Snippet from a Dialogue:

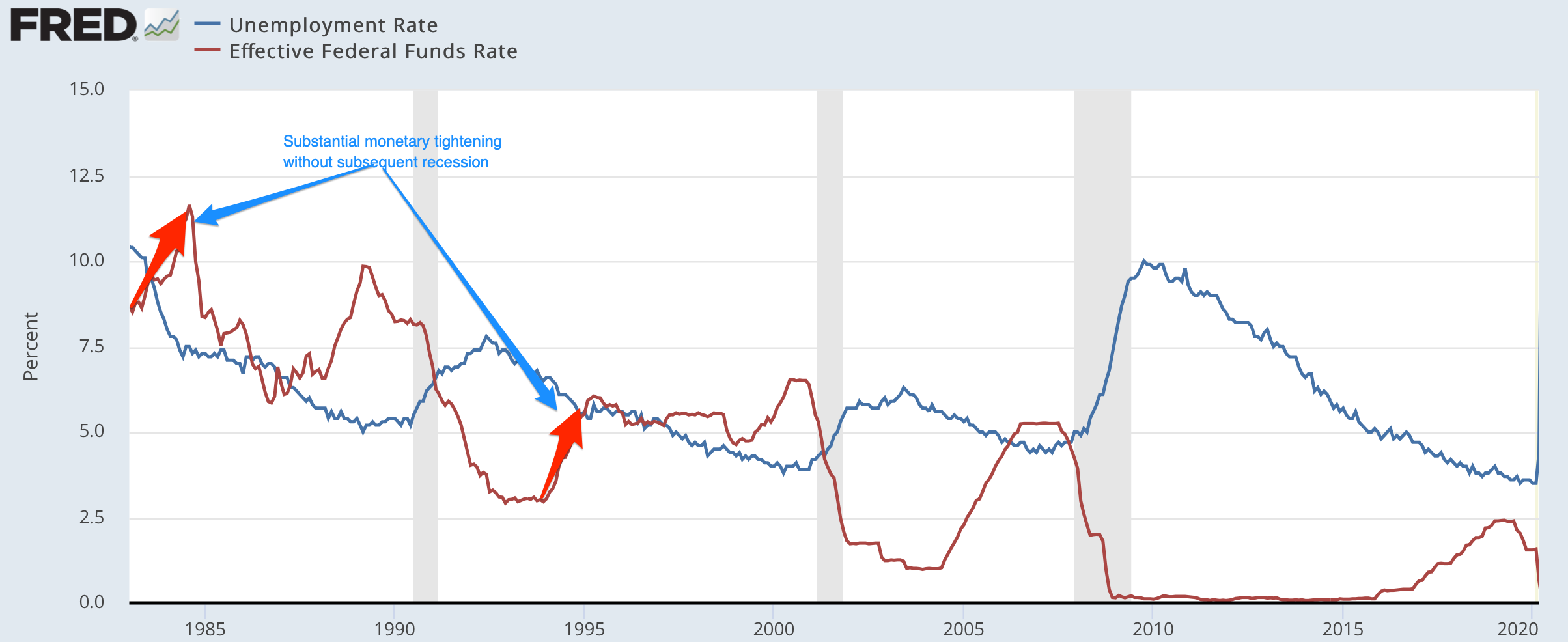

Axiothea: The hole between the labor-force participation price for prime-age employees and the unemployment price remains to be giant—as giant because it was in 2014. That implies to me that our first take must be that, aside from rate-of-change results, the labor market now’s about as tight because it was in 2014.

Kephalos: That the “labor scarcity” crowd thinks that the unemployment price features a bunch of people who find themselves actually out-of-the-labor-force is one thing I discover considerably disturbing. Or do they not know that unemployment remains to be elevated?

Glaukon: The job-openings sequence hit a rare file excessive on the finish of March: over 8 million. I recommend that helps reply among the questions. It actually wouldn’t be straightforward to fill that many slots shortly, it doesn’t matter what degree of advantages individuals are receiving (or certainly, how shortly employers enhance wages).

One Video

polyMATHY: Romanes Eunt Domus EXPLAINED:

Paragraphs:

Sure, there’s a substantial quantity of craziness within the froth across the “struggle structural racism” motion. No: I don’t suppose it’s terribly vital. Any additional questions?

John Ganz: “That’s Not A Character, Sweetie”: ‘Tema Okun’s anti-racism coaching supplies… with a barely completely different emphasis… sound like…white nationalis[m]…. They recommend solely “white supremacy tradition” inculcates fastidiousness, precision and a priority with logic and objectivity… white supremacist propaganda that connects “civilization” essentially with whiteness…

LINK: <https://johnganz.substack.com/p/thats-not-a-personality-sweetie>

When Tim Duy left the open web, the general public sphere took a giant loss:

Tim Duy: Fed Watch 2021–05–10: ’It strains credibility to argue that the improved unemployment advantages don’t disincentive job search efforts. That mentioned, I worry unemployment advantages obtain outsized consideration…. Monetary assist from tax rebates, ongoing pandemic fears, lack of entry to childcare and colleges, and retirements. Collectively, these components level towards a reasonably sluggish restoration of the labor provide…. There’s additionally the elemental problem that firing occurs extra shortly than hiring…. A degree shift up in wages and costs doesn’t by itself equate to a change within the underlying dynamic that may perpetuate into persistently increased inflation. We almost certainly is not going to have a lot sense of the persistence of inflation till the identified base and reopening results cross. Meaning the Fed is not going to need to validate any strikes by market contributors to tug price hikes ahead once more on the idea of near-term inflation numbers…

I do suppose that fear about elevating taxes must be postponed till rates of interest have semi-normalized. However, in any other case, that is very clever certainly:

Barry Eichengreen: Will the Productiveness Revolution Be Postponed?: ‘The 1918–20 influenza… got here on the heels of advances… the meeting line… the superheterodyne receiver… Radio Company of America, the main high-tech firm… chemical processes… lowered fertilizer prices…. However… the complete affect was felt solely within the Nineteen Thirties. Companies used downtime through the Nice Melancholy to reorganize manufacturing, and people least able to doing so exited…. Authorities invested in roads, permitting the nascent trucking business to spice up productiveness in distribution. However greater than a decade first needed to cross…. This prolonged delay suggests two vital classes. First, some lag is probably going…. Second, authorities can take steps to make sure that the acceleration commences sooner somewhat than later…. It could be counterproductive, clearly, to curtail infrastructure spending… or spending on early childhood training…. However the extra involved you might be a couple of delay earlier than quicker productiveness progress materializes, the extra strenuously you must insist that Biden’s spending plans be financed with taxes so as to avert the overheating situation…

“Neoconservatism” targeted on the Chilly Battle and the “conventional household”—with greater than a soupçon of racism connected. “Neoliberalism” targeted on financial construction and incentives. They weren’t, actually, allied, besides at moments of comfort. This isn’t to say that individuals might be each. However additionally it is price noting that “neoconservatism” was a powerful response towards Nixon-Kissinger-Ford international coverage:

Adam Tooze: Chartbook E-newsletter #19: ‘In 1971 Congress handed the Complete Baby Improvement Invoice…. As Walter Mondale remarked on the time: “the American individuals should understand that there isn’t a reply to the unfairness of American life that doesn’t embody a large preschool complete youngster growth program. Something lower than that’s an official admission by this nation that we don’t care.” Even though the Invoice was handed with bipartisan assist by each the Home and the Senate, it was vetoed by Richard Nixon. Within the clarification for his veto he warned that public youngster care would weaken the household and import to the US the practices of the Soviet Union…. The alliance between neoliberalism and neoconservatism… linking a protection of a restored “conventional” household to a reassertion of the market order and an overturning of the New Deal compromise on welfare…

LINK: <https://adamtooze.substack.com/p/chartbook-newsletter-19>

Longer:

Furman and Powell are speaking sense, each in regards to the present state of affairs and in regards to the uncertainties:

Jason Furman & Wilson Powell: The US Labor Market Is Operating Sizzling… or Not?: ‘America added 266,000 jobs in April whereas the unemployment price rose barely to six.1 p.c with the practical unemployment price, which adjusts for misclassification and the bizarre decline in labor drive participation, falling to 7.6 p.c… nonetheless 10 million jobs in need of its pre-pandemic development in April with the employment price down 3.2 proportion factors since February 2020….

The labor market has nonetheless been behaving as if there was comparatively little and even no slack left: Openings had been at file ranges, quits had been close to file ranges in February, composition-adjusted wages had been rising on the similar tempo they did within the comparatively tight 2019 labor market with the biggest wage features for the lowest-wage employees, wages not adjusted for altering composition rose 0.7 p.c in April, and common weekly hours stay very excessive…. With so many conflicting indicators because the labor market adjustments quickly with demand and provide returning to completely different levels in numerous sectors, it’s laborious to make a assured evaluation….

The labor market has a methods to go earlier than it’s healed. The query is what type this adjustment will take and what the dangers are…. Wanting ahead there are good causes to anticipate giant will increase in each demand for labor and provide of labor…. One draw back situation is overheating…. A second draw back situation is an incomplete jobs restoration…. The third draw back situation is that the virus itself takes a flip for the more serious… The almost certainly end result stands out as the Goldilocks situation. On this situation each demand and provide return. Patches of mismatch in timing and sectors would result in noticeable shortages and value and wage will increase in some areas, particularly over the spring and summer season as excessive demand is briefly unable to totally be happy by out there labor. Nevertheless, these mismatches work themselves out with solely transitory will increase within the degree of costs and no persistent adjustments in inflation or inflation expectations.…

LINK: <https://www.piie.com/blogs/realtime-economic-issues-watch/us-labor-market-running-hotor-not>

Hoisted from the Archives:

Once I first noticed the Solow progress mannequin in one among my first economics courses, I raised my hand, and I requested: Why is it assumed that gross financial savings is a continuing share of gross revenue—that’s, revenue plus depreciation. Isn’t that the identical as assuming that individuals are too silly to calculate deprecation? Shouldn’t the fitting assumption be that web financial savings is a continuing share of webrevenue?

The trainer then filibustered.

I finally requested Bob Solow this query. He mentioned—precisely—that in his authentic paper it had certainly been web financial savings and web output (Cf. Solow (1956): A Contribution to the Idea of Financial Development <http://piketty.pse.ens.fr/information/Solow1956.pdf>, wherein there isn’t a deprecation—the important thing parameters are “the financial savings price, the capital-output ratio, the speed of improve of the labor drive). When requested why he had shifted to gross financial savings as a relentless share of gross revenue, he shrugged his shoulders and mentioned ”referees”.

Certainly.

Until you assume that individuals can’t calculate depreciation, the primary optimizing mannequin for a consultant agent one would naturally write down has web financial savings a share of web revenue, with the share relying on anticipated actual threat and return.

I’ve all the time taken it to be an indication of the low high quality of a lot of the criticism of Thomas Piketty’s Capital within the twenty first Century that professors declare Piketty’s assumption that web financial savings is a continuing share of web revenue is a gotcha—is (a) some form of an analytical mistake, as a result of it implies an ever-growing share of depreciation in gross output in a world the place the financial progress price of the economic system n+g = 0 is zero; and (b) that it’s a massively consequential mistake. IMHO, you may solely keep it’s consequential for those who lack familiarity with the NIPA, and its depreciation charges—if the “illustrative” deprecation price you retain in 12 months head is 10% of income-earning wealth a 12 months, and so suppose that within the U.S. as we speak annual deprecation allowances are extra like $12 trillion/12 months (60% of GDP, 12% of the income-earning wealth inventory) than like $4 trillion/12 months (15% of GDP; 4% of the income-earning wealth inventory).

This, seven years in the past, actually didn’t go properly in any respect.

You woulda thunk that individuals wouldn’t double down after it was identified to them that (a) removed from being basic and canonical, depreciation was not even within the Solow (1956) that’s cited ten occasions a day, and (b) that one thing is badly improper along with your pondering if the numbers you might have in your head say that depreciation—capital consumption allowances—are 60% of U.S. GDP. However no! Removed from it!:

Per Krusell & Tony Smith: Is Piketty’s “Second Legislation of Capitalism” Basic?‘[Piketty’s] argument in regards to the conduct of ok/y as progress slows, in its disarming simplicity, doesn’t absolutely resonate with these of us who’ve studied fundamental progress concept… or… optimizing progress…. Did we miss one thing vital, even basic, that has been proper in entrance of us all alongside? These of you with customary trendy coaching… have in all probability already observed the distinction between Piketty’s equation and the textbook model…. The capital-to-income ratio just isn’t s/g however somewhat s/(g+δ), the place δ is the speed at which capital depreciates when progress falls all the way in which to zero, the denominator wouldn’t go to zero however as a substitute would go from, say 0.12—with g round 0.02 and δ=0.1 as cheap estimates—to 0.1…’

LINK: <https://internet.archive.org/internet/20150529012920/http://www.econ.yale.edu/smith/piketty1.pdf>

James Hamilton: Educating Brad DeLong: ‘Reader Salim factors out that I used to be misinterpreting Piketty’s use of a ten% determine in his e-book’s calculations of depreciation. Piketty makes use of 10% for depreciation as a p.c of GDP, not as a p.c of capital as my authentic put up recommended. So as to not mislead, I’ve deleted the incorrect paragraphs that had been included within the first model of this put up…’

LINK: <https://econbrowser.com/archives/2014/06/educating-brad-delong>

Per Krusell: ‘We think about the topic of Piketty’s work actually vital…. This… nonetheless, isn’t any excuse for utilizing insufficient methodology or deceptive arguments…. We offered an instance calculation the place we assigned values to parameters—amongst them the speed of depreciation. DeLong’s most important level is that the speed we’re utilizing is just too excessive…. It’s, nonetheless, disappointing that DeLong’s most important level is a element in an instance aimed primarily, it appears, at discrediting us by making us seem like incompetent macroeconomists…. Now we have learn Piketty’s e-book and papers, and so we after all know that Piketty is aware of; our be aware is thus not written for him however as a substitute, as we are saying within the introduction to the paper, for all of those that is likely to be puzzled by the placing consequence that he derives from his non-standard concept…’

LINK: <https://ekonomistas.se/2014/05/29/krusell-och-smith-darfor-koper-vi-inte-pikettys-prognos/>

Brad DeLong: Brad DeLong brad.delong@gmail.com Wed, Jun 4, 2014, 2:34 PM: Please inform me if I’m loopy….

Piketty’s estimates of the capital/annual revenue ratio in France and Britain in 1910 are each equal to 7. At an annual depreciation price of 10% and with a net-of-depreciation idea of revenue, that signifies that 41.176% of gross revenue is dedicated to changing worn-out capital.

That may’t be what anyone thinks, can it? For Piketty’s functions, a ten%/12 months price of deprecation can’t be a good choice can it? Krusell and Smith’s selection of a ten%/12 months depreciation price to calibrate Piketty’s mannequin is mindless, does it?

Do individuals actually suppose that in 1900 41.176% of French gross output was taken up by capital consumption?

Bodily capital depreciation charges in progress (versus business-cycle) fashions are extra like 5% than 10%, aren’t they?

And to the prolong {that a} substantial chunk of your capital inventory takes the type of high-productivity land–which doesn’t depreciate–5% is just too giant, isn’t it?

Am I loopy?

Sincerely Yours,

Brad DeLong

Thomas Piketty: ’Hiya, we do present long term sequence on capital depreciation in our “Capital is again” paper with Gabriel (see <http://piketty.pse.ens.fr/capitalisback>, appendix nation tables US.8, JP.8, and so forth.). The sequence are imperfect and incomplete, however they present that in just about each nation capital depreciation has risen from 5–8% of GDP within the nineteenth century and early twentieth century to 10–13% of GDP within the late twentieth and early twenty first centuries, i.e. from about 1% of capital inventory to about 2%…

Finest,

Thomas’

Pricey Professors Krusell, Smith, Hamilton:

This isn’t going properly in any respect….

At Piketty’s reported wealth-to-annual-income ratio for France in 1910 of 700%, a ten%/12 months depreciation price implies that capital consumption is 70% of web revenue—41% of gross output.

Thus I’ve seven questions:

-

Do you consider that capital consumption was 70% of web revenue/41% of gross output in France in 1910?

-

Should you accomplish that consider, how is such a remarkably excessive share–40% of all financial exercise in France dedicated to changing and repairing capital because it wears out and turns into out of date–in step with even a floor acquaintance of the construction of the French economic system in 1910?

-

Should you accomplish that consider, are you able to level me to any sources to again up such an enormous wedge between gross output and web revenue, particularly since Piketty and Zucman’s estimates of the wedge between gross output and web revenue are typically within the 5–8% vary for the nineteenth century and the ten–13% vary for as we speak?

-

If not, why did you assume a deprecation price that may result in such an absurd image of the construction of the French economic system as of 1910?

-

Have you considered what the suitable depreciation price must be?

-

How responsive do you consider the gross financial savings price is to shifts within the wealth-to-annual-income ratio W/Y?

-

How a lot belief do you might have in life-cycle fashions of the affect of wealth on consumption in an atmosphere of utmost inequality, like that of the Belle Époque, or (maybe) the mid–twenty first century?

Sincerely yours,

Brad DeLong

Per Krusell: ‘I actually didn’t recognize the tone of your blogs on this matter. Due to the significance of the subject coated within the e-book—it’s one I care tremendously about—and since so many individuals are fascinated about it, I nonetheless determined it made sense to jot down a brief reply along with Tony. However, generally, on the few events after I write columns or visitor blogs, I’ve a rule not to reply to individuals who don’t keep a minimal of politeness of their questions/feedback. With out this rule, it might merely be too emotionally draining for me, and easily not price it. For the reason that tone of the e-mail you simply despatched remains to be somewhat disagreeable, with rhetorical questions and a transparent unwillingness to interact in our arguments, I’ll henceforth not reply…’

And so let me give the final phrase to Thomas Piketty:

Thomas Piketty: ’Thomas Piketty: ‘There are big variations throughout industries and throughout belongings, and depreciation charges might be so much increased in some sectors. Similar factor for capital depth. The prolemb with taking away the housing sector (a very capital intensive sector) from mixture capital inventory is that when you begin to do this it’s not clear the place to cease (e.g. vitality is one other capital intensive sector). So we favor to begin from an mixture macro perspective (together with housing), and right here it’s clear that 10% or 5% depreciation charges don’t make sense…’

<https://braddelong.substack.com/p/briefly-noted-for-2021-05-11-tu>