{kind=link}

Final evening (Might 9, 2023), the Australian authorities delivered the newest fiscal assertion (aka ‘The Finances’), and, in doing so assured that unemployment would rise. A deliberate act of sabotage of dwelling requirements for deprived Australians. All of the hype was in regards to the miniscule fiscal surplus that was introduced as whether it is some form of badge of honour that politicians goal for. In the event that they went to the houses of the poor; in the event that they visited the general public hospital system that’s nonetheless straining below Covid and so on and years of fiscal neglect; in the event that they examined the state of local weather science; and if they only opened their eyes typically, they might see {that a} fiscal surplus is a sign at this stage in our historical past of deliberate neglect of the principle challenges of the day. Positive sufficient, the Authorities handed out some dollops of cost-of-living aid to low-income households – a couple of pennies within the scheme of issues. However whereas recording a surplus they nonetheless refused to raise the unemployment profit recipients above the poverty line and ensured their can be extra of the identical pressured to dwell in poverty. The priorities are all incorrect and that is one other neoliberal-lite effort from the Labor Get together.

The merciless failure to acknowledge the unemployed

In ‘Finances Paper No.1’, Assertion 2: Financial Outlook, we observe the next forecasts.

| Combination | 2022 (Precise) | 2023 | 2024 | 2025 |

| GDP development | 3.60 | 1.75 | 1.50 | 2.75 |

| Unemployment | 3.80 | 3.50 | 4.25 | 4.50 |

| Participation fee | 66.60 | 66.50 | 66.25 | 66.25 |

| Inflation | 6.50 | 6.00 | 3.25 | 2.75 |

The Treasury additionally point out that inhabitants development might be “2 per cent in 2022-23 and 1.7 per cent in 2023-24”.

Participation is forecast to fall marginally.

Notice the forecasts within the Desk are for calendar years and the inhabitants development predictions are for fiscal years.

If we assume the labour drive grows consistent with the assumed underlying inhabitants forecasts then it’s arduous to see how the unemployment fee improve could be confined to a forecasted 0.7 factors over the interval to 2025.

The well-known US economist Arthur Okun developed a rule of thumb about the way in which unemployment reacts to GDP development.

The rule of thumb has it that if the unemployment fee is to stay fixed, the speed of actual output (GDP) development should equal the speed of development within the labour drive plus the expansion fee in labour productiveness.

Do not forget that labour productiveness development reduces the necessity for labour for a given actual GDP development fee whereas labour drive development provides employees that must be accommodated for by the actual GDP development (for a given productiveness development fee).

If we assume that productiveness development is round 1.5 per cent (a long-term development worth) and the labour drive grew at 2.0 per cent, then 1.7 per cent for the following two years after 2022-23, then GDP development must be 3.5 per cent for the present fiscal 12 months, then 3.2 per cent for the years 2023-24 and 2024-25.

A cursory take a look at the Desk above, reveals the next:

1. 2023-24 – GDP might be at the least 1.4 factors beneath the required fee to maintain the unemployment fee fixed.

2. 2024-25 – GDP might be at the least 1.1 factors beneath the required fee.

3. So the cumulative rise within the unemployment fee below these assumptions can be 2.5 per cent not 0.7 per cent.

The one approach that the unemployment fee will rise by 0.7 factors over the following three years is that if productiveness development is round zero if not detrimental.

My finest guess (based mostly on a simulation) is that unemployment will rise from 507 thousand as at March 2023 to round 685 thousand by June 2025 below present traits (tighter financial coverage and monetary austerity).

That may ship a 4.5 per cent unemployment fee and can imply an additional 178 thousand employees might be intentionally rendered jobless by the federal government’s personal forecasts.

That in itself is an appalling state of affairs for a authorities to engineer particularly when recording a fiscal surplus.

On this weblog put up – The so-called Inclusion Committee that recommends protecting the unemployed impoverished (April 19, 2023) – I up to date my estimates of how far beneath the poverty line the unemployment profit recipients are.

I confirmed {that a} single unemployed particular person on unemployment advantages was $181.25 per fortnight beneath the present poverty line.

A 26 per cent improve on the present profit degree can be required to push them as much as that line.

In final evening’s fiscal assertion, the Authorities, reluctantly (it has been below excessive stress to raise the speed), raised the speed by simply $40 per fortnight.

So whereas intentionally planning to extend the jobless numbers by round 180 thousand, the coverage of this authorities is to go away the unemployed round $141 per fortnight beneath the poverty line.

It’s usually stated that we must always choose a society by the way it treats its most deprived slightly than how wealthy folks turn out to be.

On that benchmark, the Australian authorities is failing.

The prime minister tried to whitewash this by claiming that final evening’s assertion was:

… a finances that didn’t go away folks behind.

That could be a categorical lie.

Huge fiscal contraction persevering with

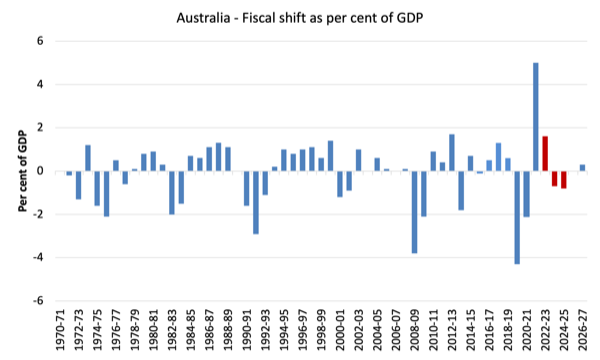

The fiscal shift from one 12 months to a different is the change within the fiscal stability as a share of GDP adjustments.

It supplies an concept of how expansionary or contractionary the present fiscal place relative to the earlier monetary 12 months.

It’s the results of two elements – the fiscal stability itself (in $As) and the worth of nominal GDP (in $As).

The next graph reveals the latest historical past (from 1970-71) of fiscal shifts as much as the top of the projection interval (2026-27).

I’ve colored the present fiscal 12 months (2022-23) inexperienced (it will likely be pretty near the precise revealed subsequent month) and the remaining purple columns are the ahead estimates for subsequent 12 months (2023-24) and people past.

A optimistic worth signifies a transfer to austerity (even when the fiscal place remains to be in deficit) and vice versa.

As you may see the shift to austerity in 2021-22 was giant (a 5 per cent of GDP shift) because the Authorities deserted the pandemic assist.

Within the first full 12 months of the present Authorities (elected Might 2022), the contraction continues, with the Authorities taking an extra 1.6 per cent of GDP out of the financial system and recording a 0.2 per cent of GDP fiscal surplus general.

Concurrently the RBA has hiked rates of interest 11 instances since Might 2022, this diploma of fiscal contraction is the rationale that GDP development is now projected to be at ranges the place the unemployment fee rises considerably.

The Authorities claims it has offered “a $14.6 billion cost-of-living aid package deal” targetted at low earnings employees and their households, the fact is {that a} fiscal contraction of this dimension will undermine the welfare of these households, lots of who will see breadwinners lose their jobs on account of the intentionally contrived slowdown in development.

And that isn’t to say the dearth of spending on methods to cope with local weather change and the housing disaster on this nation.

The place is the expansion coming from?

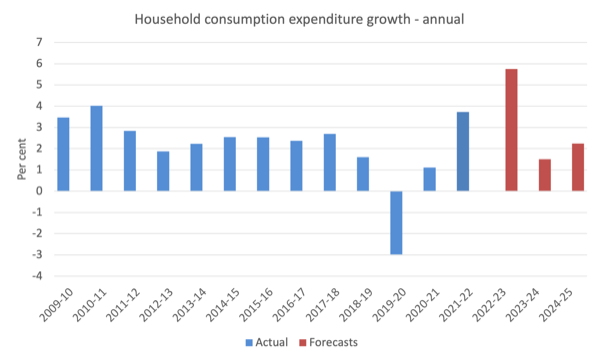

The 2023-24 fiscal assertion forecasts that actual family consumption expenditure will develop by 1.5 per cent in 2023-24 and 1.5 per cent in 2024-25.

The next graph reveals the annual Family consumption expenditure development from 2009-10 to 2024-25, with the purple bars capturing the Authorities’s projections.

You may see that after the consumption increase within the present fiscal 12 months as households modify again because the pandemic eases (a bit), is adopted by slightly slower development, which is according to the considerably decreased GDP development forecasts.

I think the ahead estimates of family consumption expenditure might be excessively optimistic.

Why?

As a result of the projected wages development is overly optimistic given present traits and the delayed affect of the RBA rate of interest hikes and the fiscal contraction underway.

Wages development has been at report low ranges even with the comparatively low unemployment charges.

With the unemployment fee forecast to rise considerably it’s arduous to see wages development breaking out of that development in any substantial approach.

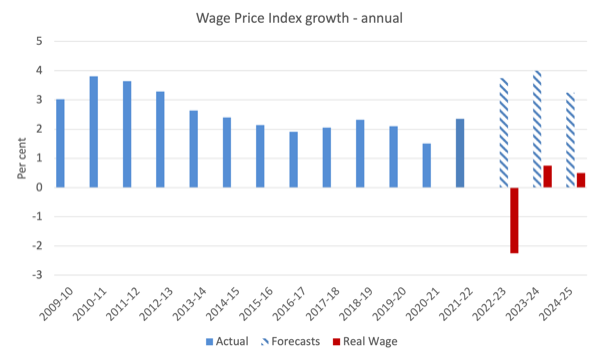

There might be some wages development however nothing like that projected within the fiscal assertion (see the following graph).

Even with these optimistic nominal wage development projections, actual wages will fall considerably within the present fiscal 12 months and solely barely report development within the subsequent two years.

I think that nominal wages won’t develop as a lot as forecast, which implies that the actual wage beneficial properties within the subsequent two years, already forecast to be miniscule, will in all probability disappear.

That leaves additional credit score development to drive development in consumption expenditure and with family debt at report ranges and rates of interest a lot increased than a 12 months in the past, I can’t see that taking place.

Why the federal government technique is unsustainable

We all know that the monetary stability between spending and earnings for the non-public home sector (S – I) equals the sum of the federal government monetary stability (G – T) plus the present account stability (CAB).

The sectoral balances equation is:

(1) (S – I) = (G – T) + CAB

which is interpreted as that means that authorities sector deficits (G – T > 0) and present account surpluses (CAD > 0) generate nationwide earnings and internet monetary property for the non-public home sector to internet save general (S – I > 0).

Conversely, authorities surpluses (G – T < 0) and present account deficits (CAD < 0) scale back nationwide earnings and undermine the capability of the non-public home sector to build up monetary property.

Expression (1) may also be written as:

(2) [(S – I) – CAB] = (G – T)

the place the time period on the left-hand facet [(S – I) – CAB] is the non-government sector monetary stability and is of equal and reverse signal to the federal government monetary stability.

That is the acquainted Fashionable Financial Principle (MMT) assertion {that a} authorities sector deficit (surplus) is equal dollar-for-dollar to the non-government sector surplus (deficit).

The sectoral balances equation says that whole non-public financial savings (S) minus non-public funding (I) has to equal the general public deficit (spending, G minus taxes, T) plus internet exports (exports (X) minus imports (M)) plus internet earnings transfers.

All these relationships (equations) maintain as a matter of accounting.

The federal government is estimating that the detrimental world elements will push Australia’s phrases of commerce from the 11.9 per cent improve recorded in 2021-22 to 1.5 per cent development in 2022-23.

Then the forecast is for a large contraction within the phrases of commerce of 13.25 per cent in 2023-24 and an extra fall of 8.75 per cent in 2024-25.

In different phrases, the commodity value increase which has pushed the exterior stability into surplus lately is forecast to finish and Australia will return to its traditional place of a exterior deficit of round 3.5 to 4 per cent of GDP – a state that has been dominant because the Nineteen Seventies.

We must always observe that the small fiscal surplus estimated for this fiscal 12 months is basically the results of huge tax receipts coming to the federal government on account of the commodities increase

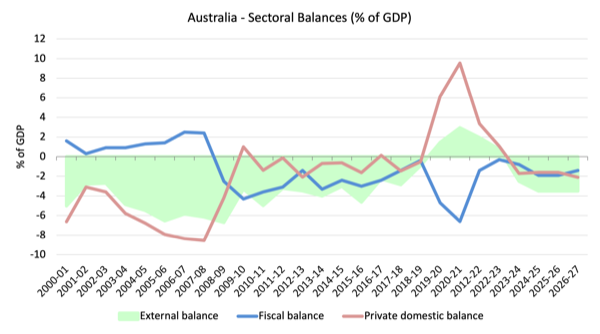

The next graph reveals the sectoral stability aggregates in Australia for the fiscal years 2000-01 to 2026-27, with the ahead years utilizing the Treasury projections printed in ‘Finances Paper No.1’.

The projections start in 2022-23 (though the present 12 months’s outcomes are in all probability going to be as forecast).

I’ve assumed that the exterior place in 2025-26 and past would be the identical because the Authorities’s estimate for 2024-25.

All of the aggregates are expressed when it comes to the stability as a p.c of GDP.

I’ve modelled the fiscal deficit as a detrimental quantity although it quantities to a optimistic injection to the financial system. You additionally get to see the mirror picture relationship between it and the non-public stability extra clearly this fashion.

So it turns into clear, that with the present account deficit (inexperienced space) projected to return to a deficit of two.5 per cent of GDP in 2023-24 (on account of a pointy reversal within the phrases of commerce) after which 3.5 per cent within the subsequent years, the non-public home stability (stable purple line) will head rapidly into increased deficits because the projected authorities stability (blue line) strikes to surplus (briefly) after which a small deficit after that.

You may see that the pandemic assist from Authorities clearly allowed the non-public home sector to rebuild its saving buffers and scale back the precarity of its stability sheet (given the huge family debt).

Within the ancient times, previous to the GFC, the credit score binge within the non-public home sector was the one purpose the federal government was in a position to report fiscal surpluses and nonetheless get pleasure from actual GDP development.

However the family sector, particularly, amassed report ranges of (unsustainable) debt (that family saving ratio went detrimental on this interval although traditionally it has been someplace between 10 and 15 per cent of disposable earnings).

The fiscal stimulus in 2008-09 noticed the fiscal stability return to the place it ought to be – in deficit. This not solely supported development but additionally allowed the non-public home sector to start out the method of rebalancing its precarious debt place.

That course of was interrupted by the renewal of the fiscal surplus obsession in 2012-13.

You may see the purple line strikes into surplus or near it and the non-public home deficit will increase on account of the liquidity squeeze.

The robust fiscal assist in the course of the pandemic overwhelmed all of the nonsensical deficit scaremongering and allowed the non-public home sector to extend its general saving (and pay down debt) which was an excellent factor.

However because the earlier authorities withdrew its stimulus and the present authorities continued to pursue a contractionary fiscal place (see above), the non-public home sector has just one possibility given the traits within the exterior sector if it desires to keep up consumption expenditure – resume the method of accumulating extra debt.

With a worldwide recession threatening and rates of interest rising sharply, the technique outlined in yesterday’s fiscal assertion is as soon as once more inserting the financial system on an unsustainable path counting on family debt accumulation, which is a finite course of.

Conclusion

There are a lot of different elements to the present fiscal stance which I’ll analyse within the coming weeks.

Typically, I’m unimpressed.

That’s sufficient for at present!

(c) Copyright 2023 William Mitchell. All Rights Reserved.