{kind=link}

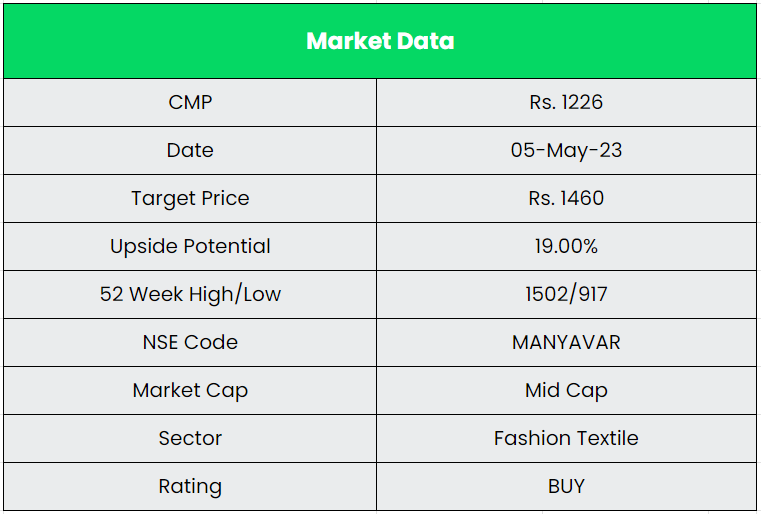

Vedant Fashions Ltd. – Manyavar Ethnic Put on

Headquartered in Kolkata, integrated in 2002 by Mr. Ravi Modi, Vedant Fashions Ltd. (VFL) presents Indian wedding ceremony & celebration put on for males, girls & children. The corporate focuses on enhancing its management place throughout the organized Indian wedding ceremony and celebration put on market by way of its numerous manufacturers together with its flagship model Manyavar, Twamev and Manthan inside males’s put on and Mohey within the girls’s Indian wedding ceremony and celebration put on market.

It’s the largest firm in India in males’s Indian wedding ceremony & celebration put on by Income, EBITDA & PAT as of FY20 Crisil report. The corporate has a pan-India presence with a retail footprint of 1.47 mn sq. ft. protecting over 245 cities and 649 shops (together with worldwide areas such because the US, Canada, UK and the UAE).

Merchandise & Providers:

The corporate is a one cease vacation spot for each event with a large product portfolio underneath 5 manufacturers.

Manyavar – Manyavar is the flagship Mens’ & Child’s model in mid-premium Indian wedding ceremony & celebration put on worth vary. It presents Kurtas, Sherwani, Jackets, Indo-western, and so on. for Males and Children.

Mohey – Mohey is an rising Mid premium model for Girls. It presents sarees, lehengas, Robes, and so on.

Twamev – Twamev is the premium model for Males. It presents of Kurtas, Sherwani, Jackets, Indo-western, and so on. for Males and Children.

Manthan – Manthan is the worth model for Males. It presents solely Kurta.

Mebaz – Mebaz is the mid premium model providing merchandise for all the household (Males, Girls & Children) within the South Indian area (AP & Telangana). It contains Kurtas, Sherwani, Jackets, Sarees, Lehengas, and so on.

Subsidiaries: As on FY23, the corporate had just one Subsidiary named Manyavar Creations Personal Restricted.

Key Rationale:

- Asset Gentle Enterprise Mannequin – The corporate follows an Asset gentle mannequin in each the manufacturing and gross sales. A lot of the firm’s manufacturing are carried out by Distributors with whom the corporate has a long-standing relationship and the remaining shall be completed in-house. The corporate has round 480+ registered distributors throughout 45 cities. On the gross sales half, the corporate was earlier operated in a enterprise mannequin with a mixture of COFO (Firm owned Franchise Operated), COCO (Firm owned Firm Operated) and FOFO (Franchise Owned Franchise Operated). From 2016-17, the corporate transformed its many of the COFO shops into FOFO shops which completely eliminated the capex and different fastened expense besides wage. With the above steps, the corporate turned out as a profitable Asset gentle mannequin which helps in rising the profitability.

- Technological Energy – The corporate is manner forward of its friends when it comes to know-how. They first examine the demand utilizing knowledge analytics and create designs as per the demand not like others who create the design first. VFL takes the total management of designing, stock choice and merchandising for its franchisee. The refilling of stock within the franchisee can be automated by a particular algorithm with no human intervention. The algorithm helps determine the shop stock/merchandising primarily based on components akin to locality, style, and desire in its current shops and benchmarking with comparable areas in new shops. The corporate additionally has a particular vendor portal to effectively handle them.

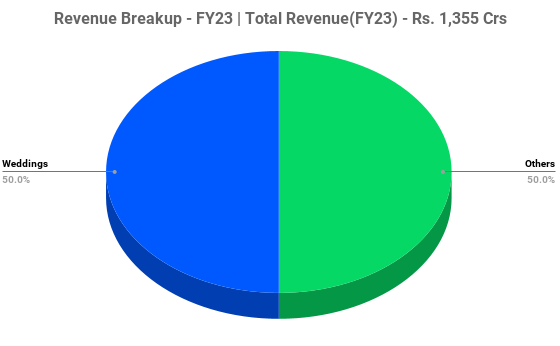

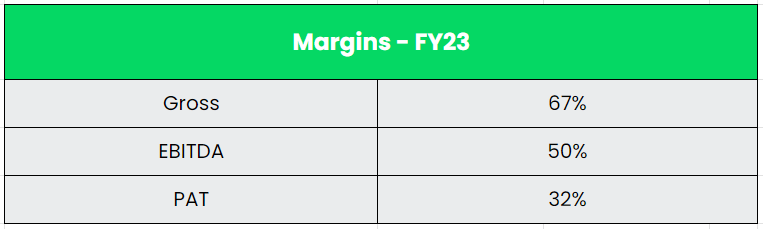

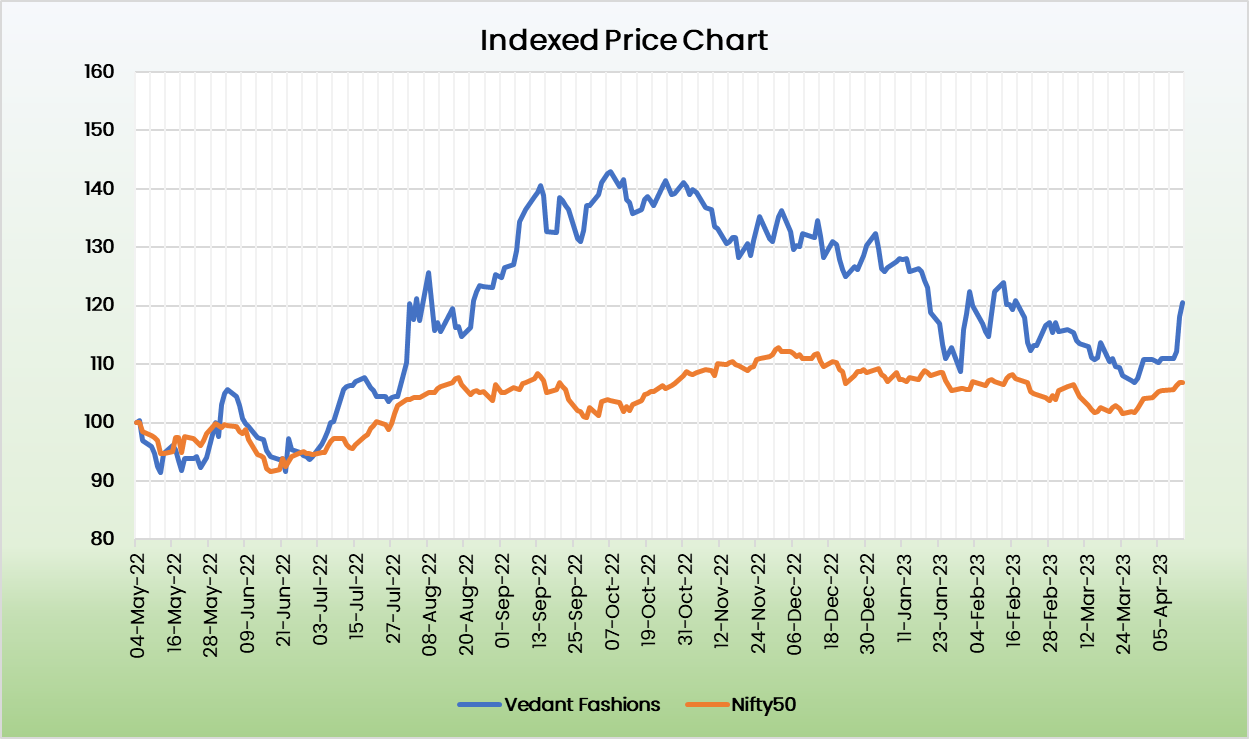

- Q4FY23 – Firm expanded its retail footprint presence by including ~75 ok sq. ft. retail space in Q4FY23 and a couple of.04 lacs sq. ft. retail space in FY23, with whole retail presence of 1.47 mn sq. ft. as of Mar’2023. It additionally expanded its worldwide presence with new shops in London (UK) and Canada in This fall FY23, and has presence in 4 Worldwide International locations (USA, UAE, Canada and UK. The corporate recorded the SSSG (Similar Retailer Gross sales Development) of 14% in Q4FY23 in comparison with Q4FY22 and 18.1% in FY23 in comparison with FY22. The income from operations of the corporate has grown at 15% YoY to Rs.342 crs in Q4FY23 and 30% YoY to Rs.1355 crs in FY23. The EBITDA margin for FY23 improved by ~190 bps to 50% from 48% in FY22. The revenue after tax of the corporate had a large progress of 36% YoY to Rs.429 crs in FY23 from Rs.315 crs in FY22.

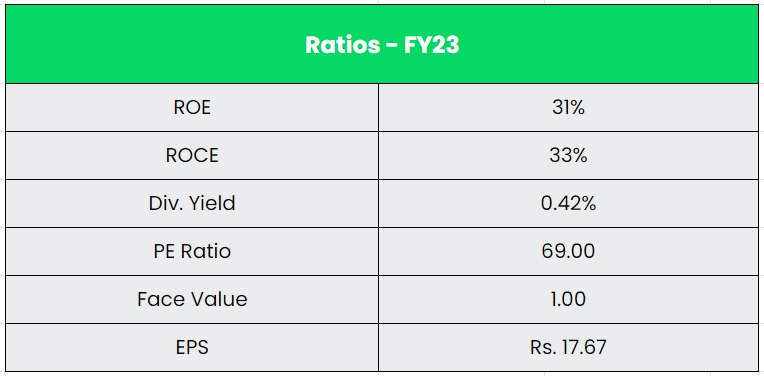

- Monetary Efficiency – The asset gentle mannequin and the effectivity within the operations are the 2 causes which made the corporate to generate constant progress within the margins and the earnings. The minimal capex for the corporate additionally attributed to a robust money conversion. The corporate’s income and PAT CAGR stands at 12% and 24% between FY18-23. The working cashflow of the corporate have grown at a CAGR of 55% for a similar interval from Rs.52 crs in FY18 to Rs.470 crs in FY23. The Working Cashflow to PAT (CFO/PAT) ratio stands at 110% in FY23 which signifies that the corporate is extraordinarily good at changing accounting revenue into money. The identical ratio for the typical of final 5 years (FY19-23) stands at a whopping 122%.

Trade:

India’s textiles sector is likely one of the oldest industries within the Indian economic system, relationship again to a number of centuries. The Indian textile and attire business is predicted to develop at 10% CAGR from 2019-20 to succeed in US$ 190 billion by 2025-26. India has a 4% share of the worldwide commerce in textiles and attire. India’s textile and attire exports (together with handicrafts) stood at US$ 44.4 billion in FY22, a 41% enhance YoY. The full Indian ethnic put on market as on FY20 stands at Rs.1,800 bn, out of which the celebration and event put on phase accounts for Rs.1,020 bn. The full Indian ethnic put on business is predicted to develop at a CAGR of 6% to Rs.2400 bn by FY25. The lads’s event and celebration put on phase, which stood at Rs.133 bn in FY20, reported 6% CAGR within the final 5 years. As per CRISIL, the market measurement of the marriage/celebration put on phase is predicted to extend to Rs.1,325-1,375 bn with a 15-17% CAGR over FY22-FY25.

Development Drivers:

- India is big marketplace for marketplace for celebration/wedding ceremony put on business with round 9.5-10 million weddings per 12 months.

- Common spending on bride/groom outfits in city India ranges round Rs.50k-100k. The upper common spending within the outfits & apparels are a results of improved earnings ranges among the many client. Any additional enhance within the earnings ranges will result in enhance in discretionary spending.

- The marriage and celebration market is witnessing a shift from the sooner tailored put on to the ready-to-wear phase, thereby benefitting branded readymade gamers which has a number of product varieties.

Opponents: Trent, ABFRL, TCNS Clothes, and so on.

Peer Evaluation:

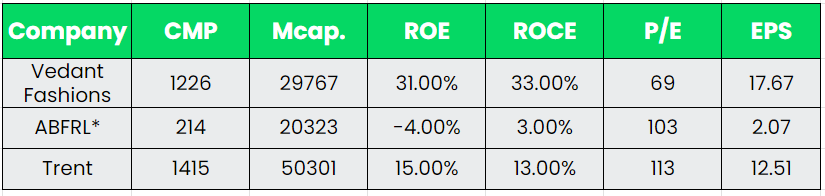

VFL doesn’t have any listed competitor within the full-fledged enterprise of promoting Indian Ethnic, wedding ceremony and celebration put on area. We thus examine VFL with different listed attire gamers. Trent not too long ago entered the ethnic area by launching a model named ‘Samoh‘ and ABFRL entered the area by buying the model ‘Sabsyachi’. Given the asset-light mannequin, VFL has higher margins in addition to return ratios, in comparison with different attire gamers.

*We took TTM EPS and FY22 return ratios (ROE & ROCE) for ABFRL

Outlook:

The corporate has a market share of 10% within the Males’s wedding ceremony/celebration put on class which is a extremely unorganised area. The branded phase in the identical class garners a market share of round 20-25% which reveals the massive underneath penetration and there’s a lot of room for the corporate to develop. The corporate’s robust design energy and choice by way of knowledge analytics (No low cost gross sales), superior know-how for provide chain, Automated vendor system and franchise pushed mannequin have supported the expansion of its enterprise with strong margins. Previously, the corporate’s retail footprint has grown at a CAGR of 16%. The administration stated that their thought is to proceed the identical degree of progress for the following two to 3 years and are planning to enter to new cities. The corporate can be engaged on a digital transformation program. The primary part of this system is in testing which incorporates improved options in appointments and consumer interface which is predicted to begin by mid Q1FY24. The second part will refresh the working platform with improved options associated to ordering, return, exchanges, and suggestions platform.

Valuation:

Vedant fashions with its flagship model ‘Manyavar’ has a protracted approach to develop within the largely unorganized market with much less competitors within the area of interest ethnic put on area. The superior margins and wholesome return ratios on account of environment friendly operations calls for a premium valuation for the corporate. We advocate a BUY ranking within the inventory with the goal worth (TP) of Rs.1460, 45x FY25E EPS.

Dangers:

- Inflationary Threat – Marriage ceremony and celebration put on phase comes underneath discretionary spending and any enhance in inflation will have an effect on the demand of the phase.

- Operational Threat – VFL manufactures principally from third social gathering distributors/jobbers. Reducing, embroidery, stitching and ending are completed by third-party jobbers, in response to the requirements specified by the corporate. Any disruption in operations of jobbers/distributors would have an effect on VFL’s efficiency.

- Aggressive Threat – Marriage ceremony put on Trade has a mixture of each branded and unbranded gamers. Along with the competitors from native and unorganised gamers, the corporate faces competitors from massive gamers like Trent, ABFRL, and so on.

Different articles chances are you’ll like

Publish Views:

579