{kind=link}

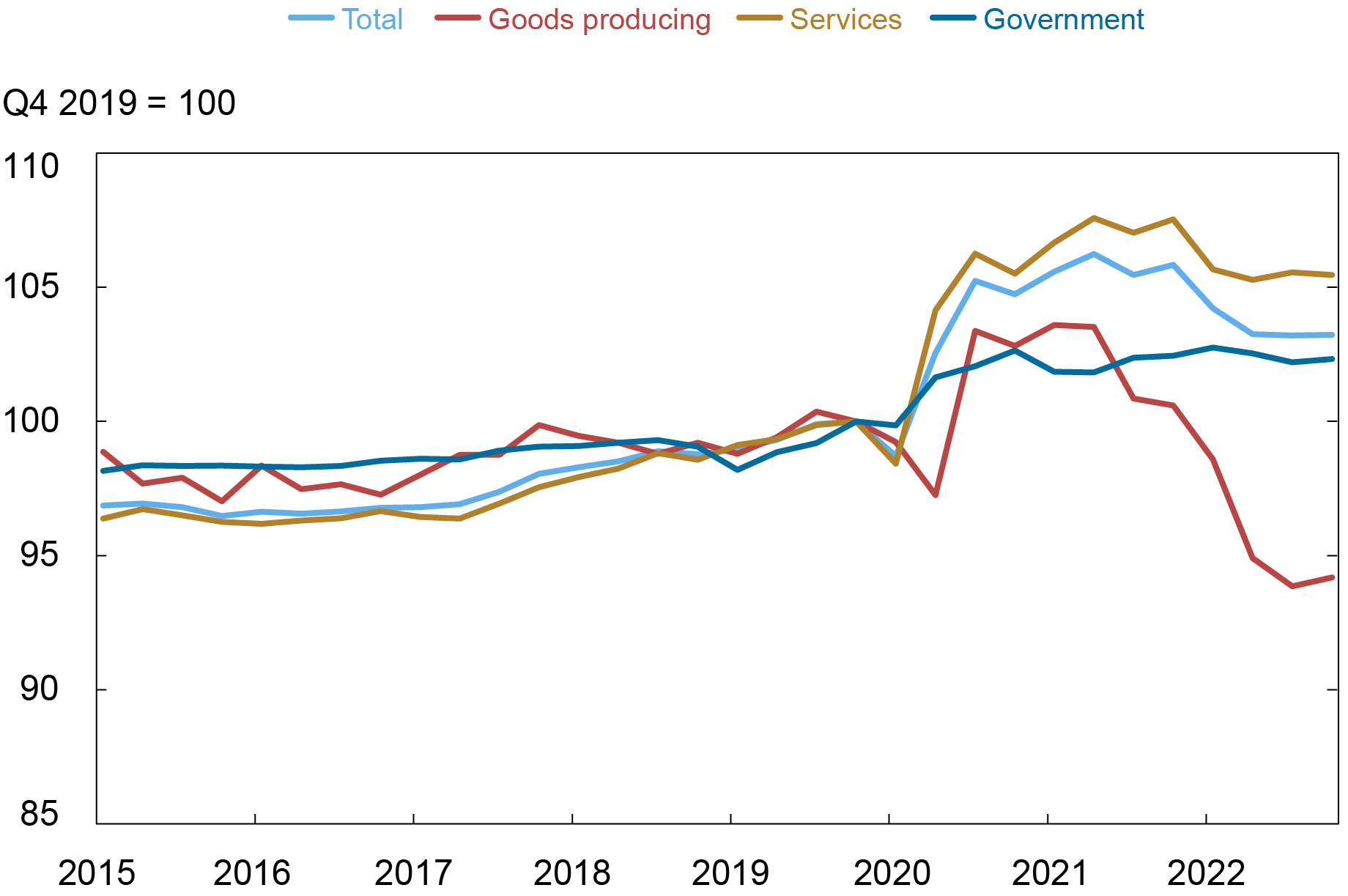

Job beneficial properties exceeded output progress in 2022, bringing GDP per employee again right down to its pattern degree after being effectively above for an prolonged interval. Employment is consequently set to develop slower than output going ahead, because it usually does. Breaking down the GDP per employee by {industry}, although, reveals a big divergence between the companies and goods-producing sectors. Productiveness within the companies sector was modestly above its pre-pandemic path on the finish of final 12 months, suggesting room for comparatively sturdy employment progress, with the hole significantly massive within the well being care, skilled and enterprise companies, and leisure and hospitality sectors. Productiveness in goods-producing industries, although, was depressed, implying that payroll progress is about to lag that sector’s GDP progress.

Output by Business

The primary launch of GDP information from the Bureau of Financial Evaluation seems at output from the demand-side perspective, with output evaluated by way of expenditures by households, companies, governments and the remainder of the world. Two months later, one other set of knowledge is revealed that breaks down GDP by {industry}, giving a supply-side view of the financial system’s efficiency. To know these information, do not forget that GDP is a value-added idea and isn’t the identical as gross output. The sale of a loaf of bread displays the gross output of bread, with value-added contributions from each the products facet (manufacturing and agricultural) and companies facet (retail, wholesale, transportation, and monetary, amongst others.) A person {industry}’s GDP is a measure of how that sector’s labor and capital inputs, together with the group of manufacturing, have added worth to inputs from different home industries and imports.

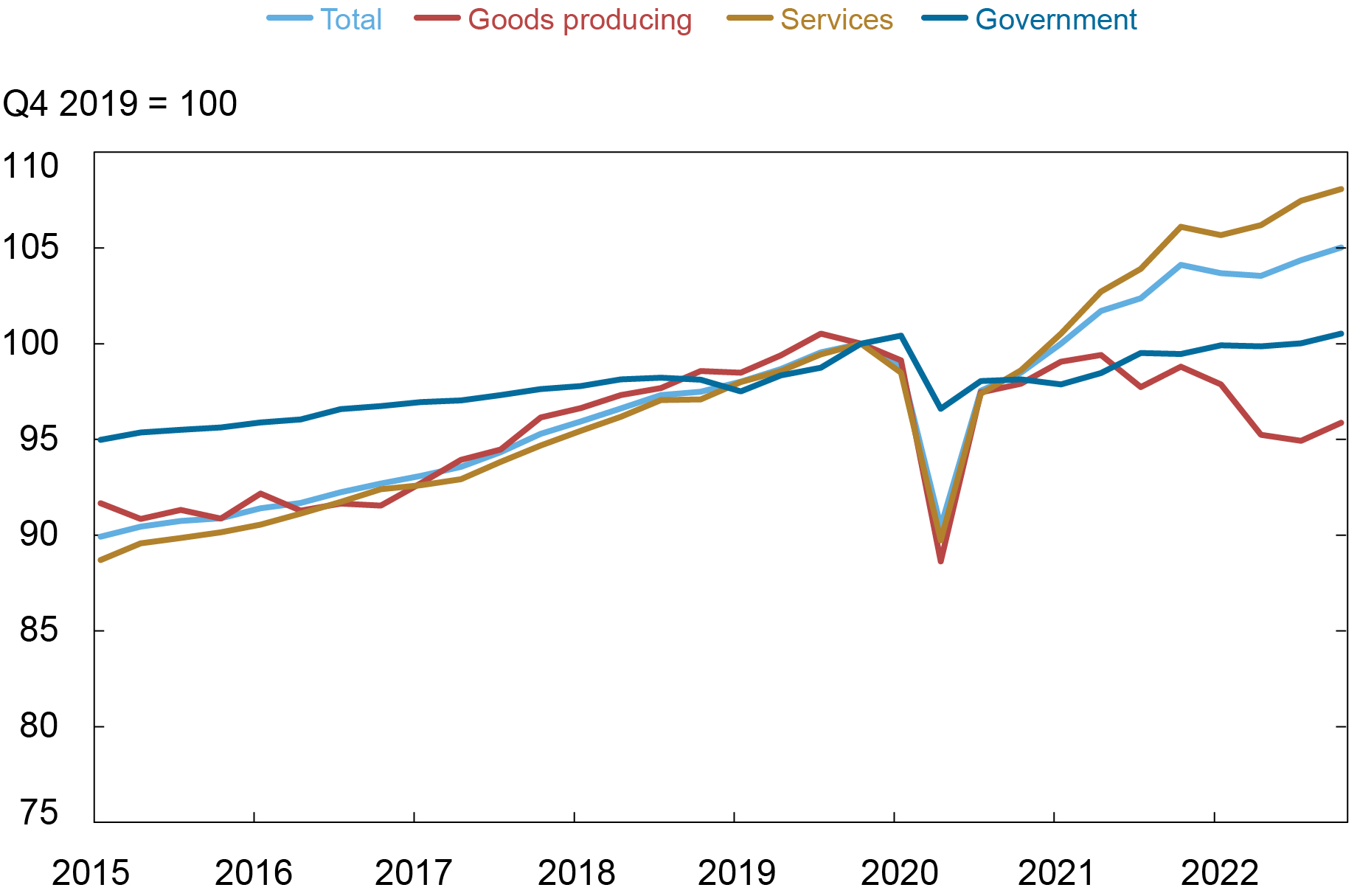

The chart under divides actual GDP into the goods-producing sector (mining, development, and manufacturing) and personal companies (wholesale, retail, transportation, warehousing, well being care, monetary, leisure and hospitality, data, {and professional} and enterprise companies), with the values listed in order that 2019:This fall=100. Earlier than the pandemic, each companies and goods-producing sectors grew according to the entire financial system, with each rising at round a 2.5 % annual charge from 2014-19, whereas the general public sector grew at a 1 % charge over the identical timeframe.

The Providers Sector Grew A lot Quicker than the Remainder of the Economic system through the Pandemic

Notice: Personal companies was 70.3 % of nominal GDP in 2019, the goods-producing sector was 17.5 %, and authorities was 12.3 %.

The chart reveals that progress for the reason that begin of the pandemic has been primarily restricted to the companies sector, with flat contribution from the general public sector and a decline in output within the goods-producing sector. From 2019:This fall by 2022:This fall, GDP rose at 1.7 % annual charge, with the personal companies sector GDP rising at 2.6 % charge, the goods-producing output falling at a 1.4 % charge, and the general public sector output rising at a 0.2 % charge.

The relative power of the companies sector might sound stunning provided that there was a big shift in client spending to items and away from companies through the pandemic. However take into account the how a lot of the worth added behind any items buy is equipped by the transport, wholesale, and retail sectors. That is much more the case when the great is imported as an alternative of produced domestically.

Productiveness by Business

Productiveness, measured right here by GDP per employee, can be utilized to judge how effectively employment tracked output through the pandemic interval. Industries initially responded to the financial system shutting down within the second quarter of 2020 by decreasing their workforce and these jobs didn’t all come again when the financial system staged a strong restoration in third quarter. (The main target right here is on payrolls, however observe that common hours labored elevated when the financial system rebounded, which means that output per hour didn’t rise as a lot as output per employee in 2020-21. This wedge disappeared over the course of 2022.)

Productiveness was flat for the entire financial system in 2021 as each payrolls and the financial system grew at quick charges. Particularly, output rose 6 % over the 4 quarters and payrolls rose 5 % over the identical interval. By sector, companies output was up 8 % versus payrolls up 6 % (greater productiveness), goods-producing output was up 1 % versus payrolls growing 3 % (decrease), and authorities output was up 1 % versus payrolls up 2 % (decrease).

In 2022, total productiveness lastly fell as GDP progress slowed to 1 % whereas payrolls rose 3 %. By sector, companies GDP grew 2 % versus payrolls up 4 %, goods-producing output fell 3 % versus payrolls up 4 %, and authorities output and payrolls each grew 1 %.

With 2022’s retreat, total productiveness on the finish of final 12 months was close to or modestly above its pattern path, with a optimistic hole in companies offsetting a big unfavourable hole for the goods-producing sector. In companies, the hole was largely as a result of well being care, skilled and enterprise, and leisure and hospitality companies industries, whereas the depressed productiveness for the goods-producing sectors was broad primarily based, with low readings for mining, development, and manufacturing.

Output per Employee within the Items-Producing Sector Was Unusually Low on the Finish of 2022

Payrolls and Output

The mixture in 2022 of a steep slowdown of GDP progress and continued sturdy employment progress introduced the extent of productiveness again down to close its pattern path. Whereas GDP-by-industry information are usually not but out there for 2023:Q1, preliminary releases have total payroll progress exceeding output progress, bringing the productiveness index within the chart above down by lower than half a degree. Going ahead, this productiveness studying means that payrolls are poised to return to rising slower than output, according to productiveness trending up over time.

The {industry} breakdown reveals how this story differs throughout industries. Providers employment has some room to develop above output significantly within the well being care, skilled and enterprise companies, and leisure and hospitality sectors. The outlook is much less sanguine for the goods-producing sector, with its productiveness effectively under pattern on the finish of final 12 months. Companies have employed aggressively even within the face of that sector’s declining GDP. Due to the ensuing low degree of productiveness, employment beneficial properties within the items sector might be fairly gradual relative to any restoration in its output.

Thomas Klitgaard is an financial analysis advisor in Worldwide Research within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Ethan Nourbash is a analysis analyst within the Federal Reserve Financial institution of New York’s Analysis and Statistics Group.

Find out how to cite this publish:

Thomas Klitgaard and Ethan Nourbash, “Assessing the Outlook for Employment throughout Industries,” Federal Reserve Financial institution of New York Liberty Road Economics, Could 10, 2023, https://libertystreeteconomics.newyorkfed.org/2023/05/assessing-the-outlook-for-employment-across-industries/.

Disclaimer

The views expressed on this publish are these of the creator(s) and don’t essentially replicate the place of the Federal Reserve Financial institution of New York or the Federal Reserve System. Any errors or omissions are the accountability of the creator(s).