{kind=link}

Conventional ILPs had been was in style in an period the place customers flocked to hybrid insurance policies that supplied each insurance coverage safety and funding returns. Nevertheless, the price additionally meant that clients noticed their premiums more and more get eroded by insurance coverage expenses as they obtained older, with much less left for funding. At present, to enchantment to the youthful technology, many insurers have launched pure-investment ILPs, with no (or minimal) insurance coverage expenses. However are these actually price your time?

The issue with older ILPs

Conventional ILPs had been launched as a hybrid coverage offering each insurance coverage safety and funding returns, in response to an period the place customers valued 2-in-1 and even 3-in-1 options.

Nevertheless, what was much less identified was the technical particulars of how these ILPs had been designed to work i.e. your premiums are used to purchase into models of sub-funds (funding funds), after which bought to fund the price of your insurance coverage expenses, which naturally go up as you grow old.

This construction (which you’ll test within the charges and allocation desk of your coverage) meant that for customers, their premiums obtained more and more eroded by expenses over time, with much less left for funding.

Because of this, even for loyal customers who caught to the plan for an prolonged variety of years, they began to see their prices go up resulting from rising mortality expenses, to the purpose the place their funding models would quickly not be sufficient to pay for the price of sustaining their safety.

Powerful.

Have trendy ILPs improved?

At present, we all know higher. In response to all of the discussions surrounding conventional ILPs, many insurers have additionally stored up with the instances and have now launched pure-investment ILPs, with the next improved options:

- 100% of your premiums get invested from Day 1

- No (or minimal) insurance coverage expenses

- Welcome bonuses and loyalty bonuses to reward you for staying loyal to the plan over time

These primarily addressed what customers didn’t like about conventional ILPs:

- Premiums go in direction of paying for gross sales expenses first (front-loaded)

- Much less premiums get invested from Day 1 (shopper doesn’t get the total impact of compounding)

- Rising insurance coverage expenses with age

What hasn’t modified is the price; clearly, investing your cash by way of an ILP will price greater than in case you DIY.

Identical to how ordering a birthday cake from a longtime baker will price you greater than in case you bake your personal cake.

Therefore, in case you *do* determine to go along with an ILP, you shouldn’t be evaluating with the prices of DIY, however moderately, consider the trade-offs and decide in the event that they make sense in your profile.

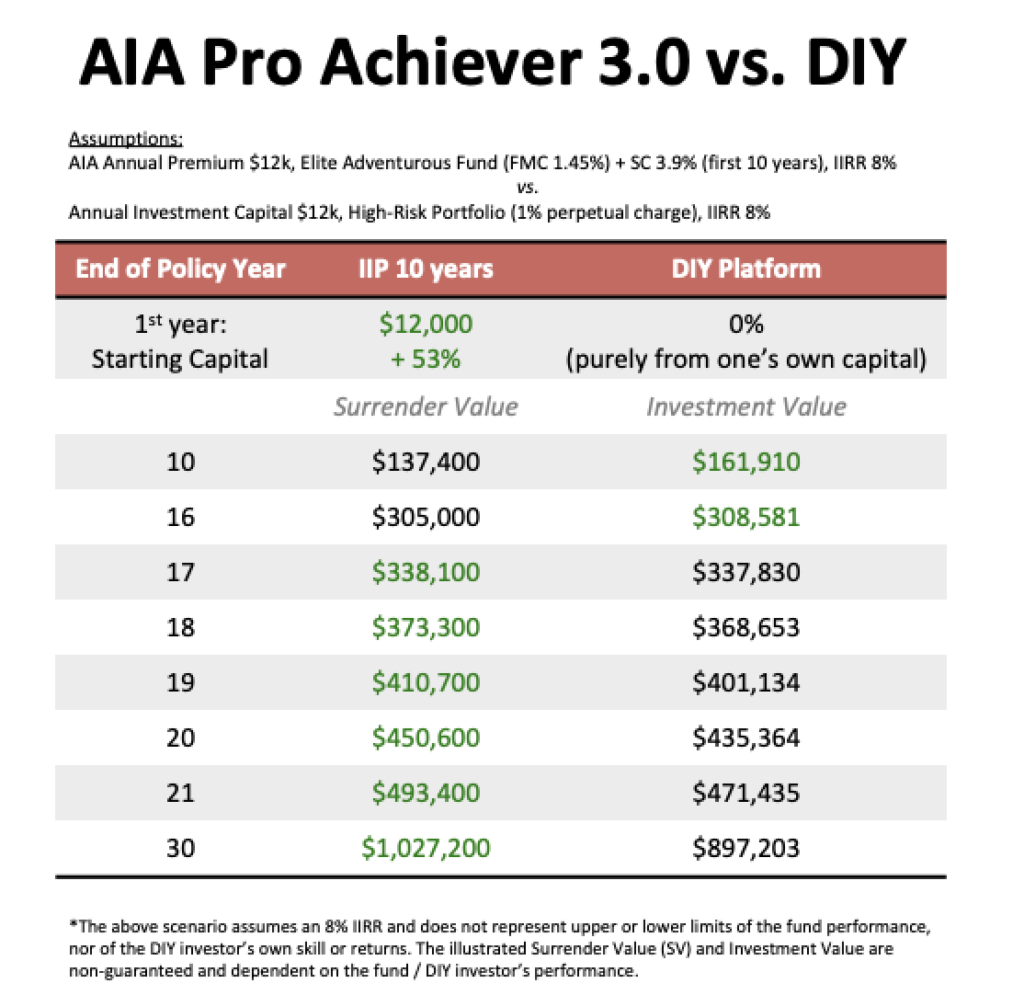

Right here’s an instance, utilizing AIA Professional Achiever 3.0 as an example:

Essential disclaimer: that is merely a basic illustration and NOT monetary recommendation.

Utilizing an ILP to make sure you don’t veer off-course

Let’s think about Jack, who’s a dad of two and needs to speculate for each his retirement in addition to his youngsters’s futures. He has $50,000 in liquid financial savings that he needs to develop, however isn’t certain of the place he ought to put it in. He tried investing throughout the pandemic, however is unsure if he needs to do it himself for the long-term, particularly as most of the shares he was influenced to purchase again then (Tesla, Palantir, Roku) are very a lot within the crimson.

He meets up together with his Monetary Providers Advisor who then recommends AIA Professional Achiever 3.0 to him, and he likes the concept that he can use the plan to attain the next funding goals:

- 100% of his premiums get invested from Day 1

- He can select his personal funding length with Preliminary Funding Durations (IIP) (10/15/20 years)1 to “power” him into staying dedicated to the funding plan, in order that he doesn’t “hen out” of the market even throughout unhealthy or emotional instances

- Free fund switching in order that if his danger urge for food modifications, he is not going to incur any transaction charges in altering his funding portfolio

- Supplementary Fees are just for the primary 10 years

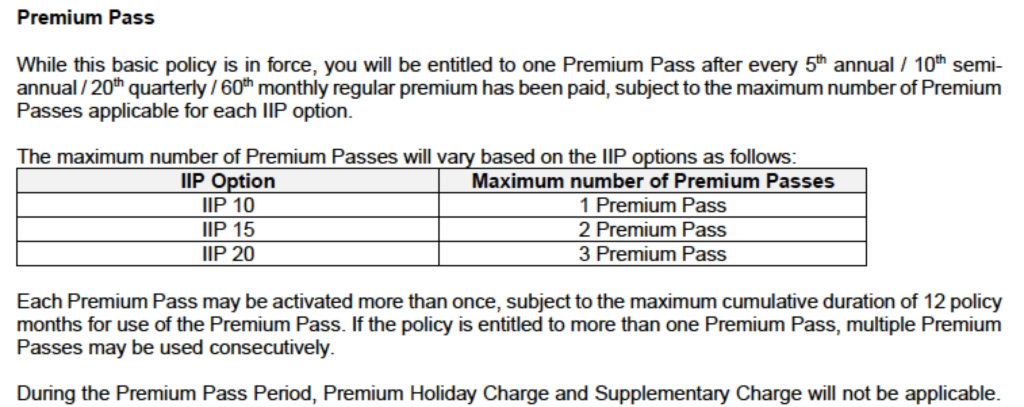

- For each 5 years of premiums paid, he will get 1 premium go (choice to take a break from paying premiums for as much as 12 months, with no expenses in contrast to a premium vacation)

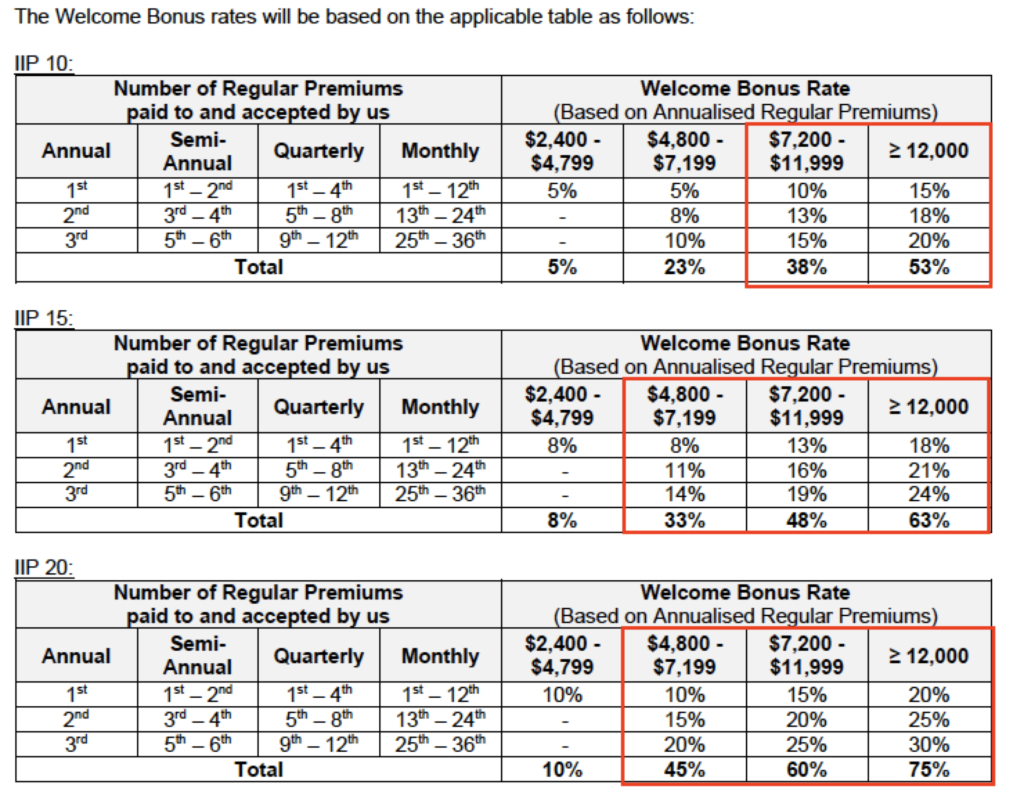

- Excessive welcome bonus2 of as much as 75% (53% if he can afford to speculate $1,000 a month, for IIP of 10 years)

- Other than top-ups, clients can also proceed to pay common premiums (past the preliminary funding interval) and earn Particular Bonuses3 of as much as 8% of standard premiums

After all, he additionally takes notice of the next trade-offs:

- If he needs to speculate greater than what he initially dedicated to, there can be a 5% gross sales cost (on ad-hoc top-ups)

- If he buys this plan, he wants to make sure he’s dedicated to it and does not cancel it midway by way of, in any other case he’ll incur hefty penalty expenses

Whereas he’s not a fan of the lock-up interval, he likes how the illiquidity will guarantee he stays on monitor to his long-term funding targets, particularly as he worries that he’ll panic and promote his liquid investments once more on the first signal of hassle (like what he did with Tesla).

Jack decides to take a while to mull over it, and calls his savvy DIY investor buddy out for a cup of espresso, who then tells him this:

- “ILPs have larger prices, you’d be higher off DIY-ing! Come, I educate you.”

Sadly, after spending per week together with his investor buddy attempting to learn to DIY, Jack begins to battle as a result of he realizes that he has completely no ardour to check companies or sustain with their information, and that he’s too emotional for his personal good (he remembers shopping for Tesla at $300 in 2021 when Youtubers had been speaking about it, after which promoting it off at $120 in December 2022 after listening to that its CEO Elon Musk cashed out over $3.6 billion of the inventory, solely to remorse it now that Tesla has rebounded again to $200). Deep down, Jack additionally feels that he’d be higher off specializing in his profession to earn cash, the place he has been steadily climbing the company ladder and is poised to get promoted to Director in a few years.

Jack makes his choice: he’ll decide to investing $1,000 a month into AIA Professional Achiever 3.0 with IIP of 10 years, and attempt to DIY the remaining by himself.

To ensure he won’t ever be caught in a scenario the place he has no alternative however to cancel his coverage (since there are penalty expenses at stake), Jack decides to put aside $24,000 into short-term mounted revenue choices, switching between MAS T-bills, Singapore Financial savings Bonds, money administration merchandise and glued revenue deposits so he retains liquidity.

With the Premium Cross4 characteristic that enables him to pause the coverage (with out incurring expenses) if he ever must, Jack figures that even within the worst-case situation (though he doubts he’ll ever be unemployed for greater than 2 years) he determined to play it secure since there are penalty expenses at stake as soon as he takes up this coverage.

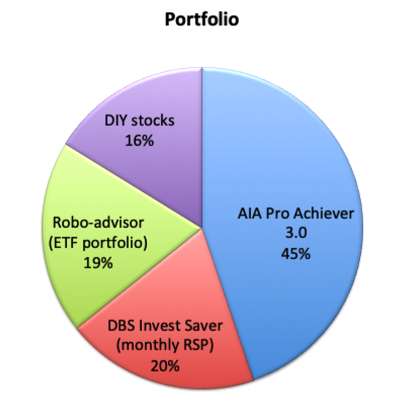

Together with his remaining funds, he decides to arrange 2 funding accounts:

- $500 month-to-month right into a Common Financial savings Plan for unit trusts (at 0.82% gross sales cost month-to-month)

- $500 month-to-month right into a robo-advisor for ETFs (0.65% p.a. administration charge every year)

- $5,000 to kickstart his shares portfolio

- $6,000 to maintain as money

A 12 months later, Jack has determined that this mix works for him greatest because it provides him sufficient room to DIY some investments with out an excessive amount of stress, whereas concurrently constructing his profession (the place he has simply gotten a promotion, hooray!).

Though his investor buddy boasts of how he’s capable of pay lower than 1% in charges, Jack feels the fees he pays to AIA for his ILP is definitely worth the trade-off, particularly for the reason that charges stop after the primary 10 years vs. his different associates who’re being charged 1% platform charges perpetually on their portfolio.

One of the best factor he likes is that after 10 years (his chosen funding interval), he will get to determine whether or not he needs to proceed paying premiums or to cease and let the coverage roll. On the similar time, he could have the liquidity by then to withdraw as and when he likes.

After all, Jack is an imaginary character, however I hope it provides you an concept of the way you may be capable to tweak or give you your personal as effectively.

When is an ILP unsuitable?

Clearly, for Jack’s good buddy who’s a talented and disciplined DIY investor who doesn’t bail on the first signal of market volatility, a plan like this will not work for him.

Neither would it not be appropriate for many who have dedication points, or those that would be the first to cancel their insurance coverage insurance policies throughout monetary hardship.

It is usually not appropriate for folk whose final goal is to go for low-cost, as a result of there are at all times larger charges while you outsource one thing as an alternative of DIY.

Conclusion

When you’re tempted into shopping for an ILP, the important thing questions you must first ask your self are:

- What is going to you do with the funds in case you’re not investing it into an ILP?

- Will you, and may you, DIY?

- If not, are you keen to learn to DIY investing?

- Are you assured of investing in your personal returns in case you go for lower-cost choices?

Your individual solutions to the above questions ought to offer you a good suggestion of what monetary instruments can be appropriate so that you can deploy in your personal funding portfolio.

And in case you’ve thought-about all these elements and determined that DIY investing could be higher for you as an alternative, then I’ll level you to these helpful sources right here that will help you up your investing expertise.

After all, AIA Professional Achiever 3.0 is just not the one ILP out there, however with the upper welcome bonuses and permitting for a premium go (as an alternative of a premium vacation), you possibly can discover it additional to see if it’ll be appropriate for you – and weigh its execs and cons like how Jack evaluated it for himself.

Disclosure: This text is sponsored, and has been fact-checked, by AIA to make sure product accuracy. Whereas Jack is an imaginary character, he’s impressed by the conversations I’ve had with readers who advised me why they determined to purchase an ILP after trying to DIY by themselves throughout the pandemic, so I hope this text helps to cowl the totally different concerns you must keep in mind earlier than committing to 1.

For detailed product phrases and situations, please head over to AIA’s web site right here.

Notes on AIA Professional Achiever 3.0: 1 The plan affords IIP choices of 10, 15 or 20 years. In the course of the IIP, sure expenses might apply, comparable to supplementary expenses (if relevant), premium vacation expenses, premium discount expenses, full give up expenses and partial withdrawal expenses. Any dividend payouts (if relevant) can be routinely reinvested into the coverage throughout the IIP. 2 Welcome Bonus in your common premium can be payable for the first, 2nd, and third annual premium acquired (topic to the annualised premium quantity and IIP). 3 Particular Bonus of 5% of standard premium can be payable for the tenth - twentieth annual premium acquired, and will increase to eight% of standard premium from the twenty first annual premium acquired onwards. 4 You can be entitled to 1 premium go after each fifth annual common premium has been paid, topic to the utmost variety of premium passes for every IIP possibility. Every premium go could also be activated greater than as soon as for a most cumulative length of twelve (12) coverage months.

Essential Disclaimer:

This insurance coverage plan is underwritten by AIA Singapore Non-public Restricted (Reg. No. 201106386R) (“AIA”). All insurance coverage functions are topic to AIA’s underwriting and acceptance. This isn't a contract of insurance coverage. The exact phrases and situations of this plan, together with exclusions whereby the advantages underneath your coverage will not be paid out, are specified within the coverage contract. You're suggested to learn the coverage contract. AIA Professional Achiever 3.0 is a daily premium Funding-linked Plan (ILP) provided by AIA. Investments on this plan are topic to funding dangers together with the doable lack of the principal quantity invested. The efficiency of the ILP sub-fund(s) is just not assured and the worth of the models within the ILP sub-fund(s) and the revenue accruing to the models, if any, might fall or rise. Previous efficiency is just not essentially indicative of the long run efficiency of the ILP sub-fund(s). The precise coverage worth will rely on the precise efficiency of the coverage in addition to any alterations comparable to variation within the Insured Quantity or premium, comparable to premium vacation or partial withdrawals. There's a chance that the coverage worth will fall to zero and on this case, the coverage can be terminated. Policyholder can keep away from the coverage lapsing by topping up further premium. It is best to search recommendation from a certified advisor and browse the product abstract and product highlights sheet(s) earlier than deciding whether or not the product is appropriate for you. A product abstract and product highlights sheet(s) referring to the ILP sub-fund(s) can be found and could also be obtained out of your AIA Monetary Providers Advisor or Insurance coverage Consultant. A possible investor ought to learn the product abstract and product highlights sheet(s) earlier than deciding whether or not to subscribe for models within the ILP sub-fund(s). As shopping for a life insurance coverage coverage is a long-term dedication, an early termination of the coverage normally includes excessive prices and the give up worth, if any, that's payable to you might be zero or lower than the full premiums paid. It is best to think about rigorously earlier than terminating the coverage or switching to a brand new one as there could also be disadvantages in doing so. The brand new coverage might price extra or have fewer advantages on the similar price. Protected as much as specified limits by SDIC. This commercial has not been reviewed by the Financial Authority of Singapore. The data is appropriate as at 25 February 2023.