{kind=link}

Wipro Ltd. – Western India Merchandise

Wipro is likely one of the main international IT, consulting and enterprise course of companies firm. It’s the fourth largest Indian participant within the international IT companies business, when it comes to income, after Tata Consultancy Companies (TCS), Infosys Restricted (Infosys) and HCL Applied sciences Restricted (HCL). They harness the ability of cognitive computing, hyper-automation, robotics, cloud, analytics and rising applied sciences to assist their purchasers adapt to the digital world and make them profitable. Wipro was integrated in 1945 as Western India Greens Product Restricted and was predominantly a client care product producer until 1980 after which it diversified into the IT companies enterprise. With impact from April 1, 2012 (FY2013), the corporate demerged its different divisions (client care and lighting, medical tools and infrastructure engineering) right into a separate firm known as Wipro Enterprises Restricted (WEL), to boost its focus and permit each companies to pursue their particular person development methods. Wipro has over 258,000 devoted workers serving purchasers throughout six continents.

Merchandise & Companies:

The corporate’s Key choices beneath IT associated merchandise and Companies are digital technique advisory, customer-centric design, expertise consulting, IT consulting, customized software design, improvement, re-engineering and upkeep, techniques integration, package deal implementation, cloud infrastructure companies, analytics companies, enterprise course of companies, analysis and improvement and {hardware} and software program design to main enterprises worldwide.

Subsidiaries: As on FY22, the corporate had 140 Subsidiaries and 1 Affiliate firm.

Key Rationale:

- Diversified clientele – Wipro has a powerful base of 1,369 prospects with 95% of the enterprise generated from present purchasers in FY2022. Firm has added 428 new prospects in FY2022 as in opposition to 280 prospects in FY2021. For Q3FY23, the corporate added 80 new prospects. The overall energetic prospects on the finish of Q3FY23 stands at 1484. Shoppers in ‘Greater than USD 75 million’ bucket elevated from 27 in FY2021 to 29 in FY2022. The corporate is witnessing wholesome renewal of offers and including new offers from present purchasers within the discipline of digitization. Going ahead, Wipro is anticipated to take care of a diversified income stream throughout prospects in numerous segments.

- Document Deal Win – Wipro for the primary time reported a Complete Contract Worth (TCV) of US$ 4.3 bn for the quarter, which was up 26% YoY in CC phrases. The corporate’s giant deal TCV wins additionally stays sturdy with wins of 11 giant offers of US$ 1 bn. Wipro indicated that the deal wins are wholesome combine of recent wins & renewal. The corporate’s web workers through the quarter declined by 435 taking the whole worker power to 258,744 workers. Wipro indicated that the availability facet challenges are easing whereas LTM attrition additionally continues to say no. The LTM attrition through the quarter declined 180 bps QoQ to 21.2% whereas the quarterly annualised attrition declined 360 bps to 17.5%. The corporate expects attrition to average additional, which might be one of many levers for margin enchancment.

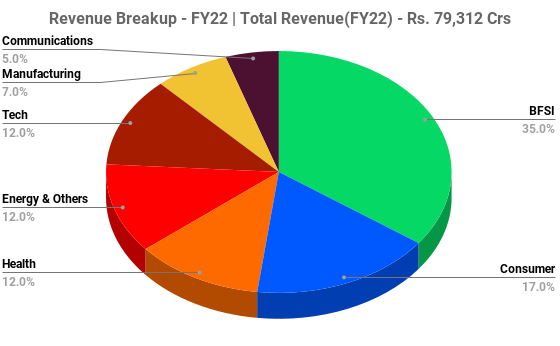

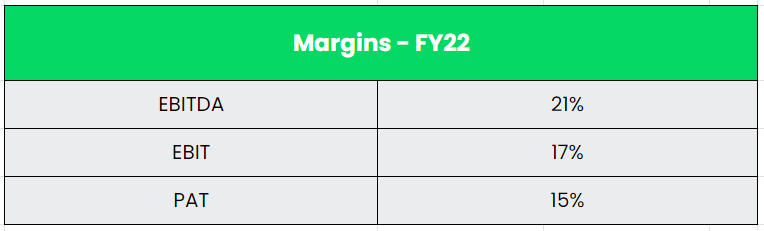

- Q3FY23 – The corporate generated a Gross Income of Rs.23,229 crs ($2.8 billion), a rise of three.1% QoQ and 14.4% YoY. IT Companies Phase Income elevated to $2,803.5 million, an enchancment of 6.2% YoY. Vertical clever, in CC phrases, well being (12% of combine), vitality (11% of combine), client (19% of combine) & manufacturing (7% of combine) reported development of 4.7%, 2.8%, 0.6% & 0.6% YoY, respectively, whereas BSFI (35% of combine), Communications (5% of combine) & Know-how (11% of combine) declined 0.2%, 2.6% & 1.3%, respectively. The corporate’s working margins, improved by 120bps and stood at 17.4% YoY, largely led by decrease working bills and a beneficial forex combine through the quarter. Its web revenue for Q3FY23 stood at Rs.3065 crs, registering a development of 15.7% QoQ.

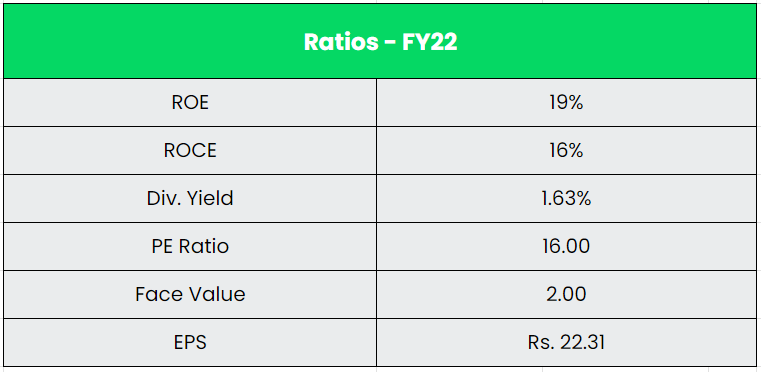

- Monetary Efficiency – The corporate has a powerful steadiness sheet a debt-to-equity ratio of 0.2 and a money and equivalents of Rs.36937 crs as of H1FY23. The corporate maintained a 20%+ EBITDA margins for a few years traditionally. The 5-year common RoE and RoCE of the corporate are 18% and 20%.

Trade:

The IT & BPM sector has turn out to be some of the vital development catalysts for the Indian economic system, contributing considerably to the nation’s GDP and public welfare. The IT business accounted for 7.4% of India’s GDP in FY22, and it’s anticipated to contribute 10% to India’s GDP by 2025. In accordance with Nationwide Affiliation of Software program and Service Corporations (Nasscom), the Indian IT business’s income touched US$ 227 billion in FY22, a 15.5% YoY development. The export income from this business (excluding e-commerce) has been estimated at near $178 Bn in FY2022. Indian software program product business is anticipated to succeed in US$ 100 billion by 2025. Indian firms are specializing in investing internationally to develop their international footprint and improve their international supply centres. The IT business added 4.45 lakh new workers in FY22, bringing the whole employment within the sector to 50 lakh workers. Over 280,000 workers had been reskilled and made digital expert in FY22. At 30-32% of business income, digital revenues grew 5 occasions the speed of general companies development.

Development Drivers:

- The pc software program and {hardware} sector in India attracted cumulative international direct funding (FDI) inflows price US$ 93.58 billion between April 2000-December 2022.

- Indian telecoms are providing 1GB cellular knowledge at $0.086 – one of many most cost-effective globally. By providing inexpensive knowledge to shoppers, the digital infrastructure permits ease of entry to companies like banking, governance and extra.

- Over 45 new knowledge centres to return up in India by 2025. Knowledge centres in India entice funding of $10 Bn since 2020.

Opponents: Infosys, LTIMindtree, and so forth.

Peer Evaluation:

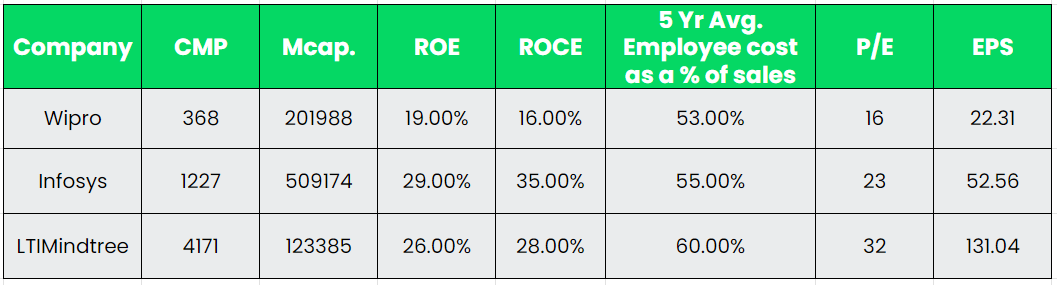

Whereas evaluating with friends, Wipro is buying and selling at a less expensive worth to earnings ratio. The 5-year common worker price as a % to gross sales stands at 53% for Wipro which is lower than its friends.

Outlook:

Administration acknowledged that tech spends remained sturdy through the quarter regardless of persevering with macro challenges leading to document order e book TCV of $4.3 bn of which 44% was derived from hyperscalers. Order e book has wholesome steadiness of renewals and new wins as Cloud & Engineering companies which noticed YoY of development of 25% & 45% respectively drove the expansion in bookings. Nevertheless, conversion of order e book to income will lag as a consequence of delay in determination making and minimize in discretionary spend. Firm expects to develop within the European area on the again of market share features and vendor consolidation alternatives. For FY23, administration expects income to develop within the vary of 11.5%-12% in CC phrases on the again of market share features, vendor consolidation alternatives, sturdy demand throughout cloud, engineering & safety. Additionally, Firm doesn’t foresee any slowdown in hyperscalers impeding the expansion.

Valuation:

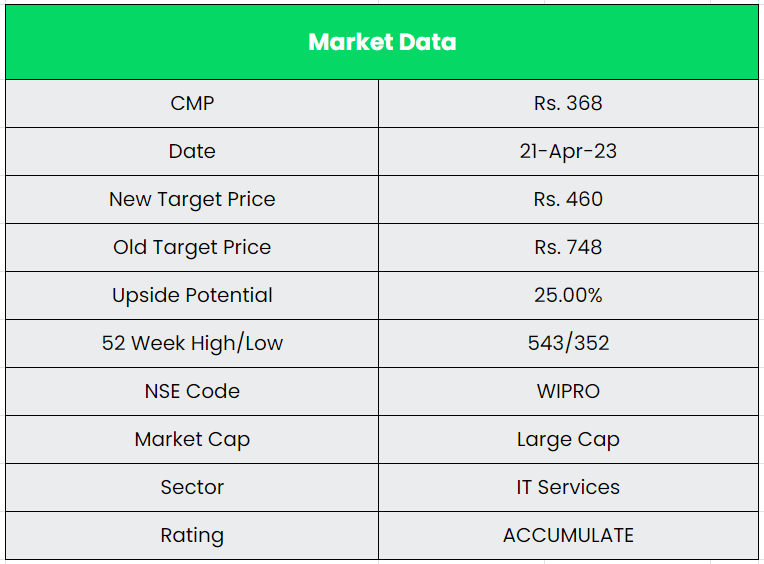

From a long-term perspective, we consider Wipro has a powerful deal pipeline and superior monetary construction. Additionally, the assured commentary from administration and the moderating attrition charge are constructive triggers within the inventory. We advocate an ACCUMULATE score within the inventory with the goal worth (TP) of Rs.460, 18x FY25E EPS.

Dangers:

- Foreign exchange Threat – Fluctuations within the USD-INR and GBP-INR and GBP-USD, as majority of the income comes from worldwide territories. Fluctuation within the currencies will affect the income of the corporate.

- Visa associated Threat – Improve in Visa charges will enhance the price. Rise within the visa charges will result in rise within the working price (Worker bills) to IT business. So, it performs a serious position within the IT business.

- Remuneration Threat – Wage hikes i.e., wage inflation might play as a spoil sport. Rising financial development will create extra jobs within the nation. This may finally give rise to wages hikes. Wage hikes will have an effect on the working margins of the corporate. So, fluctuation within the wages is a big danger in IT service Trade.

Different articles you might like

Submit Views:

977