorities analysis to evaluate the variations between clients and insurers with a three-pronged hole mannequin view that features customized pricing with information/product, value-added companies, and distribution channels.

Expertise and Profit Choices

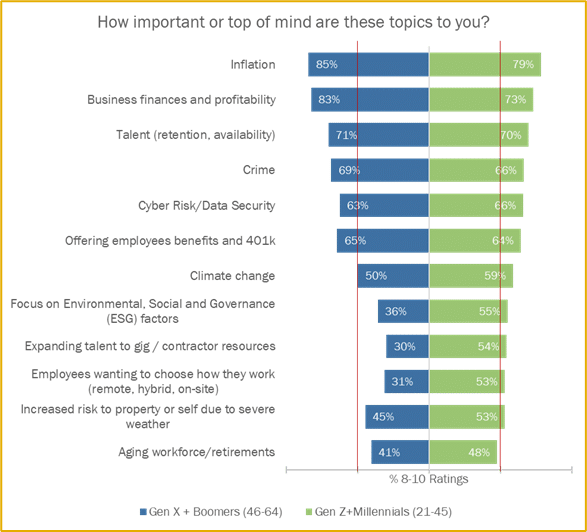

Majesco took a detailed take a look at enterprise homeowners’ top-of-mind points. Expertise and profit choices are #3 and #6, respectively, as seen in Determine 1. Within the battle for expertise, a advantages plan that provides decisions based mostly on completely different demographics, together with generational teams and life-style, could make the distinction between attracting star performers or just lacking out, impacting the enterprise positively or negatively. Because of this employers are more and more seeking to provide a wider vary of merchandise which might be related and stand out from the group, whatever the measurement of the enterprise.

Determine 1: SMBs’ high of thoughts points

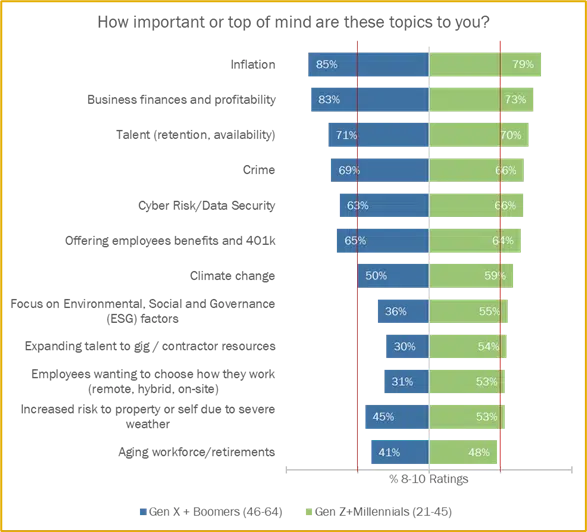

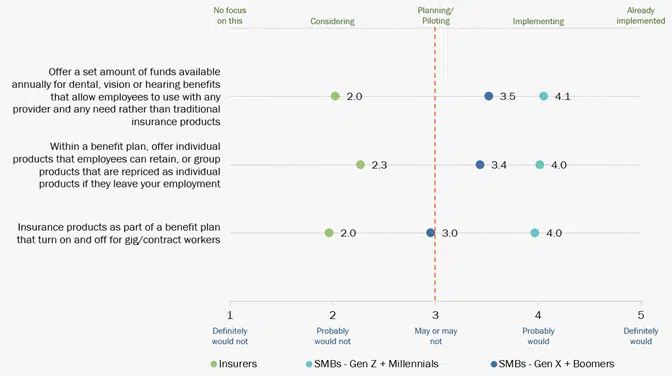

For insurers making the most of this chance, it’s not with out its challenges. The everyday American now holds a median of 12.3 jobs between the ages of 18 and 52, with roughly half of those occurring earlier than the age of 25.[v] Moreover, the Gig economic system now accounts for about 35% of the US workforce in some kind (whether or not a full-time occupation or part-time) and rising, and demand for extra fractional protection linked to Gig employees’ itinerant careers presents a problem.[vi] As such, switching employers is going on extra, leaving the necessity for insurance coverage a possible hole or alternative, relying on the product and portability. The demand for these capabilities is excessive, as mirrored in Determine 2 by each generational teams of SMB homeowners.

Determine 2: SMBs’ curiosity in providing new worker profit plan choices

The voluntary advantages market is powerful with exercise as accountability has shifted from employer to worker for a lot of nonmedical, health-related insurance coverage merchandise, with robust curiosity mirrored in rising gross sales.

Nonetheless, immediately’s merchandise nonetheless development towards the normal — targeted on life, accident, incapacity, medical, dental, and A&H, missing innovation and solutions for brand spanking new wants and expectations, significantly for Millennials and Gen Z.

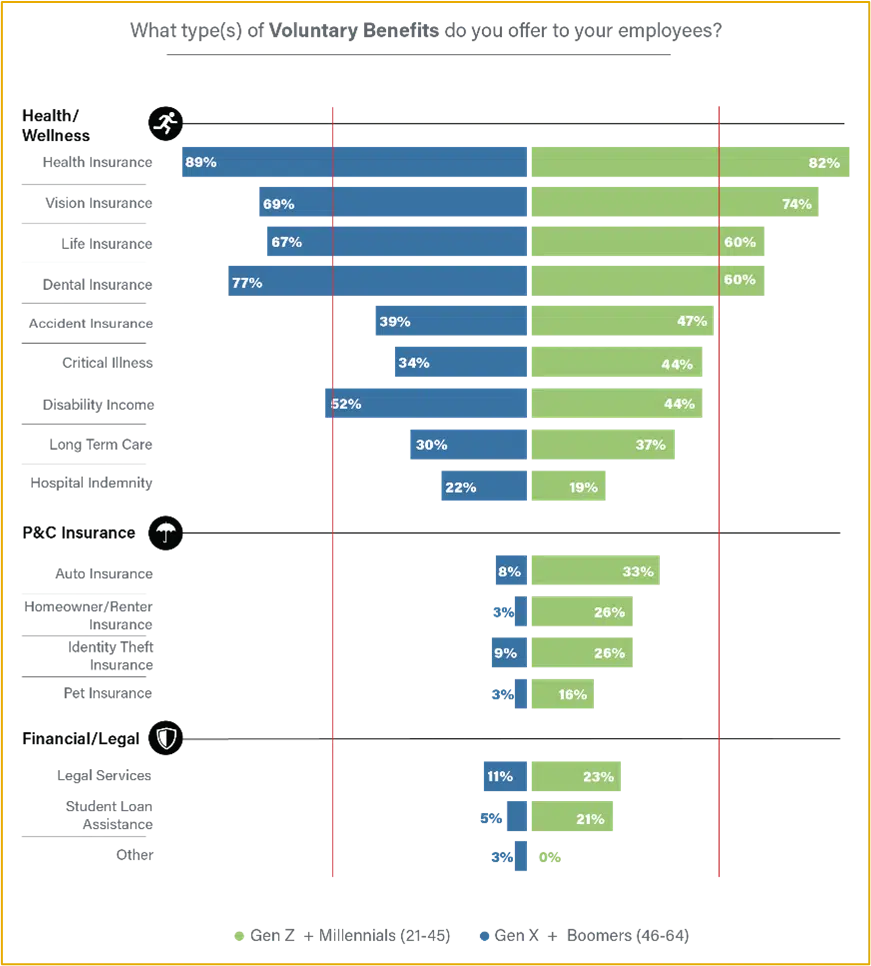

Insurers who can provide choices past conventional product boundaries have a chance to seize new clients extra cost-effectively and develop the connection as they evolve alongside their life journey. Creating, partnering, and providing merchandise that meet the worker’s distinctive rapid wants, whereas engaging them to remain as a buyer in the event that they go away their employer, is a rising technique amongst main insurers. That is mirrored in Determine 3 the place the youthful technology of SMB homeowners has a powerful, rising curiosity in different merchandise.

Determine 3: Voluntary advantages supplied by SMBs

It follows that any new or revolutionary choices that improve workers’ safety and help employer struggle for expertise would provide progress alternatives for insurers. The problem for conventional group and advantages insurers is knowing what new choices and plans can place them because the supplier with alternative, to drive extra engagement, enrollment, and shopping for of particular merchandise.

That is the place next-gen clever core and enrollment methods might help personalize and drive this progress alternative.

Progressive Advantages and Monetary Wellness Merchandise

Immediately’s clients desire a threat product, value-added companies, and an expertise that gives them with what they should handle their lives and humanize all the buyer lifecycle. Conventional merchandise can handicap insurers. From an elevated curiosity in life, important sickness, and incapacity insurance coverage to telematic and Gig advantages and extra, clients need revolutionary merchandise that assess their private threat, life-style, and behaviors.

This demand for revolutionary merchandise is seen in Determine 4 with each generational SMB teams having a excessive demand for them. Employers of all ages have gotten more proficient and understanding worker wants and becoming these wants into the group’s profit choices.

Sadly, most insurers, nevertheless, haven’t but responded to this want. Providing particular person merchandise which might be each moveable and cost-effective, and merchandise that may activate and off for Gig employees is predicted, but in addition wanted, given the shift within the worker market. With extra companies turning to Gig employees and needing merchandise extra aligned with the fact of worker expectations, insurers have an enormous alternative to distinguish and drive progress because the office continues to quickly change.

Determine 4: Curiosity gaps between SMB and Insurers in new profit plan choices

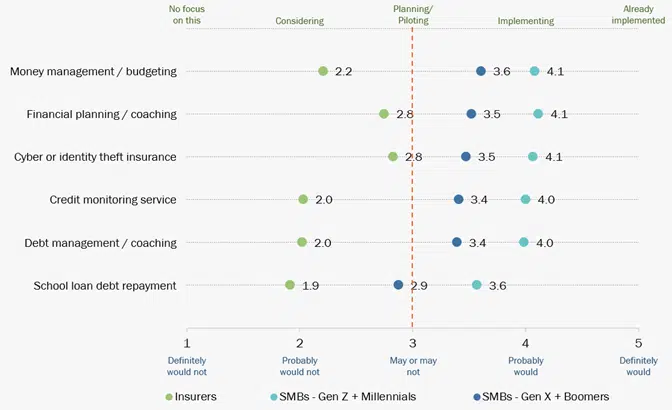

Monetary wellness is about adopting new practices and options to guide a extra wholesome and financially safe life. Training monetary wellness ranges throughout budgeting, defending property like houses and vehicles, saving, investing, and using insurance coverage to satisfy short- and long-term monetary objectives.

Rising buyer curiosity in monetary wellness will be attributed to many elements. Definitely, the COVID pandemic performed a task. The expanded use of wearable gadgets that observe coronary heart price, sleep cycles, and health exercise has motivated many people to stay more healthy lives. And a booming wellness economic system demonstrates that persons are keen to put money into their wellness. For SMBs, managing the monetary and operational points that maintain the enterprise working and wholesome – the SMB’s monetary wellness – has been difficult because of the macroeconomic elements post-COVID.

In keeping with a CNBC+ survey, solely 57% of adults in the US are financially literate, which means that 43% usually are not utilizing the appropriate instruments or lack the information to funds or make investments.[vii] Moreover, as acknowledged in a current LendingClub press launch, 63% of Individuals reside paycheck-to-paycheck and haven’t been capable of attain a degree of monetary wellness.[viii] And for companies, the rising inflation and provide chain challenges, not to mention the struggle for expertise, are straining their quick and long-term monetary outcomes. Because of this it has risen as a top-of-mind situation.

On condition that insurance coverage is a significant element of monetary wellness, it will replicate an amazing alternative for insurers to supply options. Nonetheless, as seen in Determine 5, there’s a main buyer expectation hole in what insurers are providing. This displays a unbroken enterprise mannequin and tradition of product- versus customer-driven methods inside insurers that won’t reach a customer-driven market.

Determine 5: SMB-Insurer gaps in monetary wellness value-added companies

The Group and Voluntary alternative x 10

Group and Voluntary insurance coverage services and products have at all times been about multiplication. “How can we place massive volumes of enterprise on the books abruptly?” With immediately’s applied sciences, that dynamic is turning into, “How can we place new, revolutionary merchandise that resonate with the range of life and wishes of workers whereas serving to employers to develop loyalty and entice the very best expertise?” It’s nonetheless a matter of multiplication, however in immediately’s state of affairs, it’s additionally about retention, flexibility, and treating the worker as the middle of the advantages relationship. It’s a strategic shift which will end in far better outcomes.

As corporations try to distinguish themselves with potential workers, they’re working a race that wants assist. Group and voluntary insurers want to arrange themselves to help correctly by using applied sciences and processes that may make all of it occur.

Is your organization able to serve the subsequent technology of employers? Majesco has created options for group and voluntary advantages that won’t solely convey insurers into the digital age however may also put together to present the information and analytic suggestions insurers and employers must optimize their choices. We’re working with a number of insurers who’re bringing revolutionary group and advantages merchandise to market, together with value-added companies to satisfy the calls for of a quickly altering employer and worker market.

Discover out extra about Majesco’s market-leading options that convey what you want for the longer term immediately together with L&AH Clever Core Suite, ClaimVantage IDAM, International IQX Gross sales and Underwriting, and Enroll360 options[DG1] which might be serving to Group and Voluntary insurers meet the rising calls for of employers and their workers.

For extra on this subject, be sure you learn, Wished: Group and Voluntary Merchandise to Enhance Worker Engagement & Loyalty, and obtain, Bridging the Buyer Expectation Hole: Group & Voluntary Advantages.

[i] “Securian Monetary collaborates with “BenefitBump” to boost schooling amongst expectant mother and father,” Press launch, Securian.com, September 29, 2022.

[ii] Dahl, Corey, “A short historical past of life insurance coverage,” ThinkAdvisor, September 9, 2013, https://www.thinkadvisor.com/2013/09/09/a-brief-history-of-life-insurance/

[iii] Ibid.

[iv] Howe, Barbara, “A Recent Take a look at Voluntary Advantages,” Company Wellness Journal.com, https://www.corporatewellnessmagazine.com/article/a-fresh-look-at-voluntary-benefits

[v] “Variety of Jobs, Labor Market Expertise, Marital Standing, and Well being: Outcomes from a Nationwide Longitudinal Survey,” Bureau of Labor Statistics, August 31, 2021, https://www.bls.gov/information.launch/pdf/nlsoy.pdf

[vi] Henderson, Rebecca, “How COVID-19 Has Reworked The Gig Economic system,” Forbes, December 10, 2020, https://www.forbes.com/websites/rebeccahenderson/2020/12/10/how-covid-19-has-transformed-the-gig-economy/?sh=42b329d16c99

[vii] Lorsch, Emily, “Because of this Individuals can’t handle their cash,” CNBC, April 8, 2022, https://www.cnbc.com/video/2022/04/08/financial-literacy-in-america.html

[viii] “Wages Have Didn’t Match Inflation, 65% of Employed Shoppers are Dwelling Paycheck to Paycheck,” LendingClub press launch, October 24, 2022, https://ir.lendingclub.com/information/news-details/2022/Wages-Have-Failed-to-Match-Inflation-65-of-Employed-Shoppers-are-Dwelling-Paycheck-to-Paycheck/default.aspx