{kind=link}

It’s necessary to overview your tax return.

Folks not often overview their tax return, and in the event that they do, they usually don’t overview it correctly. They might overview it to verify all the things is correct, however they don’t take into consideration frequent tax planning errors they might be making.

They don’t plan the best way to scale back their lifetime tax invoice, akin to with Roth conversions, charitable gifting, or gifting to members of the family.

Let’s have a look at the best way to overview your tax return and search for tax planning alternatives.

Please be aware that I’m reviewing tax planning errors from the angle of somebody who’s retired or soon-to-be retired

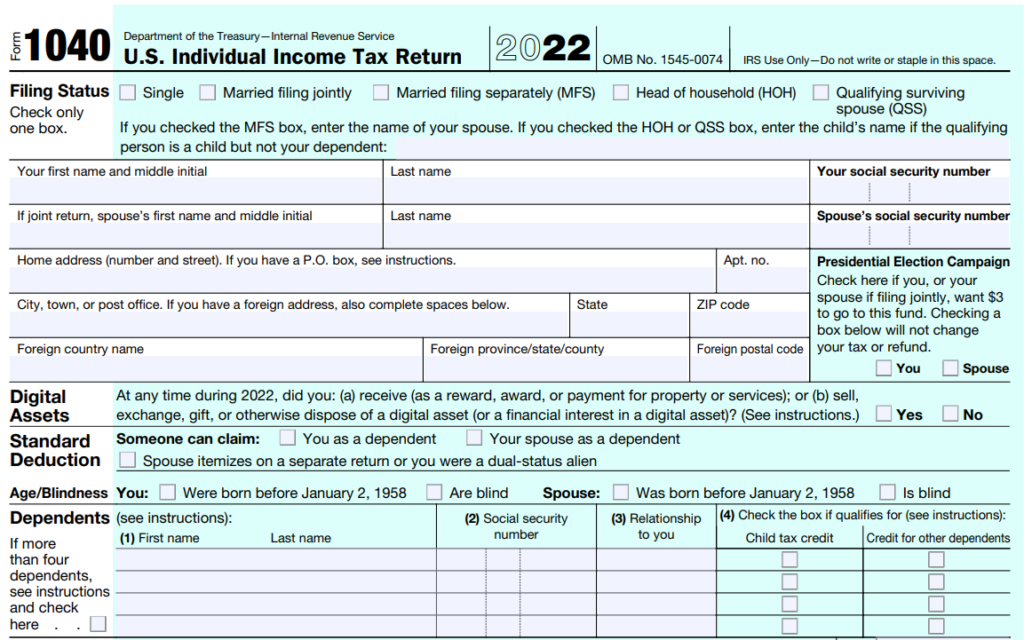

Earlier than Line 1: Submitting Standing, Title, SSN, Tackle, Digital Property, and Dependents

Earlier than line 1 are the simpler components to finish. There usually are not many tax planning alternatives on this part, however there are lots of areas to make errors.

Submitting Standing

For married folks, submitting individually not often ends in decrease taxes than submitting collectively.

If you’re a widow and your partner died this 12 months, you may nonetheless file collectively, although this can be your final 12 months to file collectively.

Solely underneath restricted circumstances can a widow file as Qualifying Surviving Partner (QSS), the place she should still use the married submitting collectively tax brackets. Qualifying Surviving Partner standing requires the surviving partner to have a dependent youngster residing with all of them 12 months, and paid greater than half of the fee to maintain up the house. It’s additionally restricted to 2 years following the 12 months of the partner’s loss of life if the surviving partner stays single.

For single folks, they usually file as Single.

Head of Family not often applies until you offered greater than half the assist for a kid or mother or father that was residing with you for at the least half of the 12 months.

Title

Double examine that you simply spelled your title appropriately.

Social Safety Numbers

A standard tax submitting mistake is incorrectly getting into Social Safety numbers. Are yours right?

Tackle

For the reason that IRS will use this tackle to correspond with you, is it correct?

If you could replace your tackle with the IRS, you may replace it utilizing Type 8822.

Digital Property

Reply this query rigorously. Given the hype in digital property the previous few years, you will have obtained a digital asset as a reward or exchanged, gifted, or offered it.

The IRS is growing scrutiny on this space.

Dependents

Many retirees wouldn’t have dependents, however when you do, guarantee another person shouldn’t be claiming them as a dependent as a result of it might decelerate the processing time.

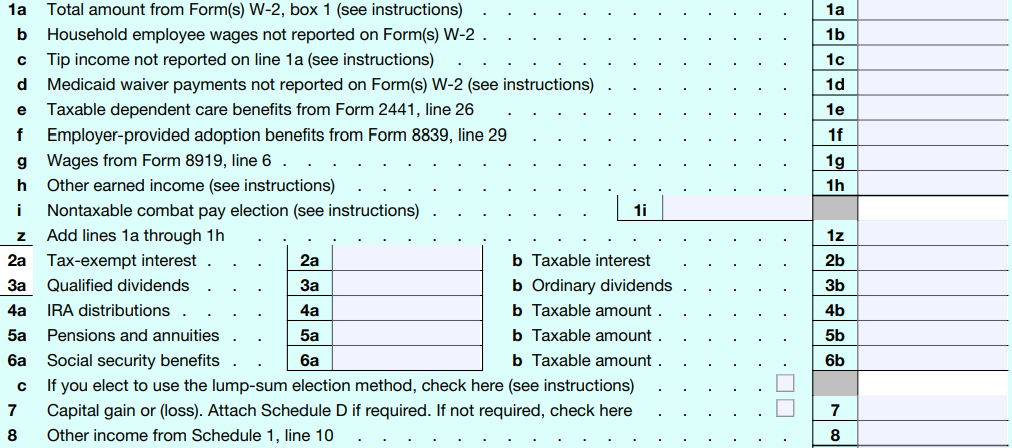

Traces 1 – 8: Earnings Sources

These are the areas the place tax planning alternatives begin to exist.

Line 1: Wages

Many retirees don’t have wages, however if you’re not retired but, listed here are a pair methods to contemplate:

- Employer Retirement Plans

- Are you taking full benefit of a match?

- Are you contemplating your tax bracket at present versus in retirement in deciding whether or not to contribute to the pre-tax or Roth portion of the plan?

- Does your plan enable for after-tax contributions and in-plan Roth conversions? If that’s the case, does it make sense to contribute?

- Well being Financial savings Accounts (HSAs): If in case you have a high-deductible well being plan that qualifies for an HSA, are you contributing via work?

Line 2a and 2b: Tax-exempt curiosity and taxable curiosity

Line 2a is often municipal bond curiosity, which is tax-exempt curiosity on a federal degree.

If the municipal bond was issued by your state of residence, the curiosity is often tax-free in your state tax return. For instance, when you had a California municipal bond and resided in California, the municipal bond curiosity could also be tax-free in your California state tax return.

Line 2b is taxable curiosity, which may very well be curiosity from financial institution accounts and company bond curiosity in brokerage accounts.

Planning Tip: Relying in your tax bracket and the way a lot municipal bonds are yielding versus company bonds, you might be higher off proudly owning municipal bonds over company bonds in your brokerage account. For instance, if you’re within the 32% federal tax bracket and municipal bonds are yielding 4% whereas company bonds are yielding 6%, your tax equal yield for the municipal bond is 5.89%. That’s calculated utilizing the next formulation: (tax-free municipal bond yield)/(1 – tax charge). On this case, the company bonds are nonetheless yielding greater than the tax equal yield, so it might be higher to personal company bonds as an alternative of municipal bonds — although have in mind the danger ranges could also be totally different.

Planning Tip: Schedule B will record the place you might be receiving curiosity from. If in case you have a number of financial institution accounts and brokerage accounts, you might wish to take into account simplifying the variety of accounts.

Don’t overlook to report all curiosity earned. Though the shape 1099-INT is just produced when you earn at the least $10 in curiosity, you continue to have to report all curiosity earned, even whether it is lower than $10 and also you didn’t obtain a 1099-INT type.

Lastly, are you holding an excessive amount of money? If in case you have massive quantities of curiosity, that might point out you’ve got extra cash than you want. How a lot money you want in retirement is a private choice.

Line 3a and 3b: Certified Dividends and Extraordinary Dividends

Line 3a exhibits certified dividends, that are taxed extra favorably than extraordinary dividends as a result of they’re taxed at long-term capital beneficial properties tax charges.

Line 3b exhibits extraordinary dividends, that are taxed as extraordinary earnings, which is much less favorable.

Planning Tip: If in case you have increased extraordinary dividends, decide which funding is producing them. You might wish to rebalance your portfolio to make it extra tax environment friendly. Bond ETFs generate extraordinary dividends. You might wish to use asset location and maintain them in a tax-preferential account, akin to an IRA. That needs to be balanced with how a lot cash is required within the near-term for withdrawals out of your brokerage account.

Planning Tip: If in case you have accounts at a number of custodians, take into account consolidating to make it simpler to trace your asset allocation, scale back the variety of tax reporting kinds, and make it simpler to entry your cash.

Line 4a and 4b: IRA Distributions

Line 4a lists the whole IRA distributions. Line 4b lists the taxable quantity of these distributions.

In the event you do a Roth conversion and have after-tax foundation in your IRA, the taxable quantity on line 4b needs to be lower than line 4a since a portion shouldn’t be taxable. Type 8606 will report your non-deductible IRA contributions, distributions, and Roth conversions when you’ve got after-tax foundation and make the professional rata calculation of how a lot is taxable.

Planning Tip: In the event you did a Certified Charitable Distribution (QCD), you’ll have to account for it in your tax return. The 1099-R you obtain will present the whole distribution, however received’t separate the quantity that went to charity through a QCD. For instance, when you took a $20,000 distribution and $5,000 of it was a QCD, line 4a ought to record $20,000 and line 4b ought to record $15,000.

Line 5a and 5b: Pensions and Annuities

Line 5a exhibits whole earnings from pensions and annuities whereas line 5b exhibits the taxable quantity.

In the event you give up a non-qualified annuity, not all of it needs to be taxable. Line 5b needs to be lower than 5a.

Line 6a and 6b: Social Safety Advantages

Line 6a lists the whole Social Safety advantages whereas line 6b lists the taxable quantity.

Line 6a shouldn’t be what’s paid to you — it’s the gross, or whole, quantity earlier than Medicare prices, IRMAA changes, or extra tax withholdings.

Not all Social Safety advantages are topic to tax. At most, 85% of Social Safety advantages are taxable. In some circumstances, Social Safety advantages usually are not taxable in any respect. The quantity of Social Safety advantages which are taxable is predicated on “Provisional Earnings.”

Provisional Earnings = Adjusted Gross Earnings (AGI) + ½ of your Social Safety Advantages + Tax-Exempt Curiosity

Decreasing your earnings may make much less of your Social Safety advantages topic to taxation.

Planning Tip: In some circumstances, it might make sense to undo submitting for Social Safety advantages or suspending Social Safety advantages to enable extra room for Roth conversions and profit from delayed Social Safety retirement credit.

Line 7: Capital Acquire or Loss

Line 7 lists your capital beneficial properties or losses, which may very well be from promoting property in a brokerage account, capital acquire distributions from mutual funds, a house sale, or different tangible property.

Planning Tip: If in case you have massive capital acquire distributions from tax-inefficient mutual funds, you might wish to take into account the tax penalties of promoting versus the tax penalties of remaining within the fund in future years.

Planning Tip: If in case you have a $3,000 capital loss carry ahead, you will have different losses you need to use to offset future capital beneficial properties. You possibly can use these losses to promote different property with capital beneficial properties and probably offset them.

Line 8: Different Earnings

Line 8 lists different earnings, which may embrace many alternative sources, akin to:

- Taxable refunds

- Alimony

- Enterprise earnings

- Rental actual property, royalties, trusts, S firms

- Playing earnings

- Jury obligation pay

- Inventory choices

- Pastime earnings

Planning Tip: These are areas the place you wish to make sure you might be correctly reporting earnings and taking any acceptable deductions, akin to enterprise bills and rental depreciation. It might make sense to work with an accountant to make sure you’re taking the suitable deductions and reporting earnings correctly.

Traces 9 – 15: Whole Earnings, Adjusted Gross Earnings, Itemized Deductions/Commonplace Deduction, Certified Enterprise Earnings, and Taxable Earnings

Now that your earnings is accounted for, it’s time to whole it, take deductions, and decide your taxable earnings.

Line 9: Whole Earnings

Line 9 is including your whole earnings from strains 1 via 8.

Line 10: Changes to Earnings from Schedule 1

Line 10 are changes to earnings from Schedule 1, which incorporates classes akin to:

- Well being Financial savings Account (HSA) contributions

- Deductible a part of self-employment tax for self-employed folks

- Self-employed certified plan contributions

- Self-employed medical insurance deduction

There are others, and they’re much less frequent, however overview Schedule 1 to be sure to are accounting for all changes.

Planning Tip: If in case you have entry to an HSA, take into account investing it for future medical bills and spend cash on present healthcare bills with money. Additionally, when you have an HSA with poor funding choices or excessive bills, take into account shifting it to a different supplier.

Line 11: Adjusted Gross Earnings (AGI)

Line 11 is your Adjusted Gross Earnings (AGI), which elements into many different calculations.

AGI can have an effect on your Modified Adjusted Gross Earnings (MAGI) and eligibility for particular deductions, credit, and different applications, akin to:

- Medicare IRMAA surcharges

- ACA medical insurance premium tax credit, which might decrease the price of medical insurance via a state or federal medical insurance market

- Whether or not you can also make contributions to a Roth IRA

- Whether or not you may deduct IRA contributions

- Web Funding Earnings Tax (NIIT)

- Baby tax credit score

- Training credit

Planning Tip: Pay particular consideration to your AGI and the way it might have an effect on what accounts you may contribute to, credit you might be eligible for, IRMAA surcharges, and extra taxes. For instance, a Roth conversion can have an effect on your AGI and trigger an IRMAA surcharge that will increase the price of your Medicare.

Line 12: Commonplace Deduction or Itemized Deductions

Line 12 is both taking the usual deduction, or in case your itemized deductions whole greater than your normal deduction, taking itemized deductions.

The usual deduction for 2023 is $13,850 for single filers (plus $1,850 if age 65 or older) and $27,700 for married submitting collectively (plus $1,500 per individual if age 65 or older).

Attainable itemized deductions embrace:

- State and native earnings or gross sales taxes

- Actual property taxes

- Private property taxes

- Mortgage curiosity (together with factors on a brand new mortgage)

- Catastrophe losses

- Presents to charity (together with unused carryover quantities as much as 5 years)

- Medical and dental bills

Planning Tip: If you’re charitably inclined, you may take into account “bunching” a number of years’ price of gifting right into a single 12 months to recover from the brink for itemizing deductions. You possibly can even think about using a Donor-Suggested Fund to make grants to charities over an extended timeframe than one 12 months.

Line 13: Certified Enterprise Earnings Deduction

Line 13 is Certified Enterprise Earnings Deduction, which permits homeowners of pass-through enterprise to probably deduct as much as 20% of their certified enterprise earnings. There are earnings limits and different limitations to concentrate on. with the QBI deduction.

If you’re nonetheless working and self-employed, you might qualify for the QBI deduction. If you’re retired, you might even see small quantities of a QBI deduction as a result of REIT dividends held in a brokerage account.

Line 15: Taxable Earnings

Line 15 is taxable earnings, which helps you identify your federal marginal tax bracket and your whole tax.

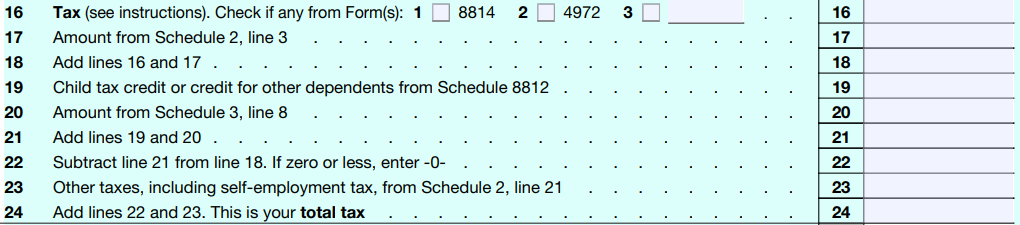

Traces 16 – 24: Tax and Credit

Now that you already know your taxable earnings, let’s have a look at what you owe.

Line 16: Tax

Line 16 is the whole quantity of tax you owe earlier than any credit, different minimal tax (AMT), reimbursement of ACA medical insurance premium tax credit, and different changes.

Line 17: Quantity from Schedule 2, Line 3

Line 17 has to do with extra taxes from Schedule 2, which is the choice minimal tax or reimbursement of the ACA medical insurance premium tax credit.

AMT usually applies when folks train Incentive Inventory Choices (ISOs), acknowledge a really massive capital acquire, or have a really excessive family earnings.

Planning Tip: In the event you thought you certified for ACA medical insurance premium tax credit and paid much less in your medical insurance all year long, however ended up making more cash than you acknowledged, you might have to repay these credit. If you wish to be extra conservative, you may forgo the tax credit all year long and have them paid to you through the tax return while you file (when you qualify).

Line 19: Baby Tax Credit score or Credit score for Different Dependents

Line 19 is the kid tax credit score.

Planning Tip: Pay particular consideration to the conditions the place a baby might be claimed. That is an space many individuals get incorrect. Take note of ages and phaseouts of the credit score.

Line 20: Quantity from Schedule 3, Line 8

Line 20 is the quantity from Schedule 3, which incorporates extra credit and funds, akin to:

Planning Tip: If you’re planning on shopping for an electrical car, see if a credit score is accessible. There are many limitations to who qualifies and which autos qualify.

Planning Tip: International shares usually produce international dividends, and a portion of it might be withheld within the issuer’s house nation for taxes. You possibly can usually get that cash again, so you aren’t being taxed on it twice (as soon as within the international nation and as soon as within the U.S.). In the event you paid international taxes as a result of investments held in your taxable brokerage account, be sure to account for them on Schedule 3. Your 1099 in your brokerage account ought to specify your international taxes paid, which you need to use to find out your international tax credit score.

Line 23: Different Taxes, Together with Self-Employment Tax

Line 23 consists of different taxes from Schedule 2.

Schedule 2 consists of the choice minimal tax (AMT), reimbursement of the superior premium well being care credit score, self employment taxes, internet funding earnings tax, Medicare payroll taxes for these with excessive incomes, 6% excise tax on extra IRA, Roth IRA, or HSA contributions, and the penalty for missed RMDs.

Planning Tip: The three.8% internet funding earnings tax might be deliberate round by managing your MAGI, akin to limiting capital beneficial properties in a excessive earnings 12 months, creating installment gross sales when promoting property, and donating appreciated property as an alternative of promoting investments with long-term capital beneficial properties.

Line 24: Whole Tax

Line 24 is the whole tax earlier than considering withholdings, estimated tax funds, or refundable credit.

The whole tax is a key determine for tax withholdings and estimated tax funds as a result of you may calculate a secure harbor quantity to guard your self from underpayment penalties.

You might face underpayment penalties when you don’t withhold sufficient taxes or make estimated tax funds that equal:

- 90% of the present 12 months’s whole tax (line 24), or

- 100% of the prior 12 months’s whole tax if prior 12 months AGI was underneath $150k or 110% of the prior 12 months’s whole tax if prior 12 months AGI was $150k or extra, or

- You owe lower than $1,000 in tax after subtracting your withholdings and credit.

Planning Tip: Withholding cash is mostly higher than making estimated tax funds as a result of cash might be withheld at any level all year long. For instance, you may make one massive withholding in December and nonetheless probably not face underpayment penalties. In the event you make estimated tax funds, they often must be paid in 4 equal installments. You typically can’t make a big estimated tax fee in December and keep away from underpayment penalties.

Planning Tip: When doing Roth conversions, it’s necessary to plan in your secure harbor quantity as a result of it’s typically higher to make estimated tax funds when you have money or brokerage property than withholding cash from the Roth conversion.

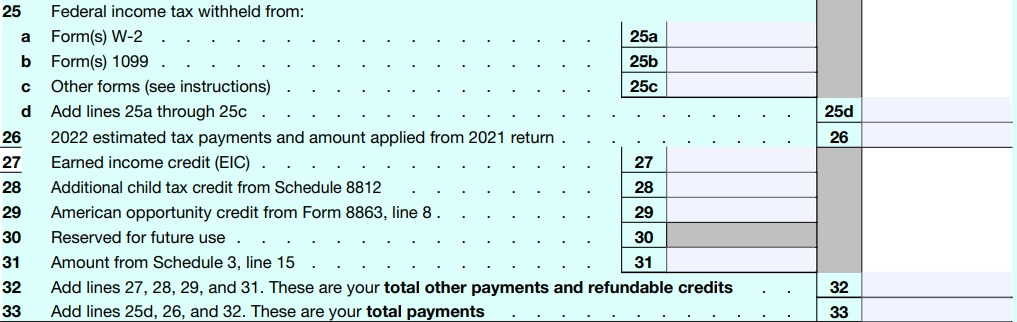

Traces 25 – 33: Funds

Traces 25 via 33 replicate the earnings tax withheld, estimated tax funds made, and different credit to subtract out of your whole tax to then decide how a lot you might be overpaid or the quantity you owe.

Line 25: Federal Earnings Tax Withheld

Line 25 captures the federal earnings tax withheld from W-2 jobs, 1099s and different sources.

Planning Tip: If you’re nonetheless working, you might wish to sometimes add up your estimated withholdings for the 12 months to find out if will probably be sufficient to cowl your whole tax. If not, you might wish to improve your withholdings to keep away from a shock while you file your tax return. Alternatively, if you’re withholding an excessive amount of, you might be giving the federal government an curiosity free mortgage and should wish to scale back your withholdings.

Line 26: Estimated Tax Funds and Quantity Utilized From Prior 12 months Return

Line 26 consists of the estimated tax funds you made, in addition to any overpayment you had utilized out of your prior 12 months tax return to this 12 months.

Planning Tip: As you make estimated tax funds via EFTPS or Direct Pay, I like to recommend printing a PDF of every tax fee and placing it right into a tax folder in your pc. It makes it straightforward to recollect how a lot you paid and when as you file your tax return.

Line 31: Quantity Type Schedule 3, Line 15

Line 31 consists of quantities from Schedule 3, that are international tax credit, certified plug-in motorized vehicle credit score, residential power credit, extra ACA healthcare alternate premium tax credit if the estimated earnings was too low, and others.

Planning Tip: In the event you retire earlier than Medicare and want to purchase medical insurance off of the healthcare alternate, it’s necessary to estimate your earnings, however when you underestimate, you’ll get these tax credit again when submitting your tax return.

Line 33: Whole Funds

Line 33 is the whole of strains 25d (tax withholdings), 26 (estimated tax funds and overpayments utilized to the present 12 months), and 32 (refundable credit).

Traces 34 – 36: Refund

In the event you paid in additional than you owe, you get a refund and may say what you need accomplished with it.

Line 34: Quantity You Overpaid

In the event you paid greater than your whole tax, line 34 is the quantity you might be overpaid (line 33 minus line 24)

Line 35: Quantity You Need Refunded to You

Line 35 is the quantity you had refunded to you.

Planning Tip: The quickest approach to get your tax refund is to have it electronically deposited. The IRS points greater than 9 out of ten refunds in lower than 21 days.

Line 36: Quantity of Line 34 You Need Utilized to Your Subsequent 12 months Estimated Tax

In the event you resolve to not have the complete refund deposited to your checking account, line 36 captures how a lot of your overpayment can be utilized to your subsequent 12 months’s estimated tax.

Having your overpayment utilized to the subsequent 12 months might be a straightforward approach to probably keep away from needing to make an estimated tax fee.

Traces 37 – 38: Quantity You Owe

In the event you didn’t pay greater than your whole tax, that is the place you’ll calculate how a lot you owe and the estimated tax penalty.

Line 37: Quantity You Owe

Line 37 the quantity you continue to owe (line 24 minus line 33).

Planning Tip: Assuming you comply with the secure harbor quantity and keep away from underpayment penalties, it’s okay when you owe the IRS cash while you file. You obtained an interest-free mortgage from the federal government. For instance, when you owe $10,000 at tax time, however you met the secure harbor necessities, you had an additional $10,000 over the previous 12 months that might have earned curiosity or been used to get pleasure from life.

Line 38: Estimated Tax Penalty

In the event you didn’t pay sufficient via withholdings or estimated tax funds, you might owe curiosity on the shortfall.

The curiosity is calculated on type 2210.

Planning Tip: In case your earnings fluctuates all year long and also you face underpayment penalties, you might be able to use the annualized earnings installment technique to cut back penalties.

Planning Tip: You possibly can see the quarterly rates of interest charged by the IRS to resolve how on prime of your estimated taxes you wish to be. Curiosity is compounded each day. Q1 of 2023, curiosity for underpayment penalties was 7%.

Frequent Tax Return Questions

Beneath are a number of tax return submitting questions folks ask.

How Lengthy Ought to I Hold My Tax Returns?

The IRS has totally different options about how lengthy to your tax returns and data relying on totally different conditions; nevertheless, a common rule of thumb is for 7 years.

Seven years covers most conditions, besides if you don’t file a return or when you file a fraudulent return.

Nonetheless, given how low-cost cloud storage and backup storage is, why not scan your recordsdata and hold them indefinitely?

Planning Tip: Create a folder in your machine referred to as “Taxes” and put a sub folder with the tax 12 months (i.e. 2023). As you obtain tax paperwork or have supporting paperwork (i.e. charitable receipts), obtain them into that folder or if they arrive through mail, scan them, and add them to that folder. Your data received’t take up bodily house, and also you don’t want to fret about how lengthy to maintain them.

Ought to I Take the Commonplace Deduction or Itemize?

Many individuals are confused about whether or not they need to take the usual deduction or itemize their deductions.

In case your itemized deductions usually are not larger than the usual deduction, you possible are taking the usual deduction.

Planning Tip: In the event you do a ballpark estimate of your itemized deductions, and it’s unlikely they’re larger than the usual deduction, don’t waste your time including all the things up. You possibly can merely take the usual deduction.

What are Frequent Tax Submitting Errors?

Many tax submitting errors are avoidable. It requires time to overview the return and catch errors earlier than submitting.

Beneath are a few of the tax submitting errors the IRS mentions on their web site.

- Submitting too early: when you file earlier than you’ve got your tax reporting paperwork, you might have to amend your tax return with the entire data

- Inaccurate data: double examine the numbers you or your accountant enter. It’s frequent to transpose numbers or kind within the incorrect numbers.

- Inaccurate or lacking Social Safety numbers: Don’t overlook to place the right SSN for every particular person.

- Misspelled names: The names ought to match Social Safety playing cards.

- Math errors: Whether or not you might be doing all your return by hand (I extremely discourage it!) or electronically, be sure to add, subtract, a number of, and divide appropriately.

You possibly can see the entire record of tax submitting errors the IRS mentions to keep away from.

Last Ideas – My Query for You

Many individuals don’t overview their tax returns.

Whether or not you personally put together it utilizing software program or depend on a CPA, spend 15 to half-hour reviewing your tax return and understanding how the numbers circulate via your tax return.

Use this text as a information to grasp how your earnings, tax planning methods, and investments have an effect on your taxes.

I’ll go away you with one query to behave on.

When will you overview your tax return?