{kind=link}

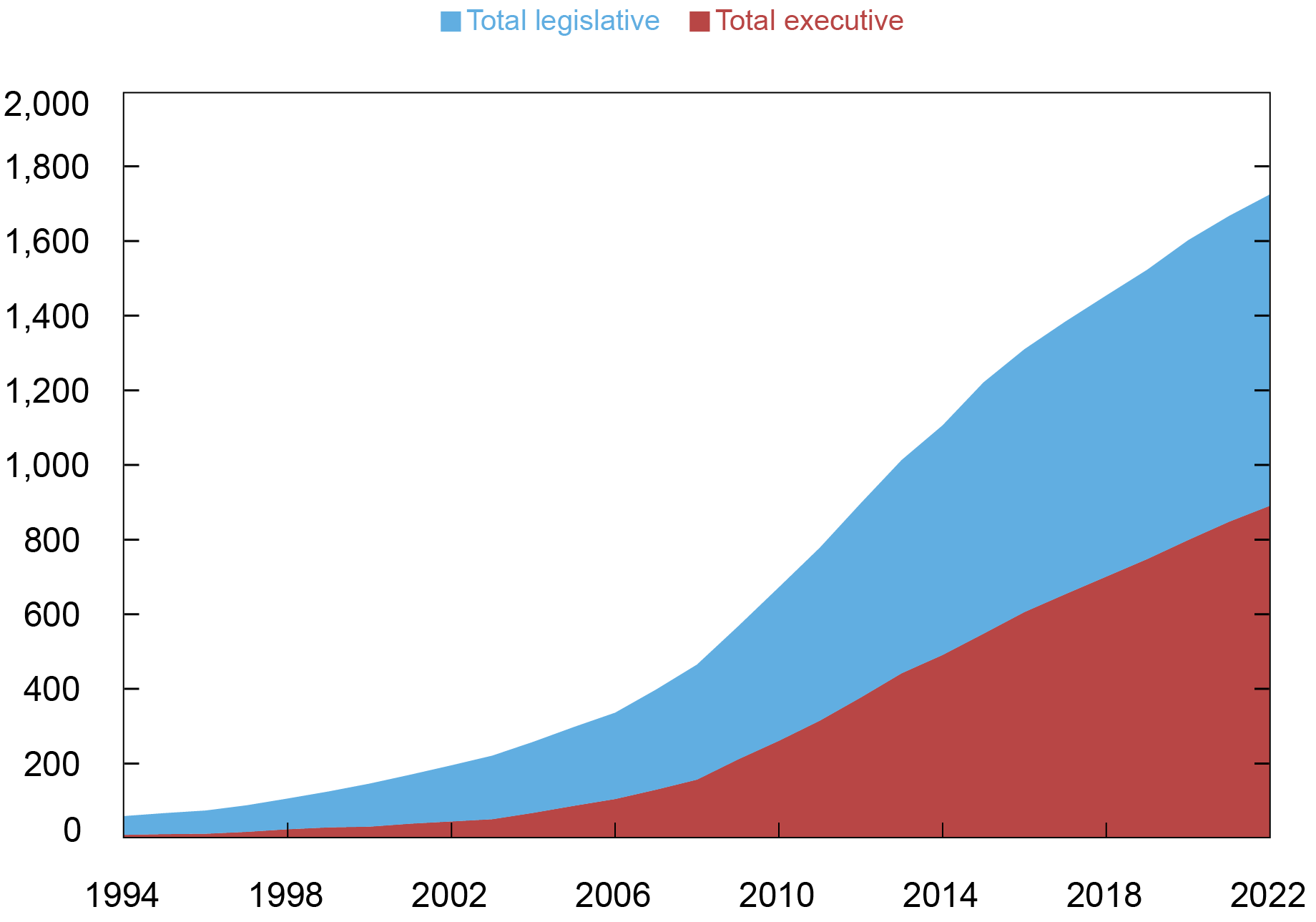

A rising variety of climate-related insurance policies have been adopted globally up to now thirty years (see chart under). The chance to financial exercise from modifications in insurance policies in response to local weather dangers, akin to carbon taxes and inexperienced subsidies, is also known as transition danger. Transition danger can adversely have an effect on the true economic system by means of the banking sector. For instance, a shock to debtors’ transition danger can impair their means to repay, which might then result in an amplified impact on banks’ present and anticipated future earnings, leading to a systemic undercapitalization of banks. In a current Workers Report co-authored with Robert Engle and Richard Berner, we look at whether or not banks are sufficiently capitalized to soak up losses throughout traumatic circumstances resulting from heightened local weather (transition) danger.

The Cumulative Variety of Local weather-Associated Insurance policies throughout the World

Notice: “Insurance policies” covers climate-related legal guidelines, in addition to rules selling low carbon transitions.

Challenges to Assessing the Local weather Threat to the Monetary System

Regardless of the widespread adoption of local weather insurance policies and the significance of understanding their impact on the banking sector, there was little understanding of the potential affect of local weather change on the monetary system resulting from a number of challenges, as identified by Bolton et al. (2020). For instance, whereas the literature on systemic danger measurement (for instance, Brownlees and Engle, 2017; Acharya et al., 2016; Adrian and Brunnermeier, 2016; Allen et al., 2012) has supplied helpful indices of systemic misery within the context of economic crises, no such measures exist to investigate climate-related dangers.

One of many key challenges to measuring the local weather danger of economic establishments is that analyses primarily based on previous local weather occasions could not successfully seize modifications within the notion of danger. Market expectations could change with no direct expertise of local weather change occasions, and asset costs right now can replicate modifications in future local weather danger despite the fact that the damages or impacts are a long time away. Secondly, each the perceived local weather danger and the way corporations, banks, and markets reply to it change over time. Lastly, the dearth of dependable knowledge sources poses a big problem. Though voluntary climate-related disclosures exist, they typically undergo from incompleteness and inconsistencies in high quality.

We develop a market-based methodology that addresses these challenges. We deal with the primary problem by developing local weather danger elements primarily based on portfolios designed to say no in worth because the transition danger rises, and by measuring the banks’ inventory return sensitivity, referred to as the local weather beta, to the local weather danger issue. We take care of the second problem by estimating the local weather beta dynamically, which permits for time-variation within the responses of corporations and buyers to modifications within the transition danger. Lastly, we confront the information hole problem as we solely use market knowledge which might be constant in high quality, comparable throughout corporations, and fewer inclined to the noise and bias inherent in voluntary local weather disclosures.

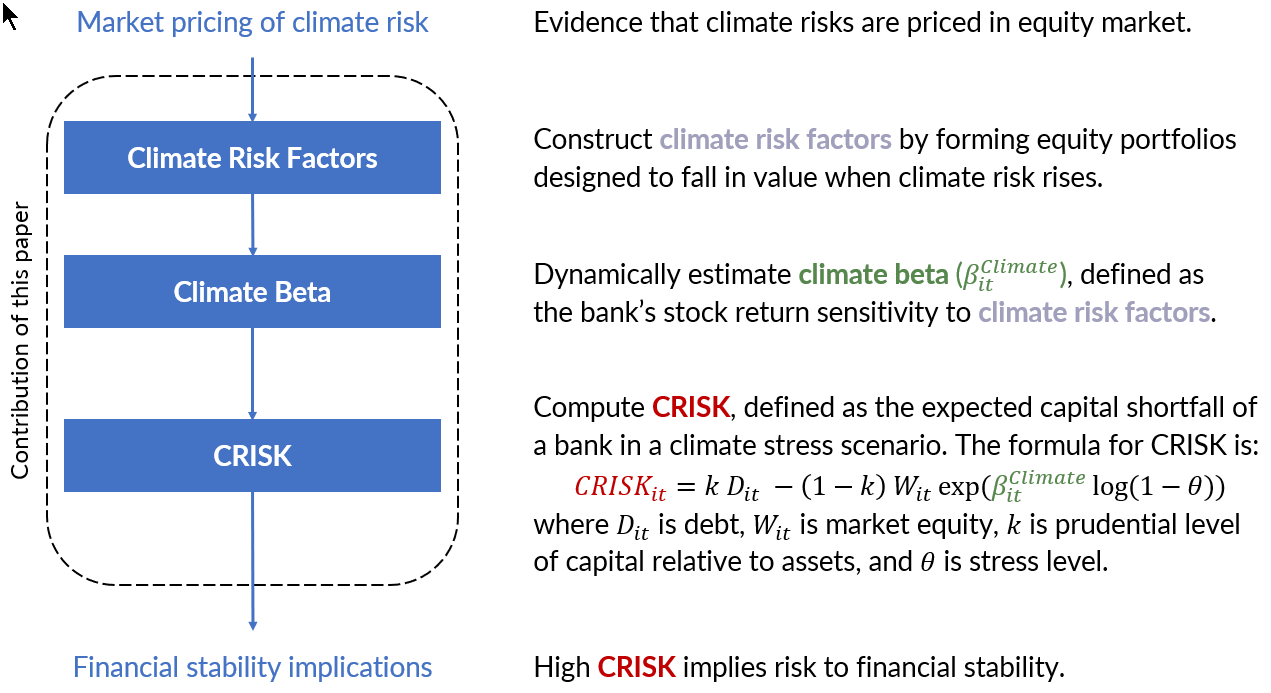

CRISK: A New Measure of Local weather Threat

We develop a novel measure, CRISK, outlined because the banks’ anticipated capital shortfall conditional on local weather stress. The capital shortfall is taken because the capital reserves the monetary agency wants to carry to satisfy prudential capital necessities. CRISK is a operate of a given monetary agency’s dimension, leverage, and the anticipated fairness loss conditional on local weather stress. As proven within the chart under, the latter is computed utilizing the estimated local weather beta and an assumption concerning the extent of local weather stress. To contemplate a sufficiently extreme but believable stress state of affairs, we take the bottom one percentile of the six-month return distribution of the local weather danger issue to calibrate the stress degree.

CRISK Estimation Steps

Local weather Threat Publicity of World Banks

We apply our methodology to estimate local weather betas of enormous international banks. The local weather beta and CRISK estimates differ relying on local weather danger elements in addition to the severity of the state of affairs. Right here, we summarize our findings primarily based on the state of affairs primarily based on returns of the stranded asset issue (developed by Litterman) which serves as a proxy for market expectations on future transition danger arising from fossil gas vitality corporations’ belongings changing into “stranded” alongside most transition paths.

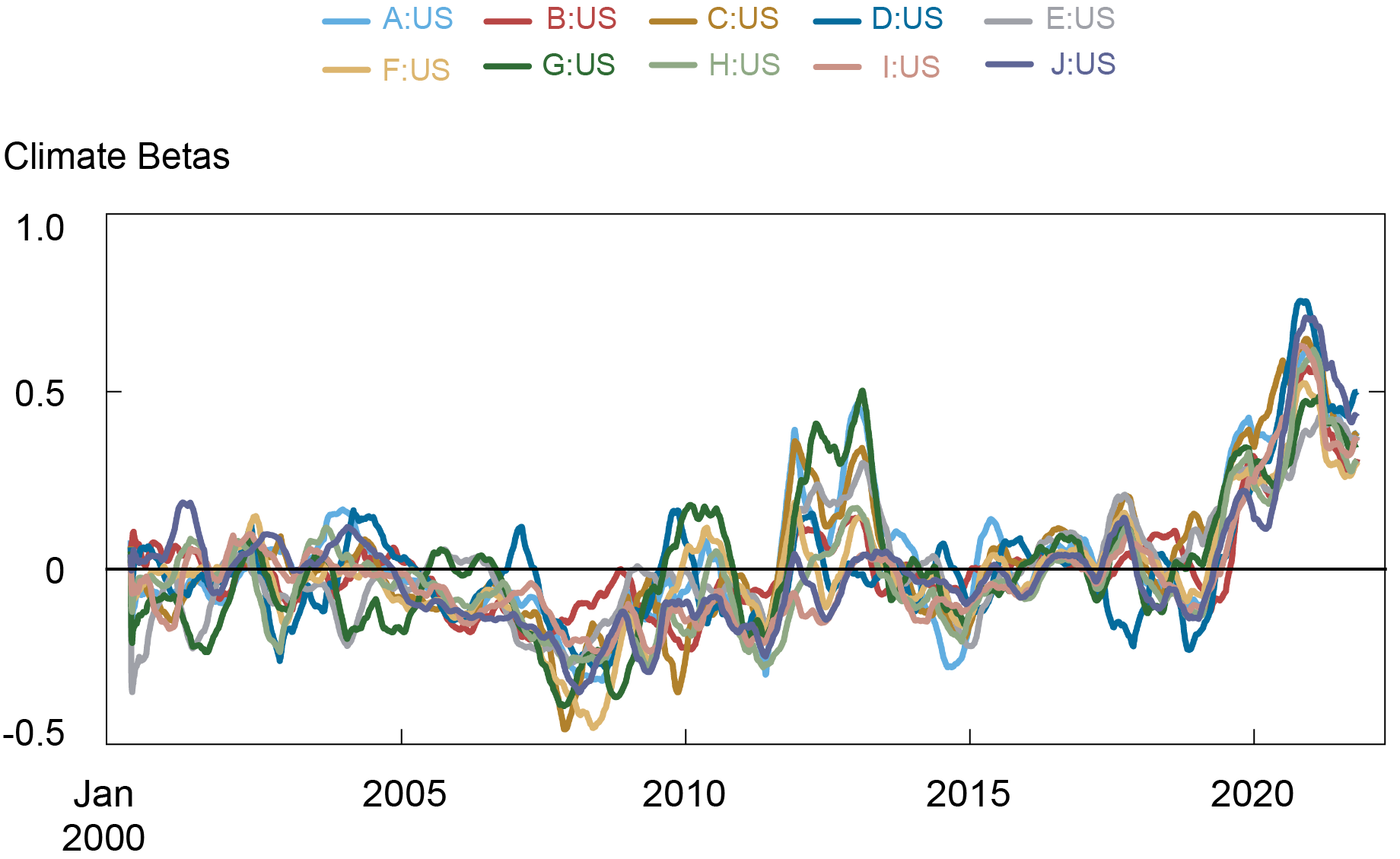

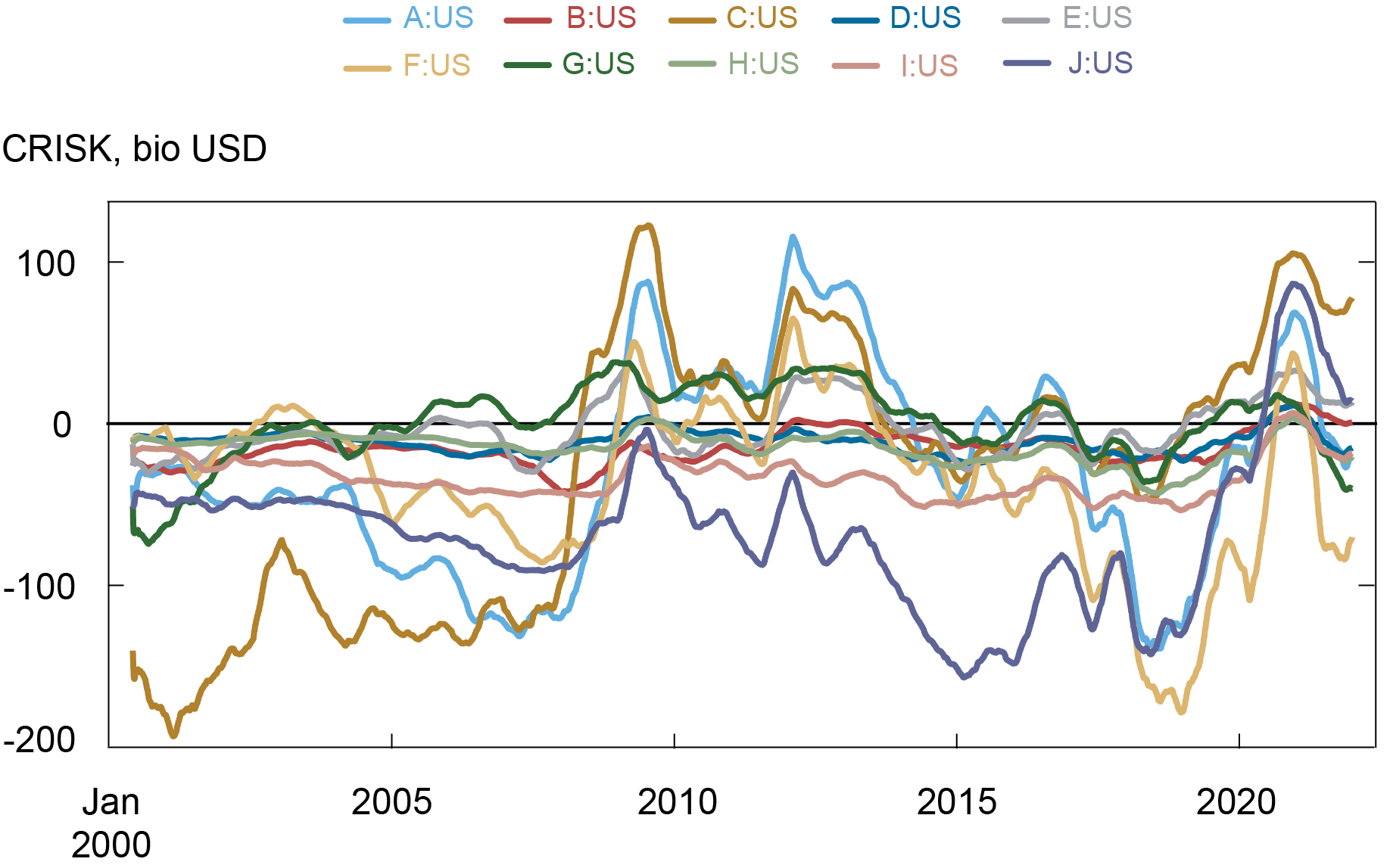

We discover that the local weather beta varies over time as proven within the first chart under, highlighting the significance of our dynamic estimation. The local weather beta and CRISK (as proven the second chart under) considerably elevated throughout 2020, throughout all banks in our pattern. In 2020, the mixture CRISK of the highest 4 U.S. banks elevated by 425 billion U.S. {dollars} (USD), which corresponds to roughly 47 % of their market capitalization. Our decomposition evaluation reveals that 40 % of the CRISK enhance in 2020 was resulting from a rise in local weather betas, and 40 % was resulting from a lower in fairness values. In our paper, we present that the local weather beta captures the consequences of transition danger and never the concurrent COVID outbreak.

Our outcomes might be interpreted as follows. When fossil gas vitality costs plummeted in 2020, which might occur beneath a sudden and disorderly transition, “brown” debtors’ loans grew to become significantly riskier, and the banks’ inventory returns grew to become extra delicate to the transition danger, thereby growing banks’ local weather danger publicity. Certainly, we discover proof supporting this mechanism from the validation train within the paper.

Local weather Beta of U.S. Banks

Notes: The pattern banks are the highest 10 largest U.S. banks by common complete belongings in 2019. The pattern interval is from June 2000 to December 2021.

CRISK of U.S. Banks

Notes: The pattern banks are the highest 10 largest U.S. banks by common complete belongings in 2019. The pattern interval is from June 2000 to December 2021.

Versatility of the CRISK Framework

Our framework is flexible as it may be utilized to monetary establishments apart from banks and might be aggregated on the economic system degree. As an illustration, within the paper we compute the mixture CRISK of 105 monetary corporations, together with banks, broker-dealers, and insurance coverage corporations, within the U.S. to gauge the system-wide measure of local weather danger. Furthermore, our framework also can admit all kinds of local weather stress situations. Within the paper, we contemplate a much less excessive state of affairs by taking 5 % quantile as an alternative of 1 % quantile of returns of the local weather danger issue. We additionally contemplate different elements that may be related to varied stylized variations of transition state of affairs (for instance, carbon tax, a mix of a carbon tax and inexperienced subsidy).

Last Phrases

Local weather transition danger, by impairing debtors’ means to repay, can cut back present and anticipated future earnings within the banking sector. The consequences of such dangers on banks’ capitalization might end in detrimental externalities on the true economic system, akin to a lower in credit score provide and financial development. We offer a market-based methodology to measure the potential impact of transition danger on banks’ capitalization. Our new measure of systemic local weather danger, or CRISK, can complement different fashions, situations, and measures to help each non-public and public sectors.

Hyeyoon Jung is a monetary analysis economist in Local weather Threat Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

How one can cite this put up:

Hyeyoon Jung, “CRISK: Measuring the Local weather Threat Publicity of the Monetary System,” Federal Reserve Financial institution of New York Liberty Road Economics, April 20, 2023, https://libertystreeteconomics.newyorkfed.org/2023/04/crisk-measuring-the-climate-risk-exposure-of-the-financial-system/.

Disclaimer

The views expressed on this put up are these of the writer(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the writer(s).