{kind=link}

The Authorities (EPFO) has supplied a selection to pick eligible EPF/EPS subscribers to go for greater pension beneath EPS (Workers’ pension scheme).

An choice to earn a better pension throughout retirement.

Who would say “No” to such a proposal?

Properly, there isn’t a free lunch on this world. Whereas there may be an choice to earn greater pension, it comes at a value.

The query: Do you have to go for greater pension beneath EPS?

On this put up, let’s take a look at the next points intimately.

- How a lot pension do you get beneath EPS? When does the pension begin and the way lengthy do you get it?

- How do you contribute to EPF and EPS?

- What’s this complete concern about greater pension? And why does this come up?

- Who’s eligible?

- What do you get for those who go for greater pension? What do you lose?

- Should you go for greater pension, what portion of your EPF corpus can be moved to EPS?

- What are the issues/drawbacks of EPS? These drawbacks may affect your determination.

- Do you have to go for greater pension beneath EPS? Or must you keep on with the established order?

Mentioned this subject in a Twitter thread too.

How a lot pension do you get beneath EPS?

Month-to-month Pension = (Pensionable wage X Pensionable service)/70

Pensionable wage = Common of final 60 months of base wage (earlier it was once final 12 months wage). The pensionable wage is now capped at Rs 15,000. Nevertheless, there’s a approach for previous staff (who joined workforce earlier than September 1, 2014) to get round this cover and earn pension on precise base wage. And that is the supply of all the dispute that we are going to focus on on this put up.

Pensionable service = No. of years of contribution to EPS

I’ve learn in lots of locations that the pensionable service is capped at 35 years for the aim of pension calculation. Nevertheless, I couldn’t discover the supporting clause within the EPS Act. If such a cap is certainly there, it could movement from one other algorithm/laws.

The pension begins on the age of 58. Should you exit EPS on the age of 58 and have rendered greater than 20 years of pensionable service, 2 years can be added to the pensionable service for calculation of pension.

You will have an choice to start out pension early (however not earlier than the age of fifty). The pension can be diminished by 4% for yearly of early exit. May defer however not past the age of 60.

Let’s perceive this with the assistance of an illustration.

Your final 60 months’ common base wage is Rs 1 lac. And also you have been contributing as per precise wage (not as per wage cap of Rs 15,000)

You will have rendered 33 years of pensionable service. Since you will have labored for over 20 years and are exiting on the age of 58, your pensionable service can be 35 years.

Month-to-month pension = Rs 1 lac X 35/70 = Rs 50,000

- You’ll earn this pension of Rs 50,000 for all times.

- After you, your partner will earn 25,000 (50%) till he/she is alive.

- After your partner, your youngsters (most 2) will earn 25% pension every (Rs 12,500 every) till they flip 25.

- There are a number of different provisions caring for nook circumstances. You’ll have to verify the EPS Act to see how pension provisions will apply in such circumstances.

Be aware: Should you have been contributing with a wage ceiling, you’re going to get pension of solely Rs 15,000 X 35/70 = Rs 7,500.

Whenever you see such a formulation for calculating pension in an outlined profit scheme, you may sense this may be gamed. Such a formulation might have had some relevance within the years passed by however not now. Good that the Authorities has plugged the loophole, no less than for the brand new members.

By the way in which, how is the pension from EPS funded? It really works by means of your (your employer’s) contribution to EPS.

How does contribution to EPS and EPF work?

You contribute 12% of your base wage (Primary + DA) to EPF each month.

Your employer makes an identical contribution of 12%. Nevertheless, this 12% is invested in a special method.

Of this 8.33% goes in the direction of EPF (Worker pension scheme). And the rest (3.67%) goes to EPF.

Nevertheless, the wage on which EPS is calculated is capped at Rs 15,000 monthly.

Allow us to contemplate an instance. Allow us to say your base wage is Rs 50,000.

Your contribution to EPF = 12% * 50000 = Rs 6,000.

You don’t contribute to EPS.

Your employer additionally contributes Rs 6,000 to your EPS+EPF.

What’s the breakup?

Employer contribution to EPS = 8.33% X Rs 15,000 = Rs 1,250 (because the ceiling wage of Rs 15,000 will get triggered).

Employer contribution to EPF = Rs 6,000 – Rs 1,250 = Rs 4,750

The Authorities additionally contributes 1.16% of your base wage to EPS topic to a wage cap of Rs 15,000 monthly.

This sounds all proper. The place is the issue?

The place is the issue?

The wage ceiling has stored altering. Earlier than the modification within the EPS scheme in 2014, the ceiling was Rs 6,500.

Properly, that’s additionally nice. I don’t see any downside there.

Had the above wage ceilings concrete, all the pieces would have been nice.

Nevertheless, the EPS guidelines allowed staff to contribute over and above the wage ceiling cap. (Btw, the modification in EPS scheme in 2014 plugged this loophole and the workers becoming a member of the workforce after September 1, 2014 can’t contribute above the ceiling cap of Rs 15,000).

However this doesn’t stop staff who have been member of EPS scheme earlier than September 1, 2014 (and nonetheless are OR retired after September 1, 2014) from contributing above the wage ceiling (Rs 5,000/Rs 6,500/ Rs 15,000). And earn a HIGHER PENSION.

And this has led to all of the confusion.

Be aware that EPS is an outlined profit scheme (in contrast to NPS which is an outlined contribution)

How does this result in confusion?

There are a number of pathways.

Case 1

In some circumstances, your employer caps contribution to EPF to wage ceiling of Rs 15,000 (wage ceiling has stored altering. It was Rs 5,000 earlier. Then to Rs 6,500 and now to Rs 15,000).

Therefore, even when your fundamental wage is Rs 50,000, you’ll contribute solely Rs 1,800 (12% of Rs 15,000). Your employer will contribute 1,250 (8.33% of Rs 15,000) to EPS. And Rs 550 to EPF.

Should you belong right here, you aren’t eligible for HIGHER PENSION. Why? As a result of you will have been contributing solely as per the wage cap.

Case 2

Your employer doesn’t cap contribution. You contribute on precise wage (and never primarily based on wage cap). Precise base wage of Rs 50,000.

Your contribution to EPF = 12% X Rs 50,000 = Rs 6,000.

Your contribution to EPS is NIL.

Employer contribution to EPS = 8.33% X 50,000 = Rs 4,165

Employer contribution to EPF = 3.67% X 50,000 = Rs 1,835

You might be eligible for greater pension.

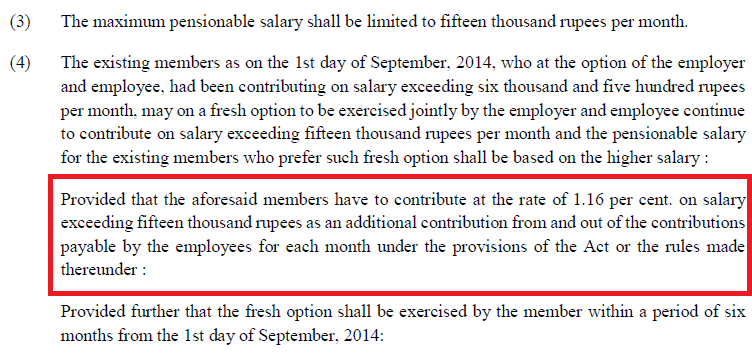

Nevertheless, there was a technical rule right here the place the worker and employer needed to convey this determination to EPFO inside sure timelines. Provision to Para 11(3) of the scheme earlier than modification in 2014. I reproduce the availability under.

Therefore, there have been situations the place folks had contributed extra to EPS with out explicitly stating this selection.

Once they reached out to EPFO for greater pension, EPFO rejected their declare for greater pension (and gave pension as per the ceiling cap) since these staff didn’t specify this selection explicitly with acknowledged timelines. And refunded extra contribution within the EPS to the EPF accounts of the workers with curiosity.

Such staff challenged EPFO within the courts and received. The Supreme Court docket discovered these timelines arbitrary and dominated in favour of such staff. Eligible for greater pension. You’ll be able to examine this case about Mr. Praveen Kohli right here.

Case 3

Your employer doesn’t cap contribution. You contribute on precise wage (and never primarily based on wage cap). Precise base wage of Rs 50,000.

Your contribution to EPF = 12% X Rs 50,000 = Rs 6,000.

Your contribution to EPS is NIL.

Employer contribution to EPS = 8.33% X 15,000 = Rs 1,250 (whereas the employer doesn’t cap contribution to EPF, it caps the EPS contribution)

Employer contribution to EPF = 6,000 – Rs 1,250 = Rs 4,750

Because the EPS contribution has been made as per the wage cap of Rs 15,000, you’ll get pension solely as per the wage cap. Not greater pension.

Should you belong right here, this current EPFO round dated Feb 20, 2023 will curiosity you.

Why?

As a result of you will have an choice to replenish a type and make sure that you really want a better pension now. Since there may be free lunch, EPFO will switch a portion of cash (deficit contribution to EPS together with curiosity from EPF to EPS). To your future contributions additionally, you (your employer) must contribute extra to EPS.

So, greater pension however a decrease EPF corpus. Within the latter a part of the put up, we are going to see learn how to consider these decisions.

Who’s eligible for greater pension beneath EPS?

I reproduce an extract from EPFO round dated February 20, 2023.

The round refers to eligibility for exercising this new choice for greater pension by filling up a type.

- You will need to have been a member of EPS as on September 1, 2014. Due to this fact, for those who began working after September 1, 2014, you’re NOT eligible. OR for those who retired earlier than September 1, 2014, you’re NOT eligible for greater pension.

- Your (and your employer’s) contribution to EPF (as on September 1, 2014) was on the wage that exceeded the wage ceiling cap of Rs 5,000 or Rs 6,500. Let’s say your base wage was 25,000 and also you have been contributing on the precise wage of Rs 25,000 (and never as per wage cap of Rs 15,000). You might be ELIGIBLE even when your EPS contribution was capped however your EPF contribution was on precise wage.

Easy methods to apply for Increased Pension beneath EPS?

The EPFO round lays down the tactic.

You will need to make a joint software alongside together with your employer to EPF. As issues stand right now, you need to apply earlier than March 3, 2023 (4 months from the Supreme courtroom judgement).

Given the confusion surrounding this matter, I hope the deadline is prolonged.

Recommend you attain out to the accounts workforce of your employer for the operational particulars.

Do you have to go for Increased pension beneath EPS?

Should you go for Increased pension, you’re going to get greater pension. Threat-free. Assured for all times. And that’s the largest benefit.

How excessive a pension will you get?

Properly, that is dependent upon your common base wage within the remaining 5 years of your work life (and years of pensionable service).

Now, you can not reply this query precisely, particularly if you’re within the non-public sector the place salaries can fluctuate drastically. In case you are working with a PSU and are nearer to retirement, you will have a firmer grip on the reply.

Nonetheless, take educated guesses. How a lot increment you will have been receiving the previous few years? And with these assumptions, you may arrive on the remaining pension quantity.

And also you examine that towards the alternate options? Don’t you?

Firstly, the upper pension comes at a value. Your EPF corpus will go down as a good portion of your EPF corpus can be shifted to EPS scheme. Your future contribution to EPF can even fall since you’ll now contribute extra to EPF.

After retirement, you’ll get this corpus and you may make investments this cash in financial institution mounted deposits, Authorities Bonds, SCSS, PMVVY and even annuity plans to generate common retirement earnings.

So, you need to see, how a lot EPF corpus are you foregoing? And the way straightforward or troublesome it’s so that you can generate the same stage of earnings utilizing this corpus? If you are able to do that simply, then preserve the established order. Should you can not (the speed of return can be fairly excessive), then go for a better pension.

Should you go for Increased pension, what portion of EPF can be shifted to EPS?

Within the aforementioned EPFO round dated Feb 20, 2023, EPFO has talked about, “The tactic of deposit and that of computation of pension will comply with by means of subsequent round”.

Deposit means deposit from EPF to EPS. To be sincere, it’s unfair to count on staff to select till EPF comes out with these calculations. Keep in mind, the Supreme courtroom handed its judgement on November 3, 2022, and gave 4 months (till March 3, 2023) to members (staff) to make their selection. And EPFO says on Feb 20, 2023, that they may concern a subsequent round for calculations.

Let’s do some crude calculations and see how a lot can be moved out of your EPS corpus.

Let’s say you began working within the yr 2001.

Your base wage firstly was Rs 20,000 and grew at 5% every year. I’ve assumed that EPF returned 8.5% p.a. all through the tenure.

The wage cap was Rs 6,500 till September 2014 and Rs 15,000 thereafter.

Whilst you have been contributing to EPF on precise wage, the contribution to EPS was solely as per cap.

Within the first yr, Base wage =20,000

Worker EPF contribution = 20,000 * 12% = Rs 2,400

Employer EPS contribution = 8.33% * 6,500 = Rs 542 (if this have been on precise wage, employer would have invested Rs 1,667)

Employer EPF contribution = Rs 2,400 – Rs 542 = Rs 1,858 (if EPS contribution have been on precise wage, this may have been Rs 2,400 – Rs 1,667 = Rs 733

The deficit contribution to EPS = Rs 1,667 – Rs 542 = Rs 1,125

Now, this deficit contribution to EPS (that went to EPF) must be shifted again to the EPS scheme. And the curiosity on this deficit contribution too. And this should be completed in your whole previous service.

How a lot will this quantity be?

This can depend upon the trajectory of your wage development. The upper your wage, the upper the deficit contribution. And the extra (in share phrases) you’ll have to switch from EPF to EPS.

Share of switch= Complete deficit contribution to EPS/Complete Contribution to EPF

On this instance, whole contribution to EPF (contains each employer and worker) = Rs 21.63 lacs

Complete deficit contribution to EPS = Rs 6.06 lacs

Share of EPF to be transferred to EPS = Rs 6.06/21.63 lacs = 28%

You can even examine the EPF corpus. Present vs the EPF corpus you’ll have with out EPS contribution being capped. You’d get the identical reply.

I did very crude EPF calculations (not actual). Present corpus = ~51.66 lacs

EPF corpus after eradicating EPS cap = Rs 37.14 lacs. A distinction of 28%.

Be aware this distinction could be greater for a better base wage.

On this instance, if we alter the beginning base wage from Rs 20,000 to Rs 50,000, the switch share rises to 32%.

If beginning base wage drops to Rs 10,000, the switch share falls to 19.8%.

And that’s not it

Should you go for greater pension, your employer’s future contribution to EPS will rise and to EPF will fall. That can even decelerate the expansion of EPF corpus.

Extending the instance to pending 10 years of service, for those who go for greater pension, you’ll finish with Rs 1.04 crores of EPF corpus after 10 years.

Had you caught with decrease pension, you’ll have Rs 1.46 crores.

What would be the pension?

Common base wage within the final 5 years = Rs 86,645

Month-to-month pension = 86,645 X 35/70 = Rs 45,798

Even for those who caught with decrease pension choice (established order), you’ll get pension of Rs 7,500 (Rs 15,000 X 35/70).

Distinction of Rs 41.68 lacs in EPF corpus.

Distinction in EPS pension = Rs 45,798 – Rs 7,500 = Rs 38,298

Now, for this Rs 41.68 lacs to generate earnings of Rs 38,298 monthly, it must generate a return of 11% p.a. That’s not straightforward.

Taking a look at such an evaluation, choosing greater pension appears to be like like a more sensible choice.

However EPS has its personal set of issues.

What are the issues with pension beneath EPS?

Firstly, you get the total pension till you’re alive. After you (the first pensioner passes away) your partner will get the pension however solely 50% of the unique quantity. And after the partner passes away, a most of two youngsters will get 25% every till they’re 25.

I’m imagining a morbid situation, however the household doesn’t get as a lot for those who (the first pensioner) move away too quickly after retirement.

Had you caught with a decrease pension, you’ll have gotten a a lot greater EPF corpus at retirement. Now, this EPF corpus belongs to you. And after you, it belongs to your loved ones. So, this extra EPF corpus might not have the ability to generate as excessive earnings as EPS however this EPF corpus belongs to you and your loved ones.

Secondly, the pension is dependent upon the final 5 years (60 months) of base wage. So, for those who resolve to take a step off the accelerator when you cross 50 and decide up a job that pays much less, your common earnings in the course of the remaining 5 years of your working life might fall. And therefore the pension can be decrease.

As an example, allow us to assume your common base wage between the age of 48 and 53 was Rs 2 lacs. And the common base wage between 53 and 58 years was 1 lac. The pension could be calculated for the common wage within the final 5 years i.e. Rs 1 lac. That you’re incomes extra earlier than that doesn’t matter.

Thirdly, if you wish to retire early, then your pensionable years of service can be much less, and the pension will accordingly be decrease. Plus, the pension quantity doesn’t begin earlier than the age of fifty. Allow us to contemplate an instance. You began working on the age of 25 and labored till the age of 45. 20 years of service. Let’s additional assume that your common wage within the final 5 years was Rs 1 lac. Therefore, your month-to-month pension could be Rs 1 lac X 20/ 35 = Rs 57,142.

Nevertheless, in order for you this full pension, you’ll have to wait till the age of 58. However you retired on the age of 45. There may be an choice to start out drawing earlier however not earlier than you flip 50. The early withdrawal comes at a value. You get 4% much less for every year of early withdrawal. So, for those who begin at 50, you’re going to get 8 X 4% = 32% much less. Rs 38,857 as an alternative of Rs 57,142.

Lastly (and I’m not certain about this), the choice for a better pension is a joint choice exercised by you and your employer. You might be in a non-public job and have opted for a better pension (and your current employer is comfortable with this). You turn your job after a number of years and the brand new employer has a special coverage about contributions. Caps the contribution as per wage ceiling. You’ll be able to ask them to make an exception for you, however it is a headache. This chance would make me extraordinarily uncomfortable.

Be aware: The most recent EPS guidelines additionally present for workers to contribute 1.16% of Primary wage (for the portion exceeding Rs 15,000) to EPF in the event that they wish to obtain a better pension.

In the intervening time, the Supreme Court docket has put this on maintain. For extra on this, confer with web page 7 of this doc. Since this pertains to funding of EPS pool, you may count on this to return to you in some type or the opposite later.

What’s the remaining verdict?

There isn’t a one-size-fits-all answer.

Going by numbers (and as now we have seen above), choosing the upper pension will certainly provide you with a really excessive pension. It might be troublesome to duplicate the identical stage of risk-free earnings out of your EPF corpus.

Nevertheless, the upper pension comes with many ifs and buts. Many caveats. You lose flexibility.

You will need to weigh the upper pension towards these issues in EPS.

I get extraordinarily uncomfortable for those who take away flexibility from my investments. Therefore, please respect my biases in my remaining feedback.

In case you are nearer to retirement and are comfortable with all of the caveats (as talked about within the earlier part), you’ll seemingly be higher off by signing up for Increased pension. However verify the calculations earlier than taking a remaining name.

In case you are youthful (35-40), connect better weight to issues/caveats/lack of flexibility in EPS.

Disclaimer: Whereas I’ve tried my greatest to grasp and clarify the subject intimately, there could also be shortcomings in my evaluation or my understanding of the EPS scheme and the EPFO round.

Supply/Extra Hyperlinks